Review 1/10/22 - Empty Words

Wall Street vs. a Used Car Salesman

Welcome we will be reviewing macro events from this past week from The Post I made at the beginning of this week on 1/10/22.

I have added a Definitions page which will include all of the terms and abbreviations that I use from now on and will be referred to on every post.

Please do not respond to the email, if you wish to leave a comment come to the substack website, especially if you are sharing information that would be beneficial for everyone to read. I will not answer questions or respond with information by email because no one else gets the benefit of seeing my response. The “comment” button at the bottom of the email will take you straight to the substack site.

This post is too long to be viewed by email, please come to the site to see it in its entirety.

I would like to take this space to say thank you for those of you who were willing to jump platforms to follow me here, as well as those of you who have joined in that time from elsewhere. Our test drive is coming to an end and the weekly macro updates will be shifting to behind the paywall from here on out. There is one more free post that is coming soon and its a beginners guide to DeFi. In general, all of my beginner guides will be on the free side so that the first rung of the ladder is available to everyone. If you can self-teach and ingrain yourselves in the right circles and continue to network, you can make it from the free content alone. But of course, the paid content intends to contain much more value for turning a profit in DeFi, and identifying new projects to invest in.

This is the last reminder those of you who have already paid will be seeing to subscribe. The test drive is nearly over, and this new car smell will be yours for as long as I last on this platform.

Table of Contents

US CPI

Central Bank Speeches

US Federal Reserve

European Central Bank

Bank of Japan

US Bond Auctions

Crypto Macro Update

Conclusion

1. US CPI

As expected, the print we received for CPI was above the consensus forecast by the mainstream media. They were guessing we would get 5.4% for the month of December, instead, we got 7%, which was slightly above the print for the month of November (6.8%).

I very often say that right now, Wall Street and most of the major banks are getting the B-team in terms of analysts and talent. You can read this CNN article where journalists and the empty sacks of meat that run our government are confused about basic economics if you want. Or just this quote below.

Of course, it wasn’t just the Fed that inflation wrong. Very few forecasters on Wall Street anticipated inflation would be this high for this long.

People think the banks are up on crypto and are master puppeteers that have their fingers on the pulse and have planned out life for the next 5 generations for their cattle. They really haven’t, they’re mostly in charge because they were born into the right family or got into HYSPM. The ivy league isn’t what it used to be. Education as an industry has devalued itself, and the rot goes all the way up to the top. Most of these banks are only hiring from HYPSM, not because people from those schools have any insight of value, but instead because their WASPy clients are typically dumb money and can only really respond to status symbols. The working hours at these banks are horrid, and starting salaries are barely even above $100k (in NYC).

Any one with any aptitude, creativity, and critical thinking can figure out this puzzle, and those people are all in crypto. The banks, and especially government economic departments are hurting for talent, which they will never get.

Consider, there are people with pH.d’s in economics working for governments that don’t even understand that money is a good as well and is subject to the laws of supply and demand. This is part of a bigger problem in that college is utterly broken and only can measure how long someone can sit still, how gullible they are, and their tolerance for debt on an asset producing no return that you can’t even sell to someone else. You can graduate if you have the capacity to take on debt, nominally show up, and copy paste what you’re told. So the administration and financial class will continue to express confusion about CPI.

But here’s whats next. The pot is slowly boiling, and at some point (maybe even last month) we’ll reach a short term high in inflation. Maybe we return to ~5% Year over year each month, this will be phrased as a good thing in order to get the general public accustomed to and having positive feelings about this range of inflation (as measured by CPI anyways). They will make people feel used to it, so that some of the pressure can be lifted off of them. We’ve discussed the proposed schedule for tapering earlier.

The factual promises that were made, are as follows

Doubling the rate of taper in mid-january

Concluding the net purchase of assets with printed money by March instead of in June

Three rate hikes in 2022 so that the overnight rate is 0.9% by the end of 2022

Today is January 15th, and I’m sure that they will maintain the rate of doubling the taper for now. But when March 15th comes, I suspect that the Fed will announce that they want to slow the rate of taper, or hold consistent asset purchases, and I suspect that they will lean on this “decreased” inflation around 5%. This narrative will also fall apart however over the summer. Prices and supply of fertilizer for the current growing season took a terrible turn for the worst this past fall, and the impacts of that will not be manifesting for the average consumer until summer time. At which point I expect the further pinch of increased inflation, decreased productivity, and a continuing money printer to force the Fed to act. Powell has spoken a few times about the dire need to reign in government spending, but he, like all Fed Chairmen is ultimately beholden to the party in power. I have never seen a single administration actually cut spending except Carter. This one will be no different. They won’t cut spending. The bond markets will be bleeding again. Inflation will be soaring. They will prioritize government spending, and the money printer will kick back on. This is the easiest trade in the world, and Wall Street will miss it.

This is how wall street did last year. I would be embarrassed if I performed this badly against the dollar considering how last year went. To put this into context, only 1 of these hedge funds performed better than just buying a used car instead.

I wish people would stop telling me that wall street has crypto figured out. Thats the B-team.

2. Central Bank Speeches

US Federal Reserve

I’ve already touched on a bit of Powell’s speech above. It was boring as hell, the US congress and senate asked very few relevant questions, and often dropped the ball when they had a chance to press for anything of consequence. If Wall Street is the B-team, our elected representatives are the D-team. They did ask about Federal Reserve board members insider trading, but no one addressed the rampant insider trading done by members of congress and the senate. Figures. Powell essentially answered their questions about inflation for them to just wait for it to go down. There’s about a 6 month lag from market activities to market responses and they’re still printing right now. Conclusion is obvious. They will be waiting a long time for inflation to go down, longer than the bond markets can hold off.

European Central Bank

One of the few central banks that holds assets even more toxic than the US. Christine Lagarde is the current head of the ECB, and the ECB has been printing money for a long time, and is going through a similar issue as the US, except even worse. They also measure Inflation through a rigged CPI, and are struggling to keep it down. Lagarde made very similar statements for the Eurozone to “wait” for inflation to go down. It won’t, it’s going to get much worse. They are several years away from solving their energy supply issues. The geo-politics of Belarus, Ukraine, Russia, Lebanon and Turkey will further exacerbate their issues with energy delivery and Europe may find itself dependent on LNG (liquefied natural gas) deliveries by ship from the US to sustain their energy demand as Turkey and Lebanon descend further into hyperinflation and instability while the Eastern European states become more belligerent as the ex-soviet bloc consolidates power and uses their advantage to extract higher prices on energy exports to western Europe. At the same time they have shown no sign of slowing down their money printer any time soon.

Bond buying under its 1.85 trillion euros ($2.19 trillion) Pandemic Emergency Purchase Programme, or PEPP, which is due to end in March 2022, will be cut next quarter as the scheme winds down.

However, bond buys under the Asset Purchase Programme, or APP, will be ramped up to serve as a quantitative easing bridge through the end of the PEPP, having continued at a monthly pace of 20 billion euros in conjunction with the PEPP until now.

They’re going to end one bond buying program, and replace it with another. It’s deck chairs on the titanic. In section 2 of this post I covered how irrelevant and broken the money is within the EU, but I’ll repost it again to drive the point home.

This chart (3 month European Interbank interest rates) is weak and depicts a mostly irrelevant continent. The money is worth so little to the people that have it that they will pay you to take it away from them. There is no wealth to protect, at least not in the paper anyways.

Bank of Japan

This speech was mostly meaningless.

3. US Bond Auctions

You can generate and download the reports from the treasury HERE (note: many “financial guides” charge $100 a month for this data that the gov. gives you for free at this link), the “competitive PDFs” are what you want.

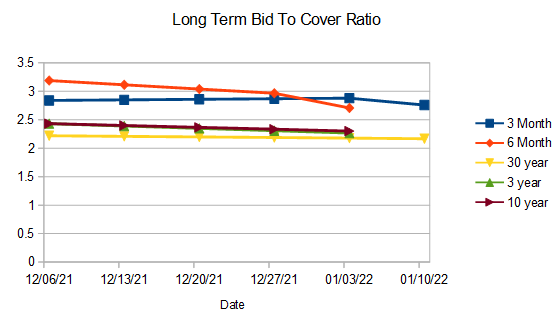

I have split the Bid to Cover Ratio charts into 2 because the 4 week is so volatile that it drowns out any movement in the longer term data. Across the board, the bid to cover ratio is falling, which is to be expected as the Federal Reserve will be buying back less and less treasury bonds from the entities that participate in these auctions. Without a guaranteed buyer, some entities that participate in the bond auctions will be looking to take their money elsewhere. ZeroHedge has a brief piece on the 10 year treasury bond auction. Of note from them; foreign buyers have been decreasing their purchase volume continually. This decrease in bids is also being matched by an increase in interest rates across the board. I suspect that for auctions occurring after today (1/15) that we will see a larger jump in interest rates, since today is the day when the Fed will double the rate at which it stops printing and buying back treasuries. So any participating in auctions next week, will be doing so with less printed money ready to buy back their treasuries.

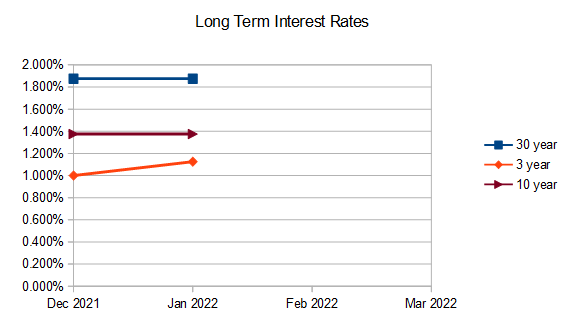

Below are the interest rates for those same auctions. This data is usually shared when the auction resolves so we don’t always have all of that data for the past week.

Of note, the long term auctions occur on a monthly basis, so their interest rates will be displayed on a monthly chart from here onwards. We can see a general trend is occurring since we began tracking in December of interest rates rising, especially for the 6 month note, who’s interest rate has nearly tripled in the past month. This is to be expected as the volume of bidders in these auctions continues to go down. When there is a real dislocation in these markets. We’ll know from watching these charts, and we’ll be ready to buy (crypto).

4. Crypto Macro Update

Lets touch on some of the crypto macro trends again. As previously stated, 2022 is going to be the year of interoperability. I outlined 4 protocols that stand to benefit the most from this trend in 2022. ATOM, DOT, ICX, and LINK. These 4 protocols are the architecture through which different blockchains can talk to each other and send assets back and forth to each other without having to go to a Centralized Exchange first. Truly, no one wants to go through Centralized Exchanges, and this architecture will come to be more and more in demand.

I will cover this more in my Intro to DeFi post, but if you are just getting started in crypto, you should be accumulating BTC and ETH. However, BTC is not smart contract capable, and transaction fees on ETH are too high for anyone with less than 6 figures of ETH to deploy in DeFi. Meaning that when you want to start interacting with smart chains, you’re going to have to do it somewhere else than ETH. There are many alternate L1’s; FTM, AVAX, NEAR, XTZ, ONE, SOL, STX ICX, and others that are smart contract capable and have DeFi dApps available. Gas fees on these chains are often pennies or fractions of pennies. And as more bridges are built to these which unlocks ETH’s liquidity on to these chains as well as the launch of interoperability solutions unlocking liquidity, we’ll be seeing a rotation of capital to these chains. The retail investor, looking to participate in DeFi that doesn’t have 7 figures of crypto is going to be joining these chains instead, and they are going to be attracting more devs, and more bridges as crypto seeks to find its level and most efficiently use the available capital.

This is a good year to be branching out, especially as you start interacting with DeFi. As these L1’s compete for limited developers talent, they are going to incentivize developers to come to their chains with incentive programs. Its a pattern like clockwork that incentive programs bring dApps, which bring users, which brings price appreciation.

These L1’s are going to be heating up in competition this year and this is one of those rare win-wins for everybody. If you take this year to learn how to engage in DeFi, there will be more cheap opportunities for income, and some of those incentives will be used to increase the yields in DeFi. And beyond that, these tokens should all appreciate, because transactions on their networks, burn the supply of the token and can cause some of these tokens to even have deflationary tokenomics. I would be on the lookout for more bridges, and more incentive programs this year. Taking a flyer on a new bridge, or an incentive program is often a good way to find an appreciating asset.

5. Conclusion

The banks are clueless.

Wall Street Hedge Funds as an investment couldn’t even outperform used cars in 2021.

The governments are clueless.

Inflation is here to stay.

Tapering will fail in a few months.

Treasury interest rates are already rising.

Begin familiarizing yourself with some of the alternative L1 smart contract protocols, and watch for them to appreciate as they spend more money to incubate developers and new dApps on their chain, as ETH is too expensive to use for new market participants. Prices across the board will still remain flat or down in most assets in this time period, so don’t rush and stick to a schedule of investment until we reach more short term turmoil in the treasury bond markets.

Our time comes soon, and lastly… I don’t ever want to hear about the B-Team again.

I've been thinking about your thesis on the fed (tapering will fail narrative) which is very intriguing. How much certainty do you see this happening? is there anyone that holds a differing POV?

Looking forward to the DeFi guide!