Forecast - 5/1/23 - Revisit the Debt Ceiling

Forecast - 5/1/23 - Revisit the Debt Ceiling

Central Banks let off the Accelerator

If you are a new reader, there are helpful links at the bottom of this post.

All times in this update are in US Central time (UTC-6 clock).

Song of the Week - Chet Faker - I’m Into You

Table of Contents

US Debt Ceiling

First Republic Bank

Economic Calendar

Australian Interest Rates

US Interest Rates

European Interest Rates

Crypto Macro

Price Action

SUI Launch

Conclusion

Internal References

1. US Debt Ceiling

My standpoint on the US debt ceiling has not changed since February, but we are going to revisit it now in light of a recent statement made by Janet Yellen, current US Treasury Secretary.

After reviewing recent federal tax receipts, our best estimate is that we will be unable to continue to satisfy all of the government's obligations by early June, and potentially as early as June 1, if Congress does not raise or suspend the debt limit before that time. This estimate is based on currently available data, as federal receipts and outlays are inherently variable, and the actual date that Treasury exhausts extraordinary measures could be a number of weeks later than these estimates.

Last week the US House proposed a $1.5 trillion debt ceiling increase and spending bill. This bill originated from the Republican congressmen, and will not pass the Democrat-controlled Senate, nor will it be signed by Democratic President Joe Biden. While we are at the debt ceiling the treasury has to manage the fund available to the government to finance its operations without issuing new debt in the form of treasury bonds.

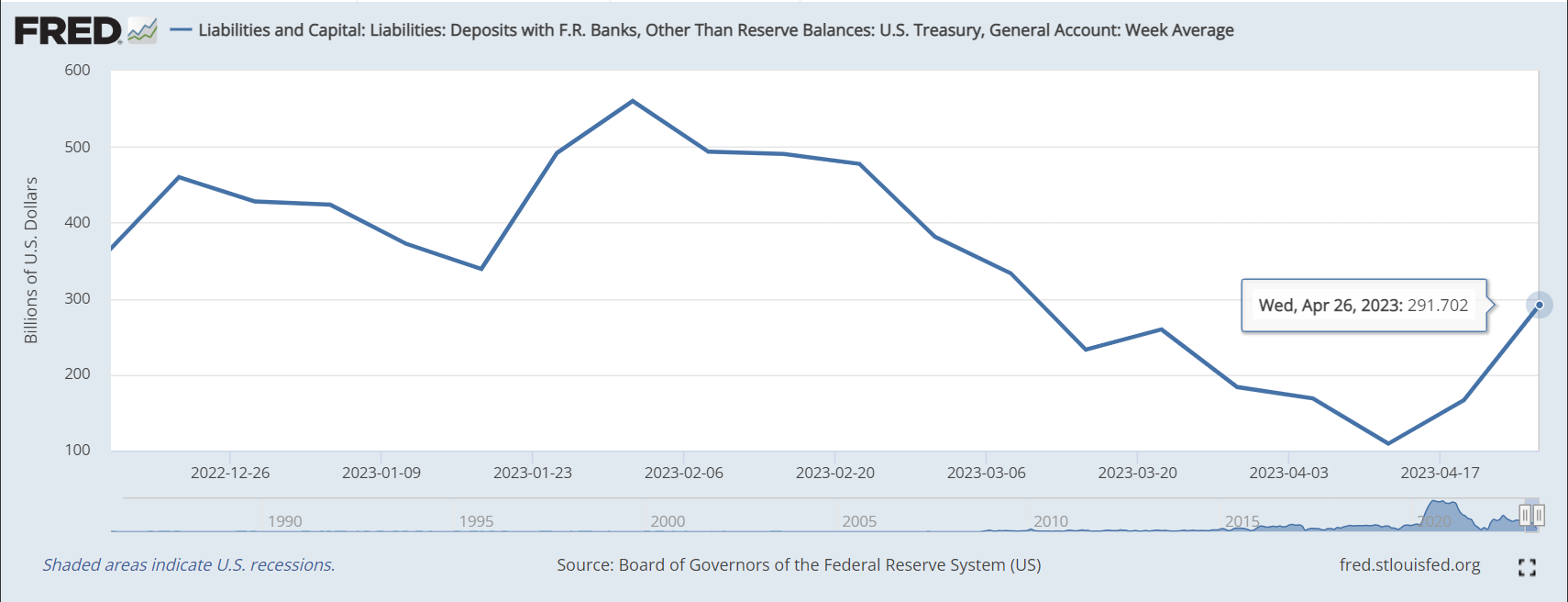

Any additional tax revenue received beyond that which has already been budgeted for expenses would go into the TGA, and we can see that it has increased since the April 12th lows, but I would not hold my breath at all in expectation of additional funding for the TGA. The burn rate for the treasury has so far been roughly $180-$190 billion a month, and having just short of $300 billion in the account at the end of the month does imply they will run out in the month of June. However, it’s possible that more tax revenue may still be coming over the following week (May 3rd) or so. However, this small amount of string is highly unlikely to cover expenses for much farther than the month of July. At this point, more government services will have to shut down unless the legislature can put together a spending bill that Democrats actually like and want to sign.

So far the Republican House has held fairly steady but as I stated in February:

What sorts of pressure might the Treasury put the US legislative branch under as this reality becomes more apparent to the Treasury? This was fairly predictable, but none of the half-decent quants work for the government so the government is mostly blind and reactive to situations like this.

I’m expecting the token resistance of the Republican Party to be over-run once discussions about the government shutdown expand when certain government activities that were presumed to be funded by tax revenue suddenly are no longer funded. But, that does give us 1-2 months where no one really has any idea just how bad things are going to get. This is the eye of the storm indeed.

Consider this letter from Janet Yellen and members of the House and Senate to be the beginning of that pressure being applied to the legislator today. I also find it to be not a coincidence that the copy of the letter that is circulating on Twitter is the one sent to the Republican Speaker of the House. It already feels like McCarthy is starting to fold and may simply be airing this out so as to justify it when he starts pushing for compromise. But we’ll see, I shouldn’t malign the man so soon.

First Republic Bank

Otherwise, the only other major event I have not discussed is the collapse of FRC (First Republic Bank). They collapsed for a fairly similar reason as Silicon Valley Bank. They issued mortgages below the market rate with the assumption that because their clients were very credit-worthy that there was little to no default risk. Unfortunately, interest rates moved significantly against them and when they had to sell their mortgage-backed securities they were doing so at a significant loss and had to mark their assets to market and recognize this loss for the first time.

When this occurs they have to sell off assets. This is where problems arise. You never lose any money until you sell, so the solution, when upside down on treasuries is just to not sell and pretend they don’t exist. But if you’re forced to sell, suddenly you have to realize that loss. Be mindful of the following sentence.

The financial institutions that have “collapsed” are just the ones that were forced to sell, everyone is holding toxic treasury debt so long as rates keep rising.

A financial entity that has not accounted for losing a significant chunk of money being forced to do so in a moment when they are already in distress is likely done for.

As I stated back in March, almost every financial entity is holding assets like this that are significantly underwater. This applies to mortgage-backed securities and treasuries. There is a free article on BowTiedBull diving deeper into FRC’s balance sheet, but the important thing for you to understand is that almost all financial institutions are holding some level of toxic debt assets on their balance sheets that they can no longer sell and can only hold until maturity. The better-run financial entities have rebalanced their assets in time or bundled and sold a portion of their mortgages and treasuries prior to 2022 so that their exposure to longer-dated maturities was low enough to hold until maturity. But many did not.

This is the inevitable outcome involved with raising rates, and today the US government and even Yellen herself are now dealing with the fallout of raising interest rates. This will always be ironic because in 2017 when the overnight lending rate was still 0.75% Yellen stated that she didn’t see a financial crisis occurring “in our lifetimes.”

And yet an implied financial crisis always exists if lending rates are low and must be raised. Yellen oversaw a looming and necessary financial crisis, yet was publicly blind to it.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.