Review 4/10/23 - New Narrative: Private Credit Tightening

Review 4/10/23 - New Narrative: Private Credit Tightening

I Drink your MilkShake

If you are a new reader, there are helpful links at the bottom of this post.

Table of Contents

Dollar Milkshake

FOMC Minutes

Why we didn’t discuss CPI

Private Credit Tightening

Crypto Macro

Price Action

Conclusion

Internal References

1. Dollar Milkshake

I’ve been referencing what’s known as the Dollar Milkshake Theory quite a bit here over the last year. But my references to it have never been overt. We’re going to discuss it now, what it is, and its impact on countries worldwide now that it’s playing out.

If you have time and want a long explanation of the Dollar Milkshake Theory, you can hear it from the man who came up with the term back in 2018.

Obviously, this video is 5 years old. A lot has changed in that time, and interest rates have risen quite higher than they were back then and things have gotten significantly worse in liquidity terms.

If you don’t have time for the video, here is the basis of the Dollar MilkShake Theory. Since 2008, global central banks have injected over $30 trillion worth of reserves into the markets. This isn’t just US Dollars, this is Euro’s, Canadian Dollars, Australian Dollars, Japanese Yen, etc. Brent uses a syringe to depict this injection and then states that we have replaced our syringe with a straw.

QE and the injection of liquidity are not what matters. What matters is who captures all of that liquidity. The entity to capture that liquidity is whichever central bank is able to suck up this liquidity and capture it. Whichever central bank can raise interest rates the highest, and hold them there for the longest period of time will capture this liquidity.

And by capturing this liquidity I mean the exact thing we have been talking about on this substack. That is pulling liquidity into their own treasury bond markets. Whichever central bank manages to do this, will manage to increase the value of their own currency the most. This is the strong dollar trade that we saw happening last year. Entities had to convert their own currencies/assets into dollars to then buy treasuries to capture the risk-free return.

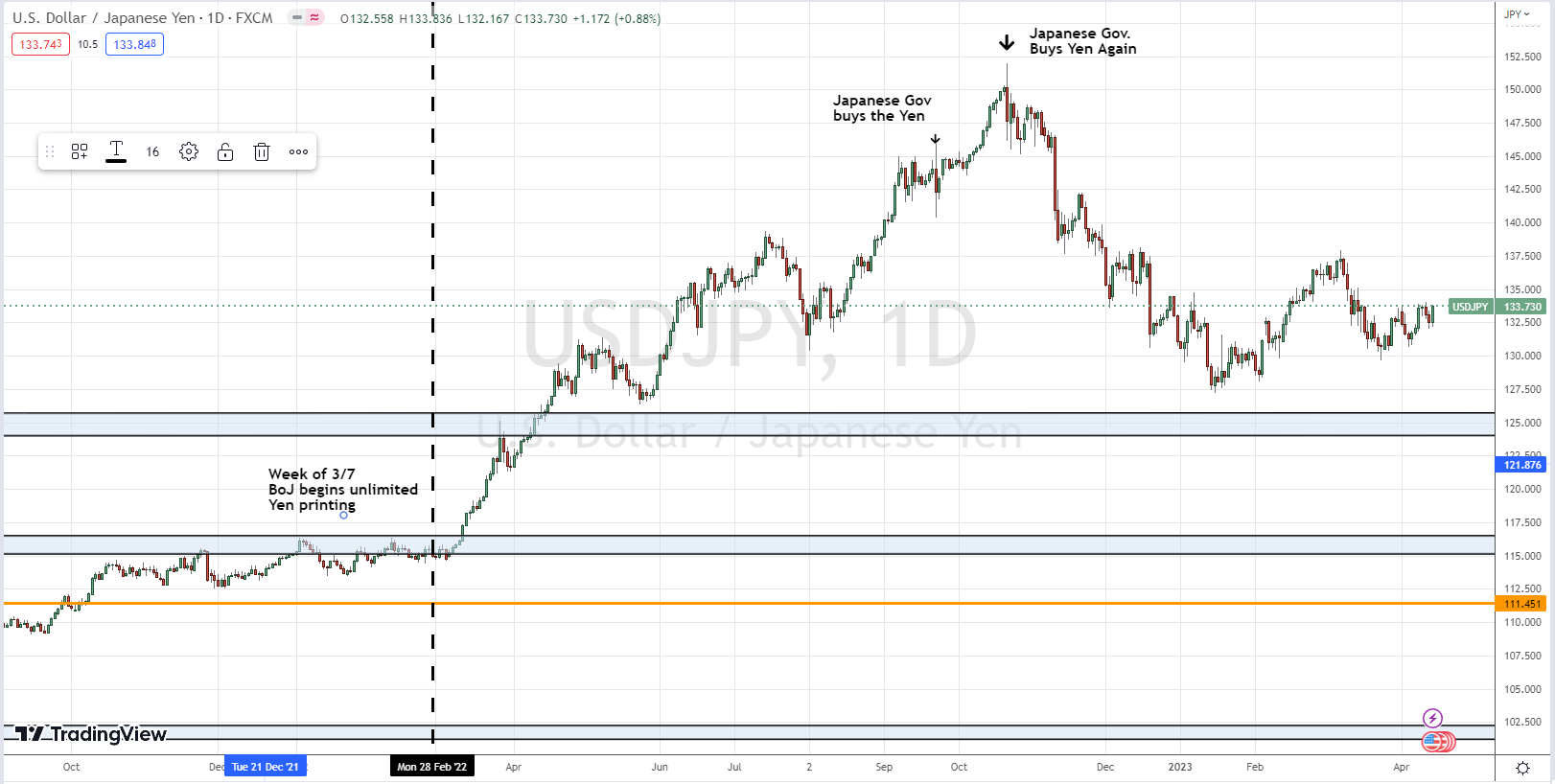

The fact that we are the ones capturing this liquidity is especially harmful to other countries. We saw Japan forced to sell their own treasuries just to support their currency because the dollar was getting too strong against it. This is an issue for many countries. They either have a significant amount of dollar-denominated debt that must be repaid in dollars, or they are dependent on dollar-denominated imports and need to acquire dollars in order to buy things like oil or natural gas.

It’d be one thing if, for instance, the Swiss were the ones to capture this liquidity, it would be far less harmful to the rest of the world because the Franc just isn’t needed by nearly as many countries to service debt or purchase their imports.

Sri Lanka collapsed because it could no longer buy imports as it ran out of dollar reserves.

The same thing is about to occur in Bolivia now. It likely will turn into Venezuela 2.0 due to the socialist government mismanaging their natural gas industry which they nationalized (read: stole) from the private companies that developed that industry in Bolivia. Bolivia was a net exporter of natural gas, but instead of investing in maintaining the industry, they used the income to pay for social services. Now their reserves are running out and the banks have run out of dollars. This is a problem because their local currency is pegged to the dollar similar to Saudi Arabia. You can’t maintain a peg to the dollar without significant dollar reserves. This wasn’t a problem when they were net exporters of hydrocarbons. But when they run out of natural gas to export because they didn’t invest in the industry, suddenly they can’t maintain the peg. Bolivia absolutely will be Venezuela 2.0 in short order.

But despite this being a real crisis for many in countries like Bolivia, Sri Lanka, Lebanon, Peru, Turkey, Argentina, etc. The Dollar Milkshake theory isn’t about these smaller economies.

It’s really about the large Western economies that invoice significant amounts of their imports/exports in the dollar.

We’ve been playing a game of musical chairs.

So long as the music is playing, every central bank is injecting liquidity into the markets. But when the music stops, there will be a loser. In crypto, you never want to be the last person trying to exit a liquidity pool. Similarly, in central banks, you never want to be the last one to hike rates, and you also don’t want to be the only one still easing while your trading partners have hiked.

This was the turmoil we saw in Japan’s Yen markets last fall. Kuroda, for all of his brilliance, had next to no understanding of what he was giving away by running the infinite Yen printer for the entirety of his term. Ueda is at least educated in New Keynesianism. He might have some understanding of what Japan is losing in its futile fight against low inflation. He still won’t change policy soon, but I expect that within 1-2 years he’ll be trying to bring the Bank of Japan in line with the West.

I suspect that by the time the BoJ is ready to come around that the West will have brought rates back down and paused QT. The ECB, BoE, and BoJ can’t keep up. That’s the plain truth of it. Beyond the stresses of the treasury market that the US government and Federal Reserve will have to deal with once the debt ceiling is lifted, one of their primary concerns has to be the soundness of their allies’ currencies against the dollar.

There is a reason Western central bankers meet for conferences often. There is a reason they speak to each other ahead of time in private regarding decisions with interest rates. They are trying to avoid this scenario where liquidity leaves one geography to enter another.

It’s why certain central bank decisions are entirely predictable. The Bank of England follows the Federal Reserve, they don’t have a choice. The Swiss National Bank follows the European Central Bank, they’ve depegged the Swiss Franc from the Euro, but they still want to maintain equal FX flows to the EU. The ECB feigns some sense of autonomy they get to do this because the Euro had some invoicing dominance prior to the Ukraine invasion, but since then Russia and China who predominantly traded in Euros have essentially stopped and switched to Yuan and Rubles. The ECB has to figure out where its bread is buttered and catch up to the Federal Reserve, otherwise, the Euro will fall below parity with the dollar again and the federal reserve gets to do its best Daniel Day-Lewis impression.

I. DRINK. YOUR. MILKSHAKE.

If they can’t keep up, or the Federal Reserve decides not to pivot but instead leaves them behind then we will watch liquidity flow to the highest western yield. In much the same function as it does in crypto markets. At every level we are degenerates chasing yield.

Having one-way liquidity flows out of currencies and into the dollar would be catastrophic for each country that does this.

This isn’t what will happen in my opinion, but it’s one of the many potential outcomes that are on the line if the Federal Reserve does not pause rate hikes soon and reverse course. The Fed and central bankers are well aware of this. For the first time, we could even say that Japan is aware of this too.

Either the music stops, and we find out who doesn’t have a seat, or we let the music play forever and hope we don’t get tired… or hungry.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.