May US Treasury Bond Auctions

A brief respite

I have now segregated US bond auction updates into their own separate post. This is the 2nd of a monthly series of posts updating the bond auction rates and bid to cover ratios. I have previously covered these within the weekly updates. I consider this to be the most important part of what I am covering on the substack and it is where we will see the first signs of distress within the market that the federal reserve cares about the most.

You can view last months post here.

Please refer to the Backdrop Post and trade with mindfulness.

Please refer to Definitions page for any terms or abbreviations that I use that you don’t understand. If a term is missing, please let me know.

Table of Contents

State of the Narrative

Primary Auction Results May

Bid to Cover Ratios

Interest Rates

Secondary Market Treasury Rates

Market Impacts

Decrease in Treasury Auction Size

Overnight Reverse Repurchase Markets

Conclusion

1. State of the Narrative

As usual we will start out with a State of the Narrative, this one will be shorter than the initial segment in February as we simply have to cover the changes over the last month.

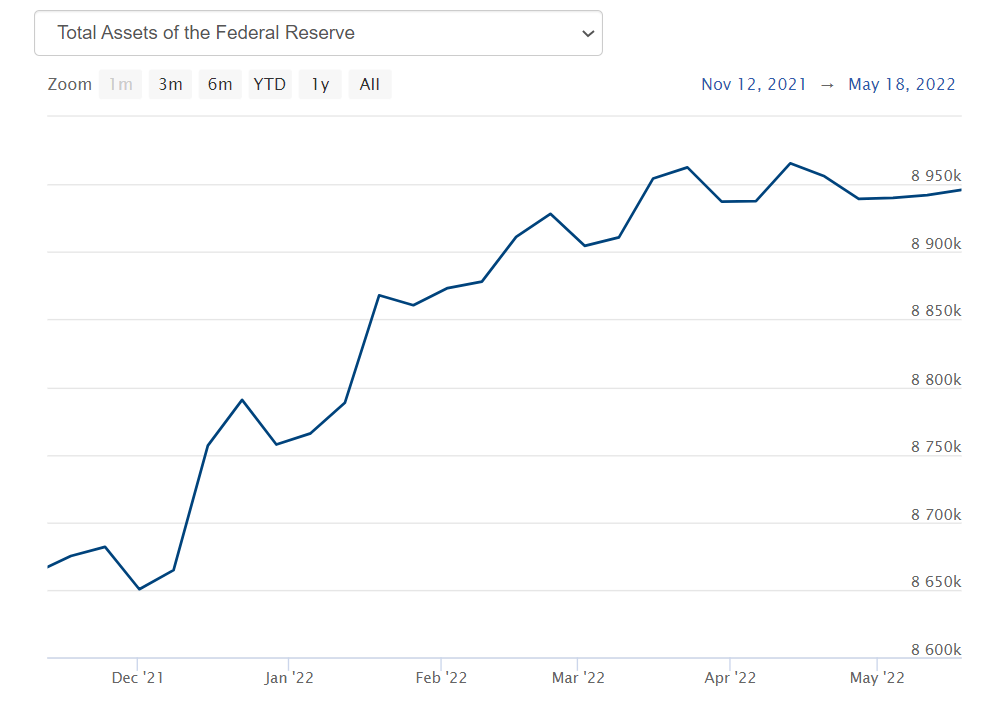

It is now clear that the Federal Reserve has completed their taper as their balance sheet remains flat.

We are all essentially waiting for the Fed to start selling it’s assets back into the secondary markets in roughly 8 days from now (Wednesday June 1st). It’s plausible they may push that back all the way to the middle or the end of the month of June, but they have already delayed one month, and I don’t think they can do that again for another month, so I suspect we will see the start of an attempt at Quantitative Tightening in June. This amounts to a brief pause for the moment in terms of the grinding down of asset prices, but expect that trend to pick up again around the middle or end of next month.

For continuity sake, below is the same chart of the yield from the 2 year US treasury note that I have provided in every single one of these treasury bond posts. Each post has been accompanied by an orange dashed line to better help you to visualize how much yields have grown over the course of a month. As you can see below, the rate of interest rate growth topped out during the month of May and is essentially flat. We’ll go into why in the later sections.

Since last month the Federal Reserve has not backed off of their plans to begin selling additional treasuries into the secondary market next month, so I suspect that the brief break we got over the month of May will be short-lived and the trend will pick up again in earnest in mid-late June or early July. For now we may get a brief sideways market in assets, again, I will get into why that is in Sections 3 and 4. There is a mechanical reason for the market to have come back into balance for this short period.

But, lets jump into this now and begin with our usual assessment.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.