Please refer to the Backdrop Post and trade with mindfulness.

If you’re new and have a question, please read the FAQ post first.

Please refer to Definitions page for any terms or abbreviations that I use that you don’t understand. If a term is missing, please let me know.

This post will be too long for the email, please come to the substack website.

Substack has launched an iOS app for those of you using apple devices. I am an android peasant and can’t tell you if its good or not, but check it out if you have an iPhone or some other such trappings of royalty.

Please feel free to skip around or ignore certain sections if it does not apply to you. The Table of Contents is made to preserve your time in this manner. You can always simply read the conclusion if you are in a hurry.

All times given in this update are in US Central time (UTC-6 clock).

Song of the Week - Max Richter - On the Nature of Daylight

Table of Contents

Bankruptcy Laws and Crypto

Chapter 11?

Economic Calendar

European Interest Rates

Royal Bank of Australia

Japanese Interest Rates (lol)

Crypto Macro

Price Action

Nature is Healing

Conclusion

1. Bankruptcy Laws and Crypto

So, the contagion in the crypto markets that started with the collapse of $LUNA and then exposed several entities with extremely unhealthy balance sheets has mostly finished running through DeFi.

But the CeFi bankruptcies and court litigations are still ongoing and will likely take over a year to resolve. I want to take this time to discuss some of the differences in how insolvency is handled in code vs. how it’s handled in law as well as to discuss some of the implications for Celsius and 3 Arrows Capital.

The first thing to note is that Celsius has paid off all of it’s DeFi loans. They had to. The code will not release your collateral unless you pay off the loan. The DeFi platform will not cuck itself and let you protect your collateral in any sense.

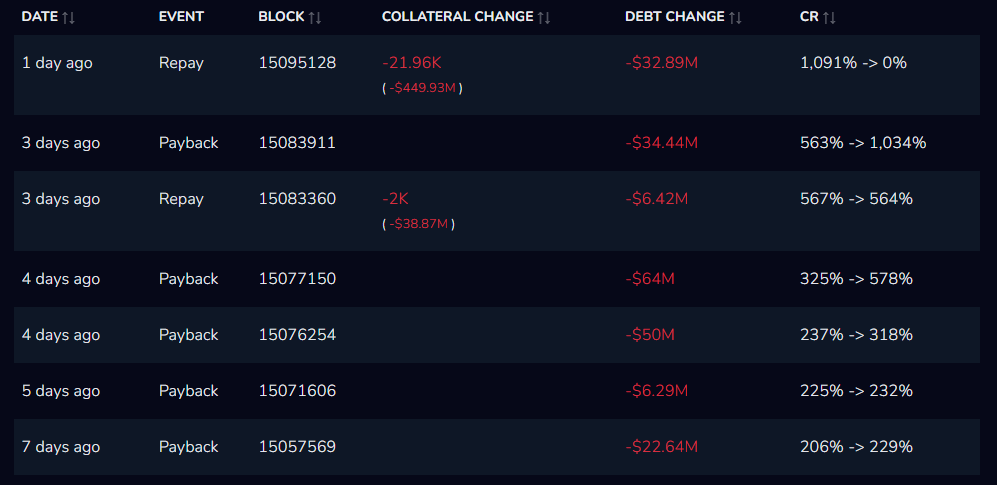

On the plus side, as of a day ago Celsius has paid off the entirety of their loan against their BTC in Makr. This is all on chain and the wallet can be viewed here.

Celsius paid off all of their loan to MAKR

This is a good thing for many reasons. Primarily because there is now no risk that the $440 million of collateral BTC they had locked up on MAKR can be market sold if their loan gets liquidated.

You’ll note that when it came time to pay off their loans, the DeFi creditors got 100% of their money back, while Celsius’ depositors are still in limbo and will be for years. From a user perspective, there is no clearer use case for real DeFi than this. From an investor perspective, the Traditional Finance system is a complete dinosaur. Nobody wants to wait on a court to hear their case for years, while the irresponsible entity that has essentially cheated you out of your funds has plenty of time to abscond and squirrel the money away in any number of legal hidey holes that you have no access to. Worse there is always the possibility for shenanigans and externalities to arise in your legal case that could screw you out of what is rightfully yours. Simply using the court system is a punishment in and of itself, and I would wish such a fate on no one.

Those jobs have a ticking clock attached to them, and in what feels like no time at all, I expect most lending to move to blockchain (either public blockchain or private blockchain) for this exact reason.

This difference in outcomes, expediency, and fairness is exactly why smart contracts will replace the traditional methods of doing just about anything that can be coded.

Now lets pivot and take a closer look at the Celsius bankruptcy proceedings and what’s going on now. The proceedings are just beginning to go through court as exhibits are being submitted and some of those exhibits are making their way online now.

There are, of course, grifters who are trying to convince themselves that the CEL token represents a short squeeze that they can ride for infinite profits because they have convinced themselves that actually Celsius really is solvent. This is not anywhere near the case, and even in this example there is a $2.2 billion hole in March 2022 already as the Celsius team can’t account for the CEL token’s value since they can’t sell it anyways, and even in July 2022, they are still $1.8B short in their own accounting.

You’ve probably been reading several months of news from me about Celsius terrible mismanagement of finances from me on here, but below is a quick recap.

The shorts on the CEL token have it right. I wouldn’t be surprised if the #CELShortSqueeze hashtag on twitter is being astroturfed by Celsius or a bad actor holding a bag who is hoping to push prices a little higher to get some exit liquidity so they can pull more money out of this.

Chapter 11?

Lastly, Celsius and Voyager both are filing for Chapter 11 bankruptcy in the US, but there are several different types of bankruptcy and what you qualify depends on what sort of entity you were and what sort of business you were operating.

These bankruptcies will likely be making case law in the future. Crypto exchanges, by all interpretations should qualify as brokerages. As Thomas points out in the twitter thread above. Chapter 7 bankruptcy applies to brokerages and has protections in place for user deposits, while Chapter 11 bankruptcy does not prioritize depositors anywhere near as high and significantly increases the chances of them never getting their assets back.

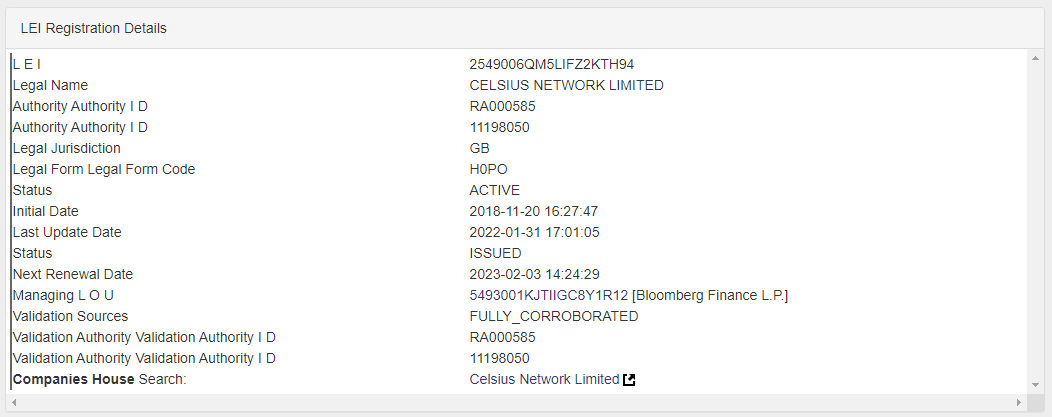

Looking at Celsius’ SEC filings, they were headquartered in Great Britain and had filed to do business in the US.

Unfortunately when looking through many of the other numerous filings against Celsius recently, both Alabama, and Vermont refer to them as a financial services company, and not as a brokerage.

Alabama filing against CEL for selling unregistered Securities

I suspect that the regulatory uncertainty and Celsius’ ability to call itself whatever it wants will likely lead to the chapter 11 proceedings moving forwards and depositors to Celsius will probably be the ones filling the $1.8 billion hole that is currently on Celsius’ books. Ironically, due to the SEC’s vice grip on what is a security and what is a commodity blocking the ability for many crypto assets to trade here in the US without significant legal expenditure, most entities have been primarily operating overseas. While clearly a broker, Celsius likely never was legally viewed as a broker by US regulators because they do not view this market as a legitimate one for people to trade in. Such opaque and difficult regulation is exactly why Celsius will likely be able to get away with defrauding users one final time. Legally, no US entity seems to have recognized Celsius as a broker, so it will be very difficult for the courts to make the claim that Celsius is a broker… according to who? No US regulatory entity, and so they can call themselves whatever they needed to in order to operate to some level in the US.

US regulators will likely use this as a reason to make regulations even tighter to avoid another event like this. But this is of course not an ideal solution and one likely to chase more investment overseas and more potential developers and what would be US companies overseas as well.

This process will likely take at least a year to go through the courts, and the US government will think that this sort of event de-legitimizes crypto, but the truth is, its just another reason for assets to move on chain and to never come back to this system.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.