Welcome anon to another week of paid (this ones free!) content.

Please refer to the Backdrop Post and trade with mindfulness.

Please refer to Definitions page for any terms or abbreviations that I use that you don’t understand. If a term is missing, please let me know.

This post will be too long for the email, please come to the substack website.

Substack has launched an iOS app for those of you using apple devices. I am an android peasant and can’t tell you if its good or not, but check it out if you have an iPhone or some other such trappings of royalty.

Please feel free to skip around or ignore certain sections if it does not apply to you. The Table of Contents is made to preserve your time in this manner. You can always simply read the conclusion if you are in a hurry.

All times given in this update are in US Central time (UTC-6 clock).

This post is free for all readers as we have reached a new milestone in subscribers. I will be giving away a 1 year subscription in the comments, all users are eligible whether you pay or are a free subscriber. Details in Section 1. Winner will be Selected Friday July 1st.

Song of the Week - Tyler Childers - Nose on The Grindstone

Table of Contents

Give-Away and Consensus

Economic Calendar

US GDP Growth Q1 2022

G7 Import Restrictions on Russia

Russian Default on Bond Debt

Central Bank Speeches

ECB Speeches

BoE Speech

US Fed Speech

Crypto Macro

Bitcoin Short ETF

Bridge’s and Interoperability

Price Action

Conclusion

1. Give-Away and Consensus

Substack has been a bit of an experiment for me, as much as it has for all of you that are following and paying to read it here. I’ve often been trying to figure out just what it is and what types of posts you gain the most value from, and which ones are the least valuable.

Over the past 3 months, I had actually come to what was probably the wrong conclusion that these weekly breakdown posts were of less value, while some of the crypto guides were of more value. But this may not be the case, and the truth is that I have a bi-cameral audience. There is a fairly significant split in the groups that are reading me, and I was listening too much to only one group. When I got to go to Consensus in Austin a few weeks ago, I had the pleasure of getting to speak with some people in person who have done me the charity of subscribing to this substack and I heard a different side of what it is people value.

As far as I can see it, there are two groups reading this. One is my dissident Libertarian Audience. They want to learn more about the financial world, crypto, etc. but may be fairly new to some of the terms and topics. They benefit a lot from the intro and explainer posts. The other group are crypto natives who want to learn more about the fixed income (treasury bonds) side of things and how the pricing of money impacts the crypto markets on a regular basis. They benefit a lot from the weekly posts and the monthly treasury bond updates.

I also have to note that my initial value proposition was for a weekly update, which I eventually moved to a bi-weekly update in April. You may be surprised to hear it, but these weekly update posts are probably the easiest ones for me to make, while the one off posts and explainers on crypto take more time and effort. Obviously that’s because these have a set format and are repeatable. The conclusions are iterative, and I am mostly building off of what I have already stated and can link back to. In April when I was still getting settled in and fighting my laptop, I had thought that if I decreased the frequency of the weekly posts that I could put out more of the the one-off posts. This was true, but I think this represented a mild betrayal of my audience. And a betrayal of myself in some ways. It’s very important that we all play not only to our strengths, but to our unique strengths. Yes, I can explain most crypto concepts and dApp functionality to an extent, but not to a unique extent. I’m finding that when it comes to explaining the ties between the treasury markets and the broader financial markets that I am more unique in that sense. When we play to our unique strengths is when we can provide the most uncommon value. Ultimately why pay to read here, what can be found for free elsewhere? The paywall has to have uncommon value behind it. It has to be things you can’t google. Better, it has to be things that google will mislead you on if you lack the right perspective. Consider the tweet and info-graphic below.

The tweeter is trying to make a point on currencies, inflation, and their function as a store of value. This tweet is both right and wrong, in a number of ways, most glaringly to you as a reader is probably Japan’s reported inflation rate, and probably beyond that, essentially every reported inflation rate in the info-graphic. They are mostly wrong. How could you know which countries have viable currencies, and which are circling the drain? How will you discover how and when these currencies will collapse and how that will impact the markets you trade? You can’t google that. And so that’s what I will be focusing on. But, I wanted to get feedback from you, the users. Whether you pay or are a free subscriber, please tell me in the comments which posts you gain the most value from (or maybe what your favorite post is and why), and which posts are of no interest to you.

I want your feedback, but obviously through the lens of my own opinion stated in this section above. I don’t care if you are paying or free, or if you have already won a free subscription from me. I really value your feedback, and it helps me to steer the ship, so to speak. I will give away a 1 year subscription to a randomly selected answer on Friday July 1st. If you wish to provide feedback, but do not want to be included in the drawing, perhaps to help those who may be in more need than you, than simply ask to be excluded in your comment and I will respect those wishes.

I’m not going to stop making any specific type of post, but I am returning to making these weekly posts every week on Sunday/Monday to start the week and on Friday/Saturday to end the week. The $FTM review is still coming (lol, this is what I’m talking about), but it will just be ready when it’s ready, as it’s more of a treatise on hype within the crypto space than it is a review of a protocol at this point. We will be sticking to a minimum 2 paid posts a week, aiming for 3 a week. I will try to continue my current trajectory of 2-3 free posts a month as well, but that is obviously not my priority.

As far as news goes, this is a relatively slow week, we will be exclusively focusing on Central Bank Speeches for indications of any weakness or wavering from their set plan. Of note this week it’s the ECB, The US Federal Reserve, and the Bank of England. All relatively important in terms of the near term. For Europe, we will be watching for any further weakness beyond what they already displayed 2 weeks ago when they backed off and admitted additional support for the toxic bonds from Italy, Greece, Spain, and others. For the US Federal Reserve we’ll be listening for any hints that QT has definitely started, and how long they think they can continue it in the face of continuing eye-melting yield increases in the US treasury market. From the Bank of England, we’ll be looking for any hint of heroism as so far they have not yet displayed any but it is necessary for them to take on the burden if they wish to save their population’s ability to earn a decent living from an honest wage.

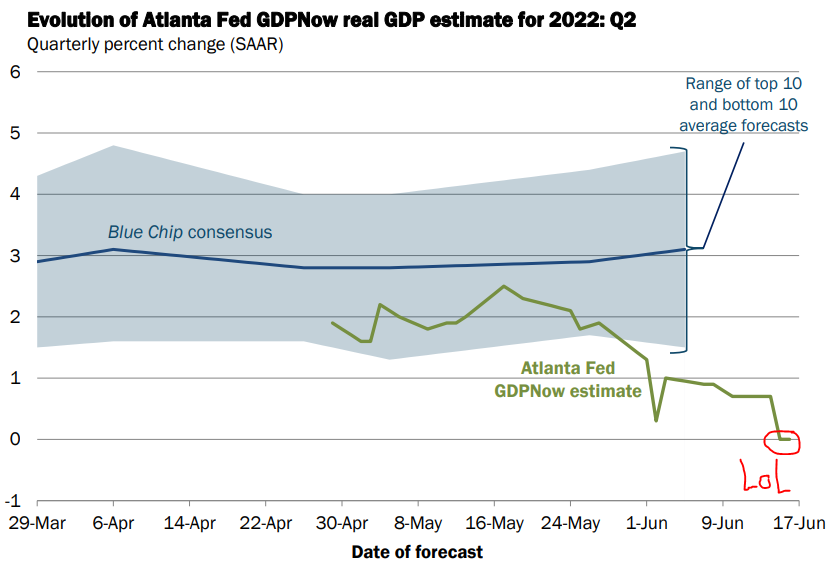

The other big item we’ll be watching is the finalized US Q1 GDP growth (lol) number. As you know Q1 was negative and they have been continually walking down their estimate for Q2. Last week they had their estimate at 0%.

We’ll discuss that further below. But first, take a second and just soak in how far off base the “blue chip” estimates are. Imagine, in this economy, predicting a 3% GDP growth for Q2 as recent as only a few weeks ago, in the face of continued rising inflation. But then again, these are the same nerds who were predicting peak inflation. Of course they’re getting this number vastly wrong as well. All of the bad economists are paid to be economists. All of the good economists don’t need to be employed.

3. US GDP Growth Q1 2022

So when the initial Q1 GDP number came out negative it was a bit of a surprise to me, that post is linked here, and you can read the section if you want a decent background on how GDP is calculated.

The main factors behind that negative print were a significant further shift negative for our trade balance. We import far more goods than we export, and our net trade balance plays into GDP growth; for obvious reasons, the D in GDP stands for Domestic, after all. I don’t see that trend having changed at all. The other major factor that made last quarter negative is the deflator from inflation pushed GDP down as well. Inflation has of course not improved, with last months inflation being the highest of this current cycle. We can presume that Q1 Inflation figures aren’t going to improve after further investigation, in all likelihood they’re worse. Beyond that, we’ve covered how many companies reported significant contractions in their Q1 earnings and most fell below projections with several reporting a loss. I don’t expect that trend to have changed in the past 3 months either, with fuel costs, and unexpected inflation playing into many companies coming up negative.

Please note, this weeks number is the finalized figure for Q1. We won’t get Q2 until next month.

The number we’ll receive this week is likely going to confirm the negative 1.5% that we got for Q1. It’s unlikely that it will diverge much in either way, but this will be the finalized number for Q1 GDP. I’m expecting no surprise here, but reserving a space for this just in case.

Germany currently lacks the infrastructure to import Natural Gas from anywhere else as they were wholly unprepared for the consequences of their own attempts at sanctions on Russia.

The west, as an economic hemisphere is totally lacking in the raw goods needed to sustain itself, and it’s workforce is currently not positioned to pivot to the necessary production that it has outsourced to the East. There is simply not enough infrastructure and raw goods to go around for Europe, North America, Japan, and Oceania. The rest of the world will have to decide which economic sphere to join. This newest move from the west to block Russian Gold exports is just a further move in restricting the transfer of value to the west for our valueless paper money. It is sad because we are doing this to ourselves. We should be attempting to extract as many resources from Russia as we can at this point, and we should have been attempting to establish our independence from Russia and China over the past 2 decades. But we didn’t do that, and just presumed they would remain under our thumbs for as long as we pleased.

Unfortunate coincidence, Russia and China lead in mining capacity

The result of us blocking Russian Gold exports is simply that any country wishing to trade with Russia will be able to get Gold at a discount, while any country unwilling to do so will pay a higher price for Gold.

Any basic economist could tell you what would happen in that case. People with money to buy things will go where it’s cheaper, and people with goods to sell will go where it’s expensive. And people with access to both markets will buy from the cheap market to sell to the expensive market (this process is called arbitrage). And at some point, China and Russia would likely enact a rule that anyone using their system (CIPS or SFPS) would be removed if they were also using SWIFT in order to end the arbitrage opportunity. There’s no reason why they wouldn’t take that opportunity to starve the West of energy.

What happens when our trading partners don’t want Euro’s and US Dollars because they can’t use them on the global market because anyone trading with Russia and China has no use for these currencies in broader exchange?

Currently a Russian civilian has no use for US Dollars because we’ve blocked their ability to transact with them. Those dollars are now just worthless paper. So anyone trading with a Russian, can’t pay them in Dollars or Euros. They have to use something else. This is of course why Russia is forcing European countries to pay Gazprom in Rubles, why would they accept Euro’s they can’t use? Now what happens when Europe runs out of Rubles to buy to then use to pay for oil and gas? No one is talking about this yet, but their FX reserves of Rubles are not infinite. And unless they are exporting goods to Russia, they have no new sources of Rubles. This can’t last forever.

If we can’t trade our own currencies to them, the only thing we’ll be able to trade on an international scale will be Gold, and of course we are in the middle of cutting off one major supplier of Gold Bullion to the West. The trade balance problem the US has is going to bite us majorly right when we are least able to afford it. So long as we import significantly more than we export, our currency will lose value when it is no longer accepted on an international scale. When the day comes that a US Dollar can only buy goods in the US, Europe, Japan, Canada, The UK, and Australia, that will significantly decrease the value of the dollar. Especially since most of the countries in this list are also net importers and will be having the exact same problem with their own local currency. We’ll essentially have a market flooded with paper chasing very few goods, while the Eastern Sphere will have the exact opposite problem.

This is not a good thing, and this is extremely incompetent foreign policy. Sadly, the closest thing the world has right now to Paul Volker is Elvira Nabiullina, she is the current governor of the Central Bank of Russia. You’ll note they are one of the only countries involved in this conflict running a budget surplus that also has an overnight lending rate that is higher than the inflation rate. At the very start of the conflict, you’ll note that Russia hiked it’s overnight rate from 9.5% (which was stable and above inflation) to 20%. Within a week, that was done. They run a budget surplus, so their treasury could afford this, of course. We’ve only see record profits for their nationalized oil and gas industry since then, of course. The ruble is… of course… the currency that has seen the strongest growth this year.1 And we’ve just gifted them more gold, and we are holding back our rapidly inflating currencies in exchange. I couldn’t invent a worse trade for the West if I tried.

People who bought Russian Government Bonds, in the same way that people buy US bonds, are owed a certain amount of money when those bonds reach maturity. I could swear that I covered that on here as well, but I can’t find the post. Essentially in May, the US Treasury through Janet Yellen blocked Russia’s ability to make any further payments on debt owed. That started a 30 day countdown, as terms on the Russian Bonds allowed a 30 day payment window, which expires tonight. The US Treasury is still blocking Russia from making those debt payments despite Russia having the money to do so. Such will result in a Russian default on debt and a decrease in the Russian credit rating. This is kind of a laughable attempt from the West to block Russia from access to credit markets. But Russia was not running a deficit prior to the invasion and had little need for access to credit markets. After their invasion of Ukraine and some of the sanctions, their surplus turned into a small deficit of $21.6 billion in April. But since then they have seen record profits in their exports, so I’m not sure if they are still running a deficit anymore.

According to Russian Sources, they are now running a budget surplus of ~$16 billion, but I’m not sure if this is a credible figure or not, but the budget deficit for 2022 could credibly arrive at 2% of GDP by the end of the fiscal year. Russia has enough reserves to cover this without having to access the global credit markets at all, and simply relying only on internal demand from balance sheets and reserves held at Russian banks. This move is ultimately only going to hurt those western creditors that had bought Russian bonds. Russia essentially is being gifted money, and the only negative outcome is a downgrade of their credit rating in the western world. When countries sever themselves from the western financial world in order to engage in trade with the Eastern sphere, they simply won’t care what the Russian credit rating is in our sphere. It’s the beginning of a parallel economy, what we do in ours is less and less relevant to their sphere.

6. Central Bank Speeches

Many central bank officials are going to be attending an event in the Portuguese Riviera this week about monetary policy. These include several prepared remarks from the major central bankers in the western sphere. In general, an event like this is for prepared remarks, but sometimes you can get a hint about how the western central bankers as a whole view the fiscal environment of the west, especially moving forwards. I would be curious to see if any disputes arise, because when they speak to their own citizens, you’ll note they often blame their own problems on other countries. Japan, for instance, blames inflation in the US on their rising cost of imports. The ECB might point to the US or Swiss bank raising rates as putting pressure on them. The Bank of England might blame inflation on another bank holding rates low. Who knows? I don’t expect this level of infighting from them, but it’s not exactly off the table considering how strained these bankers currently are in prisons of their own making.

ECB Speeches

We’ll start with ECB head, Christine Lagarde I would expect most of her comments to be very canned and not representing any surprises, but it’s possible she may comment on the ECB’s ability to credibly stop printing money in July and to raise interest rates. She may also give us some insight about the ECB’s relationship with the Swiss National Bank and their rate hike of 0.5% which most of the financial world was somehow surprised by. We’ll mainly be listening for any hints of weakness in their resolve to raise rates, but this is not the sort of platform where the head of the ECB would make any waves, so I wouldn’t expect her to. I am reserving a spot so you know to be aware of these speeches just in case she surprises us with something out of left field.

BoE Speech

The Bank of England we’ll mainly be listening for any hints about increased urgency in their planned rate hikes. They’re currently moving far too slow, and I’d like to see them pick up the pace, especially since they are one of the few western countries that can afford to do so.

US Fed Speech

Jerome Powell also has a speech planned, and I expect much of the usual nonsense that we get from him. Will give it a listen, but only with a passing ear as I expect nothing of any substance or change in tone from him here.

Yes, lol. That’s right, the SEC approved an ETF that allows you to open a short position against bitcoin on the NYSE (New York Stock Exchange), but they still won’t approve a spot Bitcoin ETF. As far as news goes, this is mostly meaningless and will have no affect on the market, however I find it funny since there was so much opposition to the spot ETF.

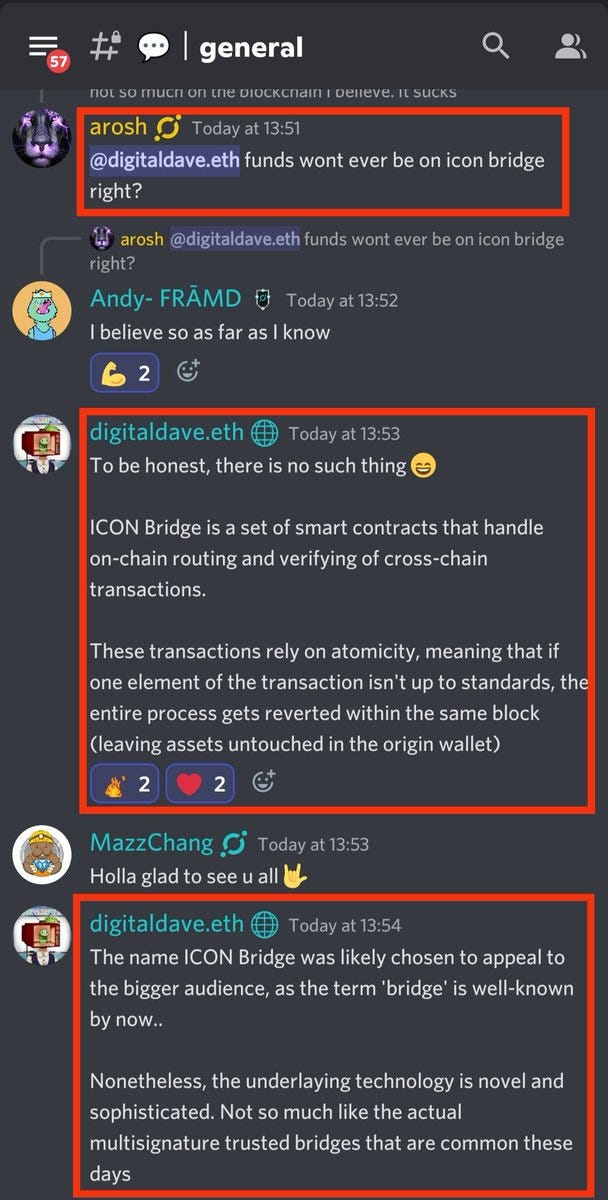

Bridge’s and Interoperability

Going back to our main theme that we are tracking in the quarterly Macro updates there was another significant hack of a bridge last week.

The bridge involved a multi-sig with 4 verifications to authorize transactions. It’s very likely that 2 of the node’s verifying transactions were compromised and used to authorize malicious transactions. The wallet address where all of the ETH held by the bridge was re-directed to is below. They got almost 86k ETH for a market value of over $100 million at the time of writing.

As has been outlined in the Quarterly Crypto Macro posts, this is the problem that will be solved by the major interoperability protocols this year and they will likely see a massive rise in valuation for whichever chain solves the problem and captures market share for doing so. The protocols outlined in the Crypto Macro post all solve the problem of “bridges” by using the inherent security of the blockchain itself to verify transactions, rather than relying on vulnerable nodes to authorize transactions.

The above chat is from the $ICX discord, but keep in mind that $ATOM does nearly the same thing, $DOT is tied in to both $ICX and $ATOM, and $LINK’s solution whenever it does get rolled out will probably function in a similar manner. Ultimately this is the next big trend I expect to arise in crypto. The ability to wrap tokens and send them to another chain in a fully trustless, decentralized manner. The Bridge’s that we use right now are just… a bridge… to the inevitable future where the security of these sort of transactions are handled by the security of the blockchains themselves.

Price Action

Not much to update from the post that went out reviewing last week, so I’ve copied that text below.

It seems we’ve finally found a mid-term bottom (for now) with Bitcoin not pushing down into a lower support zone. As I suspected there simply wasn’t much juice left to squeeze in a bitcoin short, and seeing how much buying action FTX and Alameda went in on buying Bitcoin and buying up distressed assets, they may have set the short term bottom for bitcoin.

BTCUSD 4 Hour chart

Bitcoin recovered back above the previous high from the last cycle of $19,690 and stayed above that support zone for the majority of the week. ETH performed similarly and looking forward we can expect both assets to be flat in the short term moving forward.

I’d expect price to be relatively stable in the short term, while the current macro of flat/down will persist. Please be mindful of the conclusion provided in this month’s US treasury auction post. We likely saw a short term bottom put in, and can expect for another swipe low in the future when the Fed is forced to act that may present a double bottom, or an even lower price than what we saw a week ago. That price in the future will represent the actual Secular bottom for the market.

8. Conclusion

The West is still punching itself in the face with the hopes that it will find the strength to win if only it hurts itself enough first.

For those of you that haven’t seen Four Lions yet (hilarious film), I’m going to spoil it for you. Nobody ever won a fight from self-inflicted wounds.

When I say the Ruble has seen the strongest growth this year, that statement needs to be understood in context. In the international FX exchanges, the Ruble has grown the most; what sorts of transactions occur in those exchanges? Mainly between central banks and large institutions. With the sanctions placed on those exchanges, most of the transactions are one way. Western institutions, putting in western currency, to purchase Rubles to use to buy goods from Russia. We are blocking most of the other side of these transactions, so in this marketplace, of course the Ruble is going to appreciate, because 90% of the volume selling the Ruble, has been blocked.

The experience on the street of the average citizen of these currencies is probably different. Are food prices going up in Russia, gas, base commodities? I don’t know the answer to that and couldn’t tell you. But it’s important for you to be mindful of this gap in our understanding. It’s one thing to say a currency is appreciating in a very specific market against another counter-asset (the US Dollar). It’s another entirely for it to be strengthening outright and for the economy to be experiencing deflation. We know that the first thing is happening, we have no way of knowing from the western world if the second is occurring with any real specificity.

Whatever I find most engaging I'll usually comment on. I can't really say what is my favorite bc it all kind of merges as what I file in my head as your takes if that makes sense. I don't see anyone covering the treasury bonds and FOMC to the depth that you do which gives me more trust that you do your own analysis and theories into what seems to be the economic crux. The crypto stuff is still slightly different than the others I'm now reading so it pairs well, sometimes it's too technical for me and I'll read it anyways so that maybe I will learn through literary osmosis - it still helps bc I catch things without knowing what they really mean but know it's bad or not, or seem to. I traded a lot of what I was holding for bitcoin several weeks ago bc something urged me to and I'm glad I did. Some of that was just on principle of WEF too.

I like the off topic cultural observations as well keeps it engaging and human.

I'm here for all of it, the insights & possible scenarios on macro, as well as crypto lessons are all very enlightening as I am a beginner. I'm just curious regarding your economics background, since i reckon these knowledge is not gained from just being an outsider. Thanks!

Whatever I find most engaging I'll usually comment on. I can't really say what is my favorite bc it all kind of merges as what I file in my head as your takes if that makes sense. I don't see anyone covering the treasury bonds and FOMC to the depth that you do which gives me more trust that you do your own analysis and theories into what seems to be the economic crux. The crypto stuff is still slightly different than the others I'm now reading so it pairs well, sometimes it's too technical for me and I'll read it anyways so that maybe I will learn through literary osmosis - it still helps bc I catch things without knowing what they really mean but know it's bad or not, or seem to. I traded a lot of what I was holding for bitcoin several weeks ago bc something urged me to and I'm glad I did. Some of that was just on principle of WEF too.

I like the off topic cultural observations as well keeps it engaging and human.

I don't know want to be considered for anything.

I'm here for all of it, the insights & possible scenarios on macro, as well as crypto lessons are all very enlightening as I am a beginner. I'm just curious regarding your economics background, since i reckon these knowledge is not gained from just being an outsider. Thanks!