Review 6/27/2022 - The Sun Rises in the East

And Sets in the West

Welcome we will be reviewing macro events from this past week from The Post I made at the beginning of this week on 6/26/22.

I have added a Definitions page which will include all of the terms and abbreviations that I use from now on and will be referred to on every post.

Substack has launched an iOS app for those of you using apple devices. I am an android peasant and can’t tell you if its good or not, but check it out if you have an iPhone or some other such trappings of royalty.

Please feel free to skip around or ignore certain sections if it does not apply to you. The Table of Contents is made to preserve your time in this manner. You can always simply read the conclusion if you are in a hurry.

For This weeks giveaway I used Wheel of Names and ElliotVreeland was the lucky commenter. They are already a paid subscriber with a 1 year subscription. Their subscription will be extended for an additional year, and won’t be asked to renew until 2024, at which point hopefully this entire platform functions on BTC anyways, lol.

Thank you all for your feedback, it was very valuable to me and I will continue to do these giveaways everytime I hit a subscriber milestone as a way to giveback, so I’m sure there will be another one within the next month.

A note, I excluded commenters who requested not to be included in the giveaway, and I excluded one commenter who had already won a free 1 year subscription in an older competition.

Table of Contents

Central Bank Speeches

US Q1 GDP Growth

Final Q1 GDP Number

Q2 GDPNow Forecast

BRICS and the Eastern Trade Sphere

Crypto Macro

Mechanical Liquidations

Price Action

Conclusion

1. Central Bank Speeches

The conference in Sintra was a shitshow. In the western hemisphere, central bankers have mostly been an embarrassment, however there was at least a veil of uncertainty that persisted where people would presume that maybe our leaders actually were smarter than the average person but were intentionally enacting harmful policy for their own benefit.

That illusion will slowly break.

Western Central bankers don’t even know what inflation is or where it comes from. The guy at the grocery store who tells you which aisle the milk is in was telling you that printing money was going to cause inflation back in 2020. These aren’t rare insights. Your mechanic probably told you. Your plumber probably told you. You yourself probably commented on this phenomenon as an incoming concern. Yet here is Jerome Powell admitting that 34 out of 35 of professional forecasters were blindsided by the increase in inflation. Note that his comment is that the only thing they’ve learned is that they’re ignorant about inflation. They still don’t know what it is. That should be chilling, or as Bloomberg’s host said “that’s not reassuring.” You as a citizen of a western nation (especially the US, Japan, or the Eurozone) need to internalize this and then think about the consequences.

If they don’t understand the cause of inflation, then they are likely to cause it again even while believing that this time it’s different. Consider what Governor Lowe said about his plans for the Royal Bank of Australia in his speech last week.

We now expect this more aggressive approach to see the US economy stalling, with the risk of a mild recession in the second half of 2023. We expect a need for a series of rate cuts from December 2023 eventually taking the federal funds rate back to 2.125% through 2024.

The Australian Central Bank is already planning rate cuts for 2023, and that’s in the face of their current inflation and the ongoing energy crisis. It is almost an inevitability that the US, and EU will be following in Japan’s footsteps with full yield curve control and money printing. They are scratching their heads on live TV (admittedly, very few people watch these), and telling the investing public that they still have no idea how inflation occurred, and that nobody in their circle was able to predict this. I tend to believe them when they say this.

You look at the current college curriculum for economics, and the kind of people who come out with pH.d’s in economics and it’s complete trash that is nearly entirely divorced from fiscal realities. If you’re science can’t accurately predict the ebb and flow of inflation and the value of assets, then it’s not a science. We are watching the results of education systems dominated by Modern Monetary Theory for decades. They really believe that they can just print money whenever they want and have no consequences.

Now here’s the real kicker. For as long as these central bankers have been paying attention, that was actually true. Consider my example from the beginning of the week.

What happens when our trading partners don’t want Euro’s and US Dollars because they can’t use them on the global market because anyone trading with Russia and China has no use for these currencies in broader exchange?

Currently a Russian civilian has no use for US Dollars because we’ve blocked their ability to transact with them. Those dollars are now just worthless paper. So anyone trading with a Russian, can’t pay them in Dollars or Euros. They have to use something else. This is of course why Russia is forcing European countries to pay Gazprom in Rubles, why would they accept Euro’s they can’t use? Now what happens when Europe runs out of Rubles to buy to then use to pay for oil and gas? No one is talking about this yet, but their FX reserves of Rubles are not infinite. And unless they are exporting goods to Russia, they have no new sources of Rubles. This can’t last forever.

For the last 40 years, countries around the world have had to buy US dollars in order to trade. The US central bank, and to a lesser but not insignificant extent, the ECB and BoJ have had to manage foreign demand for their own currencies. Due to the amount of dollars demanded worldwide, the Federal Reserve often has to manage how many dollars are available internationally to facilitate global trade. It’s just as much of a crisis for our allies to be forced to buy dollars in an illiquid market as it is for Russia to stop exporting oil and gas to them. Back in 2020 during the market crash in March, many global swap facilities were actually running extremely short on dollars as the supply in circulation was far short of the international demand. Part of the money that was printed in that time was used to provide additional liquidity to these swap markets so that major trading partners could have access to US dollars without running out of liquidity. Ironically, the initial move to bolster the international dollar markets marked the exact bottom of the March 2020 markets.

Knowing that there is this level of demand for the dollar internationally, it is then not so much of a stretch to conclude that a certain portion of Dollars can be printed every year so long as the dollar is the international reserve currency and accepted everywhere as a unit of exchange. The problem for Modern Monetary Theorists, is that they do not understand that global demand for the dollar is what supports US deficit spending. In order to keep the dollar from strengthening too much, some printing in that environment could be seen as “necessary.” And if some is “necessary,” well you can see how MMT didn’t get laughed out of post-secondary Economics classrooms. They take global demand for the dollar for granted.

This is one reason why your server at Applebee’s would think that inflation is to follow money printing, while government economists don’t think any inflation is coming. A decade ago, your Applebee’s server was wrong, and the government economist was right. Post-2008 we printed $4.5 trillion and pushed the debt ceiling significantly. But international demand for the dollar was fairly strong, and while we experienced inflation, it was relatively mild compared to what we’re feeling today. If you’ve been reading for a while, you can probably tell what the difference is between the 2008 market interventions, and those in 2020. The difference of course is international demand for the dollar.

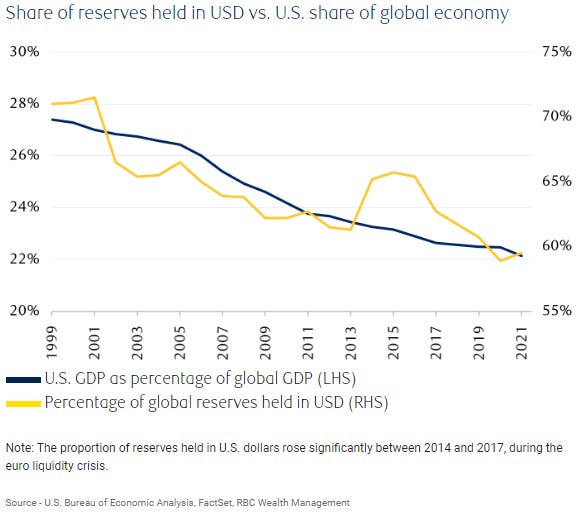

In the year 2000, 80% of global FX reserves worldwide were held in US dollars. At the end of 2021, that number was 58%. I’m willing to bet that this has further dropped since then, and I’ll go further into why that is in section 3. Yes, demand for the US dollar worldwide has been steadily dropping with a brief exception in 2014. That is the difference maker. In 2012, despite the global market being unsure if QE would ever stop after nicknaming QE3; “QE Infinity,” the world still didn’t have a choice about what currency to use for global trade. The Dollar was still king.

Your server at Applebees, your mechanic, and the guy at the grocery store pointing out where the milk is don’t know that this is occurring. Or maybe they do? And Modern Monetary Theorist’s haven’t considered how large of an impact this has on their ability to expand the money supply. If nobody else is buying our bonds, then we have to be the ones to do it ourselves. If the world doesn’t need to hold US Dollars, or Euro’s as FX reserves for global trade, then they no longer have to buy our bonds. And if they no longer are buying our bonds, then our interest rates are going to keep rising. If our interest rates keep rising, then we can only default or print money to buy the bonds ourselves (Or, lol, stop deficit spending).

The western economic sphere have not sufficiently humbled themselves enough for me to believe that they will make the right choices. In the US, EU, and Japan, things are so far gone, that I don’t believe their governments are capable of cutting spending enough to decrease how many bonds they have to sell to keep interest rates manageable. The conclusion is foregone.

I will undermine my point a little bit by showing how ECB head Christine Lagarde is actively lying to people at the forum. They’re not totally clueless. During one of her speeches, she stated;

her team is ready to raise rates at a faster pace — if needed — if inflation continues to shoot higher

Inflation in Europe is 8.6% according to their broken statistic, but likely much higher. If she really believed what she was saying, she would have raised rates yesterday. Remember how Russia’s Central Bank reacted to the sanctions after the ukraine invasion.

At the very start of the conflict, you’ll note that Russia hiked it’s overnight rate from 9.5% (which was stable and above inflation) to 20%. Within a week, that was done.

The ECB can’t raise rates due to how many countries within the Eurozone have toxic debt and are running atrocious budget deficits, so they delay by telling you that if they wanted to move faster they could, but lol, we’ll do it next month. The central banks may not know where inflation comes from, but they do know that they need to delay rate hikes as much as possible because there is a certain reality to the outcomes that they have to avoid. From our perspective, this is nothing but evil, to a certain class of person, this is heroic. I’ll leave my free subscribers with a quote from a movie scene (that was also filmed in Sintra).

Even hell has it’s heroes.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.