Review 12/13/21 - Free Giveaway

Oracle Says... we wait

Thank you for joining me for the 2nd week of content review.

I have added a Definitions page which will include all of the terms and abbreviations that I use from now on and will be referred to on every post.

We will be reviewing my predictions from The Post I made at the beginning of this week on Sunday 12/12/22.

My first giveaway will also be on this post.

Table of Contents

Giveaway

Mindfulness of our Goals

US FOMC Interest Rate Decision

High Impact Global Events

Bank of Canada Speech

Swiss National Bank Interest Rate Decision

Bank of England Interest Rate Decision

European Central Bank Interest Rate Decision

Bank of Japan Interest Rate Decision

US Bond auctions

Results

My thoughts on the future of the Treasury Markets

Conclusion

1. Giveaway

A few posts ago I stated that I would be giving away subs in a series of competitions on my free posts. A whole year of free content. Whenever I hit subscriber goals, I will be giving away subscriptions. Forever. So long as this substack grows, these competitions will always keep happening. If the $10 a month might be out of your budget, then share this substack with whoever you can, especially if you are reading something good, or relevant to someone you know. If they subscribe, it pushes you closer to another competition for a free sub. And $10 can absolutely change budgeting decisions, so no shade on you at all. I don’t pay for my netflix subscription, I probably never will. Forever a mooch.

To enter, it’s as simple as leaving a comment on this post responding to a prompt. I will choose 2 commenters to gift a subscription to my substack for the next year.

The prompt is: Tell me about who you want to be, and where you see yourself in 10 years. Alternate prompt, tell me about goals you have achieved for yourself that you once thought were impossible.

I will choose 2 winners Next Friday on Christmas Eve. The winners will be determined by which ones I like the most. Subjective I know.

2.Mindfulness of our Goals

Following along with our prompt, here’s a quick music video by Rich Brian (fka Rich Chigga).

This is the first song he ever wrote, when he was 15 years old living in Indonesia. He shot this music video when he was 17, and a year later, he moved to California, and he did become famous over the last 4 years, and he has a song titled “Bali,” that he filmed in Bali. A lot can change in 6 years.

One of the most gratifying things we can do as people is write goals down and work towards them. Every year, in March (after a personal holiday I invented), I write down my goals for the year, and I strive to achieve them by October. I give myself 8 months in the middle of the year to make things happen. And the biggest surprise for me is reviewing my list every October and seeing just how much I did accomplish (I always underestimate myself), and just how far I have come. I also made a list of goals 6 years ago when I moved to the city I currently live in. It was a 5 year list, and its been a very moving experience for me to look back at what I wrote down in 2016 and what seemed so impossible to me and was all achieved by the end of 2020. Of course, a new list of goals was written, and as I stare at it now, many of them seem impossible as well. Yet, I know I’m going to crush them, even though CovID nonsense cut one of them out at the knees.

I’m not saying that you won’t have hardship. Or that your dreams for your life will all come easy just because you write them down. But I am instead saying that focusing it into written words, real tasks, and milestones with real work attached to them has power. And then, once you start achieving a few of them, you will end up building self-esteem and feeling more capable and willing to take on more complex problems. This is a psychological concept called The Winner Effect. The more wins under your belt, the more serotonin your brain pumps out, and the less cortisol your adrenal glands create. You will literally start feeling better, looking better, and reacting better under stress. The opposite effect happens when you take a lot of losses in a row, especially big losses. There is a great book on this topic that I value a lot, called The Hour Between Dog and Wolf, it follows a group of wall street traders around during the housing bubble collapse of 2007-08 and explains the bio-mechanical processes ruling their behavior. It contains great insight into the brain-gut connection through the Vagus nerve as well. I highly recommend reading it or listening to the audiobook if you intend to trade, or manage financial assets.

3. US FOMC Interest Rate Decision

I have covered this decision and its ramifications in a separate post.

4. High Impact Global Events

Bank of Canada Speech

A decent summary of the speech can be found here. I found this speech to be too dovish to really put a bottom on the Canadian currency. They have left the door open for a rate hike in January but I don’t think we will see the short term top at 1.3 on USDCAD like I had envisioned. While we did wick into the supply zone I mentioned earlier, it is quite likely that we will push through that supply zone (light purple). For a swing short entry, I would wait and watch until January, and I would now expect for the high to come closer to 1.31 (around 1.30840).

Swiss National Bank Interest Rate Decision

The swiss provided no major changes or surprises, as expected.

Bank of England Interest Rate Decision

This was our big watch and the Bank of England did not disappoint. As expected by me (and lol, not by the Guardian), the Bank of England began their upcoming rate hikes with a push from 0.1% to 0.25% for the overnight rate. I’m not sure what the reporters at the guardian were looking at to be surprised by this move, but I’m guessing they just paid an intern to write an article from a 400 square foot apartment with 7 foot ceilings and a half kitchenette. No real thinking can be done in a space like that. If you live in such a space; go outside, use the night sky, or the infinite canvas of blue at mid-day as your muse.

As the Bank of England attempts to undo the damage caused by Brexit, we will see a significant swing in their currency over the next few months. GBPUSD fell all the way to 1.3162, and if you check my forecast, that is 2 pips away from the top of my target range for 1.314-1.316, and is likely to be the near term low.

I would expect for the following week for brief entries into this zone again around 1.3196 and to provide another long entry. From the Guardians article you can still see how far off the “financial journalist” sphere is from the actual truth, they expect no further rate hikes. Yet, as discussed by me this past Sunday, the head of the BoE has signaled for multiple rate hikes coming soon and they are already behind on their own schedule. I would expect several rate hikes over the coming year, and a great opportunity for a swing up to the 1.59-1.65 range within the next 9-14 months. On leverage and with multiple entries, this can be a great safe trade to stagger positions into. As a note, to maintain adequate risk management, when staggering entries, make sure to stagger stop losses as well to maintain profits if the markets move against your thesis. No matter how good the trade looks, risk should be managed so that you can trade another day if you are wrong.

European Central Bank Interest Rate Decision

No changes to the negative rates in Europe. They have commented to slow down their purchase of bonds, but to increase their purchases of assets. Shuffling deck chairs on the titanic. Inflation in the Eurozone will continue, no meaningful changes were made. This is par for the course for the ECB.

Bank of Japan Interest Rate Decision

No changes were made to interest rates, but the BoJ decided to announce tapering of their corporate bond purchases while still maintaining negative rates. This is not a significant impact announcement for the Yen.

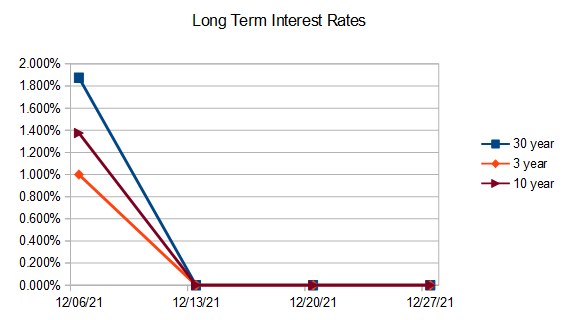

5. US Bond Auctions

You can generate and download the reports from the treasury HERE (note: many “financial guides” charge $100 a month for this data that the gov. gives you for free at this link), the “competitive PDFs” are what you want. Now we’ve got some more data on the Bid to Cover Ratio’s as more auction data has come in.

Results

We still mostly just have data for the first week except for the 4 week note. As we can see, there is much less demand for longer term debt than there is for short term debt, which makes sense, as this is the general trend we will always see, since longer term debt comes with more risk and is a less liquid market. Of course, we can’t yet see trends emerging (and I’m not going to add retroactive data, these charts will grow and move with us). I have since split interest rates into 2 charts, one for short term, and one for long term to make the data more readable.

As we now have 2 weeks of data for interest rates, but we are still mostly lagging in data for the Bid to Cover ratio due to the slowness of the Treasury to upload that data. From just a cursory glance at these rates, I would presume that the 6 month, and 3 month auctions also saw a drop in their bid to cover ratio compared to their auctions last week. Will confirm this next week.

The long term bond auctions occur monthly, so there is no change to be noted here, I have simply added the chart here so that the rates can be viewed separately from the short term rates.

My thoughts on the future of the treasury markets

Due to the Fed’s recent decision to increase the speed of tapering starting on Jan 15th, I expect that we will see a significant drop in the Bid to Cover Ratio in the auctions in the latter half of January to concur with a mild spike in interest rates. I expect further spikes to follow in February and March as random auctions will find low volumes of bidders for treasury notes.

How the Fed reacts to that will determine in which manner the US economy breaks. If they ignore it, and let Government lending rates rise, we will see significant chaos at the federal level and we will also see asset prices continue to fall as people move further into the dollar. That is what they should do. It is the most ethical thing for them to do. And there is a small outside chance that they actually do it, which is why we are watching the markets. If on the other hand, the Fed is pressured to intervene, or decides to intervene, they will push the economy further into stagflation, but the Federal government will not struggle to fund itself.

If the government pushes the Federal Reserve to reverse the taper and save the treasury bond markets with increased bond buying to hold interest rates down at this point in the cycle, we would do something that has never been done before in the chart above except for briefly in the mid 1970’s. We would enter a recession (in gray), and the CPI would keep rising. This is known as stagflation. Even in the 70s and 80s, you can see CPI mostly taking steps backwards during recessions. This would be a huge mistake for the federal government to make, but I don’t put it beyond them to do this, and it is the worst case scenario I am watching for. I say that because it is imperative for you reading to understand that and to not front-run this trade, or you will end up feeling pain as covered in the intro to last weeks review, which is something we are trying to avoid. The thesis right now is for prices to be flat or going down for the next few months in US Dollars. So if you are buying assets right now, it should be in a DCA strategy of just regular recurring purchases that fit within your budget. When the treasury market breaks and we see how the Fed reacts, that will be our signal for big splash purchases. For now, as stated last week, holding cash equivalents, and DCAing crypto is the strategy.

6. Conclusion

The British Pound, and several emerging markets have pushed for interest rate increases and are diverging from other western nations that have not yet moved to stop easing.

The US has announced it will double the rate of tapering starting on January 15th 2022, which will conclude the taper in March 2022. For now the narrative is holding and we can expect asset prices to continue flat or down. Meaning that the effective strategy is to DCA into risk assets with regular purchases, and to hold/accumulate dry powder for a larger purchase at a later date depending on how the Federal Reserve reacts as it loses bid volume from the treasury markets. I’m not here to sell you an unfounded dream. I have a belief about the math and what the central bank will do, and how the markets will react. There is a hypothesis, and a null hypothesis. I will never be so blind as to ignore my null hypothesis. But at the same time, something has to break.

Either the federal government has to massively cut spending to deal with the incredibly high interest rates that will result when the Fed lets go of the treasury bond markets. Or stagflation will result when the Fed reverses course and continues easing. One of two scenarios is mathematically guaranteed. The 1st scenario, is good for anyone with a job as their income will go further and be able to buy more things. The 2nd is good for anyone with assets, as people who are productive will have to spend more of their time to buy your assets, making your assets more valuable as units of exchange.

Our goal here is to see which one will occur, and to move appropriately before the rest of the market does it. But for now, we are in a holding pattern.

My biggest accomplishment will definitely be getting sober from prescription pills and weed, seems petty but addiction is a mfer...

Hard to say where I'll be in 10 years, not that I don't have goals or aspirations, I just want to be healthy, I'm getting married and I want to be happy with her, healthy and happy.. Hopefully my father is still alive, I lost my mother, 53yrs old, 5 years ago and my sister, 34 yrs old, 2 months ago, so he's the last I have.. As we are all here to gain knowledge and make money, money is simply a tool, and it cannot buy happiness unfortunately!

expecting nothing in return buddy!

I want to be someone who is physically fit, able to afford to eat (and maybe grow) things that are only good for me, confident in my abilities, knows what I want from life and relentlessly goes after it, and thoughtfully enjoys every day of life with people I love, doing things I love.

In 10 years, when I'm on the edge of 30, I want to see all of those above elements which I'm already working on be a given in my everyday life. I see myself with significant agency over my time in how I work, which likely will mean creating liveable streams of income outside of being a corporate employee. I see myself married to a man who shares similar desires, makes every day a little sweeter, pushes me in all the good ways, and loves living life. I see myself living in a mountain home likely in Colorado or Montana and waking up every morning thankful to see nothing but nature and hear nothing but birds and maybe a creek. I want to successfully graduate college/earn my compsci and neuro degrees, use them to find a job I like that supports my other goals, and then continue learning across all of those 10 years. I see myself financially free and not tied down by anything unpleasant. I see myself having maintained good friendships I formed now and when I was even younger.

In short, I see myself financially successful enough to afford a lifestyle that leaves me content, healthy, and able to devote time to meaningful relationships.