Review 5/9/2022 - $LUNA Post-Mortem

Inflation is Our Greatest Strength

Welcome we will be reviewing macro events from this past week from The Post I made at the beginning of this week on 4/26/22.

I have added a Definitions page which will include all of the terms and abbreviations that I use from now on and will be referred to on every post.

Substack has launched an iOS app for those of you using apple devices. I am an android peasant and can’t tell you if its good or not, but check it out if you have an iPhone or some other such trappings of royalty.

Please feel free to skip around or ignore certain sections if it does not apply to you. The Table of Contents is made to preserve your time in this manner. You can always simply read the conclusion if you are in a hurry.

Table of Contents

Coinbase and Mid-Term Risks

US Inflation

Crypto Macro

$LUNA Post-Mortem

Impacts to $ATOM

Broader Market Impacts

Bitcoin Macro Analysis

Conclusion

1. Coinbase and Mid-Term Risks

One of the main theses’ put forth in the beginners guide to crypto and the beginners guide to wallets is that we likely had a 2 year runway for people in the west to be figuring out how to take custody and sign transactions for crypto.

If I had to guess, the IRS and federal government will start tightening restrictions on centralized exchanges in 2023, with outright bans coming in 2024 or early 2025 after the elections. Meaning that you as an individual probably still have about 2 years where the convenience of a centralized exchange will still be available to you. Phrased another way… you have 2 years to learn. If you do learn, the governments ban on crypto will be absolutely meaningless to you. If you don’t learn, it will have a massive impact on your life.

This runway is how long I expected us to have the ability to freely withdraw and deposit to centralized exchanges before the ability to do so is restricted or removed entirely. It’s been roughly 6 months from then and my view on this hasn’t changed at all. Meaning I believe there is only 18 months left to learn.

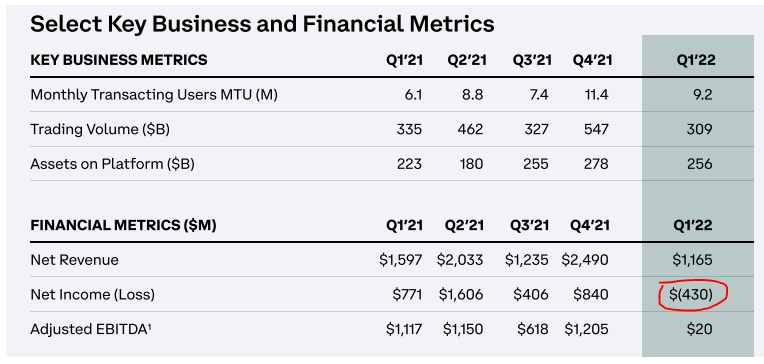

Coinbase, when they had their IPO, were forced to submit to the same SEC regulation that all publicly traded companies submit to. Part of those requirements include making public filings and statements as well as fairly strict financial reporting requirements. The first recent release from Coinbase that we’re going to talk about is their 2022 First Quarter Shareholder letter, within which they reported a $430 million loss.

Of note, this loss is from their operations up until March 31st. 2Q will probably be even worse than the first quarter. Essentially since Coinbase went public, they have missed earnings basically every single quarter, and I actually decided to make my substack after I made a post on Instagram last year about Coinbase missing their 3Q 2021 earnings in the middle of a bull market and why I expected that trend to continue.

The stock was still ~$360 back then, today it’s barely trading above $60. In a bull market (which we were in when I made the post above), people were withdrawing and taking custody of their crypto (which they should), which was decreasing the amount of collateral they had on hand to facilitate people trading in and out of crypto. Meaning that they had to market buy crypto at the top of the bull market to replace assets being withdrawn from the platform. The liquidity they have available for users of the coinbase wallet to open a short position is dependent on how much crypto they hold at any given time. Replacing “cheap” bitcoin that they had been holding from the start of the bullrun with “expensive” bitcoin that they had to buy at the top, especially at volume they didn’t predict is one of the reasons they missed their projections. Coinbase’s main form of income is collecting fees as users trade in and out of positions on the platform. I don’t know what volume of trades they need from a user before that user withdraws assets in order to be profitable, but I would guess that users have been withdrawing assets quicker than projected or modeled based on behavior in the 20teens (2017-2019). I suspect that a far larger portion of people in crypto are taking custody and engaging in DeFi off of the centralized exchanges today than were in 2019. This is partly because there are far more options, UI is far more user friendly, and the DeFi summer of 2020 probably made opportunities more visible to a greater number of people. This substack, for instance, could not have happened in 2019, maybe 2020. But right now, and moving forwards, I expect more and more people to be turning towards self custody.

Lets look deeper at Coinbase’s $430m loss in 1Q. As a reminder, once you issue public shares of stock for exchange, you subject yourself to regulation from the SEC. Here is an example of such. The SEC issued a letter outlining some accounting guidelines for all publicly traded companies that hold crypto assets for platform users. Yeah, it’s a specifically targeted letter, and right now, I’m pretty sure that letter explicitly applies to Coinbase, maybe MicroStrategies, and nobody else. Among other things it required Coinbase to record crypto-assets that are held on behalf of others as liabilities on their balance sheet. Taking a deeper look into their 1Q letter, roughly $730m of their liabilities were customer assets, which adjusted their net-cash to negative ~$830m. If we ignore the customer assets as liabilities, their 1Q would have likely shown closer to $120m in losses, rather than $430m in losses. I’m explaining this difference for context, not because I think it actually changes my outlook for Coinbase moving forwards. My expectation is for Centralized Exchanges that have public stock to actually embrace and encourage regulation making it harder for users to withdraw assets, since that will make the accounting easier and likely make projecting future operations easier.

Now here’s the 2nd part that people are freaking out about. Coinbase, like all publicly traded companies, has to file a quarterly report with the SEC. These are public documents that anyone can view if they wish to. Full document Linked here. Within that document, the following statement appears.

Moreover, because custodially held crypto assets may be considered to be the property of a bankruptcy estate, in the event of a bankruptcy, the crypto assets we hold in custody on behalf of our customers could be subject to bankruptcy proceedings and such customers could be treated as our general unsecured creditors. This may result in customers finding our custodial services more risky and less attractive and any failure to increase our customer base, discontinuation or reduction in use of our platform and products by existing customers as a result could adversely impact our business, operating results, and financial condition.

When an entity goes bankrupt, there is a specific order in which creditors get to split up the assets of the bankrupt entity in order to be made whole. If you have a mortgage on your house, or a car note and you fail to pay it, then your home or car are assets that your creditor gets primary rights to. Some of you may be familiar with the term “lien.” If an entity has a lien, it essentially establishes that entity as having the highest claim on that property. If, as an example, you were to go bankrupt and you had 2 homes with mortgages on them. The primary creditor on your bankruptcy would normally be entitled to claim your 2nd home (the one you don’t live in) to recover your funds. But the bank that gave you the mortgage has a lien on the home, and so has a higher claim to it than the creditor that you are bankrupt to. How this relates to Coinbase, is that they are telling everyone that if they were to go bankrupt, and you hold assets on Coinbase, you would not have the highest claim to those assets, their secured creditors would. This is true. This has always been true.

Not your keys, not your coins.

The CEO of Coinbase put out a Twitter thread to discuss the company’s stance on the letter, he basically says that your assets are safe because Coinbase is unlikely to go bankrupt any time soon. I genuinely believe this is true, but notice he does not say you would be protected in the event of a bankruptcy. He instead says that it’s likely the bankruptcy court would not rule in a way that was harmful to customers, but he can’t know the actual truth of what would happen, because no precedent exists yet. If you have not already, take custody of your coins.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.