Review - 9/5/22 The Grasshopper and the Octopus

Giveaway - Forex Invoicing Dominance

This post is free as we hit a subscriber milestone.

Welcome we will be reviewing macro events from this past week from The Post I made at the beginning of this week on 9/5/22.

I have added a Definitions page which will include all of the terms and abbreviations that I use from now on and will be referred to on every post.

Substack has launched an iOS app for those of you using apple devices. I am an android peasant and can’t tell you if its good or not yet, but I will know soon. Substack has announced a waitlist for their android app, which they claim is nearly ready. I’ve signed up for the waitlist and the link is here in case you wish to do so.

Please feel free to skip around or ignore certain sections if it does not apply to you. The Table of Contents is made to preserve your time in this manner. You can always simply read the conclusion if you are in a hurry.

This post was late because I spent all night Friday awake poring over the public blockchain as the victim of an exploit on an NFT marketplace. I cover part of this in Section 5.

Giveaway

I’m including a giveaway in this post because we hit another subscriber milestone. Everyone is free to comment. For a 1 year gifted subscription, tell me which country or place you think would be ideal to move to for you with the considerations of avoiding the most political and financial stress. I will pick a winner next week Friday (9/16).

Table of Contents

The Mind of a Keynesian

Australian Interest Rates

Euro and Dollar Invoice Dominance

EU Interest Rates and Conflict

Greek-Turkey Conflict

Canadian Interest Rates

Crypto Macro

Price Action

A Lesson Learned

Grid+ Wallet

Conclusion

1. The Mind of a Keynesian

This conversation from Powell hosted by the CATO institute is a peek into the mind of a Keynesian.

From this you can get a picture into how a Keynesian views fiscal policy from this interview. You’ll note that when Powell talks about inflation he states that one of their goals by targeting a 2% average inflation is to impact the behavior of the public in order to keep inflation down. From here you can understand why CPI is so broken. CPI isn’t made to tell people what’s going on, it’s purpose is to control behavior. They want the public to expect 2% average inflation and to make financial choices based on an expectation of 2% average inflation. What the actual average inflation is at any given time is irrelevant. Think about the public’s decision making at 2% inflation. There’s enough disincentive for people not to hold cash, while 0% inflation or deflation causes people to hold cash rather than invest/spend. But at 2%, inflation is also slow enough that people aren’t hoarding goods or rushing to spend money as soon as they can. So it makes quite a lot of sense why one of the key moves under Reagan in the 80’s was to readjust the way CPI was calculated to make inflation appear lower than it actually is.

The keynesian does not want to actually hit 2% inflation, they want to be able to credibly tell the public that inflation is 2%, regardless of the fact that prices for basic goods such as shelter are significantly outpacing the statements made by the Bureau of Labor and Statistics. Keynesian’s are never going to be honest with the public, because they are not even honest with themselves. Every statistic, number, and guideline they give you is an act of manipulation; it’s purpose is to mislead your behavior and engineer society. They are not simply economists tracking and managing fiscal policy, they are managing human behavior itself.

The interviewer was underwhelming of course, the CATO institute allowed the CEO of Barclays’ LatAm branch to interview Powell, and almost all of the questions were softballs and he did not press Powell on anything. It’s quite likely that CATO only got the interview if they agreed to ask only pre-approved questions. Bureaucrats, Eunuchs and Politicians do not engage in ad-hoc conversations. They aren’t real people in that sense. Everything is a prepared statement, manipulation of their appearances. In general, this is a rule of thumb for politicians. If they can’t participate in an unscripted conversation, you can’t trust them with a vote. Regardless of party affiliation.

Powell does let some of his personal opinions briefly show near the end of the discussion. He is asked about fiscal responsibility, and his answer was as follows.

At the Fed, my position is- needs to be, that fiscal policy really is the responsibility of congress and the administration. It wouldn’t be appropriate for me to comment too much on specific policy proposals or laws.

This is a true statement. The Federal Reserve is a political position, and a political appointment. You carry water for the administration in power regardless of your own personal opinion. You can hear him self-edit in real time. What he stated is not his opinion, it’s what his opinion needs to be. I’m harsh on Powell, but in truth, just like Greenspan and others, he probably actually knows the real problems and threats to the currency and quality of life of the population. And despite knowing this truth, they accept the job and carry water for congress and the senate despite knowing all of that.

It’s not much solace for your executioner to agree with you as he swings the sword that takes your head off. But I do wonder how much worse the Fed would be if an actual activist were in the seat instead? We would have probably already dived off of the same cliff that Japan is halfway down right now. But ultimately, Powell’s personal opinions will not matter. The administration, and Janet Yellen will push him to support the treasury by reversing policy when the treasury bond market becomes too distressed.

It’s only a matter of time, and when pushed to act… Powell will do his job, just as your sympathetic executioner will still swing his sword.

2. Australian Interest Rates

This week the RBA raised the overnight lending rate by 0.5% again to 2.35%, their official statement is here. The governor is currently under pressure from the Australian Green party to resign as they seem to think he should not have raised rates at all. They represent a minority faction within Australian politics now, but it is indicative of how the public can grossly misunderstand fiscal policy and it’s impacts on their lives. If Australia had followed Japan’s lead and kept printing while holding rates at 0%, things would be far worse in Australia than they are today.

The RBA Governor (Phillip Lowe) has the same excuses that all western central bankers have. His central bank flooded the economy with money printing in 2020, that easy money entered the financial markets and flowed out from there into the commodity and consumer markets. While similarly their productive economy was hamstrung and under-produced during CovID lockdowns and trade/travel restrictions. The value of money is directly represented by comparing the amount of goods produced vs. the amount of money available. Lockdowns reduced goods while increasing the money supply. Anyone that wasn’t a paid economist was predicting this would occur in March of 2020, but Lowe leans on the same excuse as anyone else.

“No one could have predicted this.” In fact, the west has removed anyone competent enough to predict this from academic institutions, so the only place accurate predictions came from were private sector financial actors with minimal ties to academia and the government.

As a note, Lowe has previously stated that plans exist to begin cutting rates again in December 2023, and as we watch for hints now we see that this week he stated he expects to be slowing the rate of rate hikes in the near future. So we may be seeing Australia as the first western nation to attempt to “normalize” lending rates. Despite my macro thesis about liquidity being constrained, Australia may be able to actually pull off what Lowe is describing here. Unlike other western nations they have significant supplies of coal, oil, natural gas, and uranium, and haven’t succumbed to the same ideological crippling that Europe has where they shut down and minimized their own oil and gas production. As a result of that, energy prices in Australia have not increased anywhere near as much as they have in Europe and the US. As we move into a world where the Eastern trading sphere and BRICS have more power, we will see a move where the value of a currency on the global sphere will be directly dependent on how in demand their exports are.

Euro and Dollar Invoice Dominance

This is a bit of a tangent, but covers what I expect to be the most important economic change in the world this decade. I’m taking a bit of information from this study written for the IMF about invoicing dominance by currency, from July 2020.

the dollar share of invoicing (23%) still exceeds – by a sizeable margin – the share of exports destined for the US (10%).

Figure 4 also reveals that the euro’s share in global export invoicing is an impressive 46%. While this appears as a very large number, recall that a currency’s vehicle currency role can be gauged only by comparing its share in global invoicing to the share of global exports that involve the jurisdiction issuing the currency. This comparison reveals that the euro’s share in global export invoicing is not much larger than its share, 37%, of exports destined to EA countries.

Essentially this is the issue. 10% of world exports (2016) are heading to the US. But 23% of non-commodity exports are invoiced in US dollars and settled in that currency.

If we take data for that same year from the BEA:

You can see we had $2.7 trillion in imports and $2.2 trillion in exports. Essentially all trade coming into and also leaving the US was settled in US dollars. We essentially create demand for our own currency both when we buy things and when we sell things. The world that BRICS is currently trying to create is one where the only demand created for a currency is when that country exports a good. Beyond our trade imbalance, most countries in the world hold US dollars as a primary reserve currency beside their own because the US dollar ForEx (Foreign Exchange) markets are the most liquid and the easiest for other countries to use to acquire the currencies needed to facilitate trade.

In the quote above, we can see that the Euro and US Dollar in 2016 accounted for 69% (nice) of invoicing for all exports in 2016. When including the petro-dollar (below in orange), US dollar and Euro invoicing dominance averaged from 1999 to 2019 was 84%.

84%

This is the great Satan when viewed from an Eastern Lens. This is what allowed for rampant money printing within the west over the last 2 decades, and this is the applecart that is currently being overturned because the Eunuchs in charge of running the Liberal Economic Order did not realize that it is more valuable to them for Russia and China to continue to do commerce in our currencies than it is for them to protect whatever dirty little secret they were hiding in Ukraine. In the cold war, spies and subversives had the common decency to defect, or mysteriously commit suicide rather than overturn the economic applecart that allowed for our cultural dominance. The current crop of Eunuchs in charge leave much to be desired.

So when we speak of Australia moving forward and what they can afford to do, it depends on how much they want to help Europe and the US by continuing to invoice their own exports in those currencies, or being defensive of their own currency and forcing the exact same standards that Russia, India, and slowly China will be enforcing. Will Australia start invoicing more of their own exports in their own currency?

This process of de-dollarizing global trade cannot be reversed in the eastern sphere. As stated in February before the ukraine invasion;

Any threat we make to remove Russia from SWIFT is an empty one if we’re smart, but if we’re dumb it’s a major threat to the stability of Germany, England, Denmark, and others.

The sanctions kneecapped global demand for Euros, and Dollars at the exact time when we had just finished flooding the world with Euros and Dollars. Those Euros and Dollars have no other trajectory other than returning back to their domestic markets and pushing consumer and asset inflation significantly higher. The rest of the world has not figured this out just yet, but like an ICBM (Inter-Continental Ballistic Missile), as more time passes, more and more people will be able to estimate its landing zone.

3. EU Interest Rates and Conflict

The ECB has made it’s largest ever rate hike this week, moving the overnight lending rate up by 0.75%. They’re finally blinking awake slowly, it’s 11am, the party ended at least 7 hours ago and all of the guests have left except this guy. He’s in your living room just blinking awake on your couch as you and your roomates are mopping up the sticky kitchen floor and re-attaching your closet door that serves as a beer-pong table in a pinch. He thinks the party is still going and is trying to hang out, he’s reaching for the PS4 controller on the living room table while your passive aggressive roomate is hinting that they should leave because “we all have to go to work soon, you know.”

That is the ECB, extremely slow on the draw, and hasn’t quite realized that they should have dropped their classes on the drop date instead of ignorantly hanging on and pretending to still be planning to pass at the end of the semester. It’s November, they no-showed their mid-terms but think that if they start studying hard now, they can still pass their finals next month.

The truth is that Europe was not just dependent on Russia for oil and gas, they were also dependent on Russia as one of the largest non-EU sources of demand for the Euro. And as I stated in February;

Europe is extremely dependent on Russia for oil and gas imports, cutting Russia off from SWIFT would essentially push Europe into a dark age of recurring black-outs if not permanent ones

They are dealing with supply destruction of oil and gas, but soon they will also be forced to deal with demand destruction for their currency on an unprecedented level.

This is what demand destruction for a currency looks like. The chart against the Ruble is even worse, and this is not the bottom yet. The ECB is currently signaling that they expect for more 3/4 point rate hikes at their future meetings. And I believe them, but when official inflation is 9.1% while real inflation is likely in excess of 20%, they are nowhere near where they need to be at in their fiscal policy to actually begin to reverse this trend. All of those Euros will have to flood back to buying goods produced in Europe as they lose their function on the international stage. If the return on investment for holding Euro’s rather than spending them or investing in something else is not high enough to dampen spending, then those Euro’s will be spent, and prices will run significantly higher. But, as we covered in my post about Eurozone debt, there are several countries within Europe who’s sovereign finances are so out of whack that the governments could not function with interest rates high enough to actually fight inflation. It’s why the only possible outcome I can see is for countries to break from the Eurozone.

Greek-Turkey Conflict

As discussed at the beginning of the week, a dispute over islands and sea territory in the Aegean is beginning to flare up again between Greece and Turkey. They have had minor disputes over the past 5 decades around Cyprus and several outlying islands in the Aegean sea, some which included minor armed conflict.

Erdogan and Turkey have been moving away from the EU lately and in favor of Russia and the BRICS sphere, and it’s possible that if things become extremely disarrayed that Turkey or Greece may try to dance on the line of pseudo-conflict in the near future.

Quite a few conflicts these days tend to brew around the same thing, Sovereign rights in the ocean. In the 1900’s, as exploitation of ocean resources began to become more widespread and industrialized; and as the preservation of resources began to become a concern for countries; they wanted a uniform way to identify specific areas of the ocean that belonged to them and nobody else. So, in the late 1900’s (lol, don’t get mad), the UN came together and signed a series of treaties, the latest of which came into effect in 1994 that established what is called an EEZ (Exclusive Economic Zone). An EEZ is essentially a 200 nautical mile area, it extends from a countries shoreline outwards perpendicular to the shore, and can extend up to 350 nautical miles if a continental shelf is present of shallow water (like the US has in part of the atlantic ocean).

The legal jurisdiction of a country only extends 12-24 miles from shore. So most of the EEZ does not fall under any countries legal jurisdiction. So this UN treaty says that you have exclusive rights over this 200 nautical mile zone, but enforcing that can only really happen on the world stage in the UN, and typically would be done through international sanctions. But as we’ve seen so far, countries that want to flout UN laws in international waters have been able to do so with impunity. This is why most of China’s maritime neighbors do not like them. The UN has mostly failed to enforce this treaty on the international stage. This is why China is building islands in the South China Sea, and then claiming to own these islands, because it extends China’s EEZ in a 200 mile radius around the island.

Similarly, Greece and Turkey have been feuding over who owns which islands in the Aegean and who has claim to what resources in the Aegean. Depending on how distracted western nations that were previously the hedgemons get, and how restricted their national budgets become; Turkey may feel emboldened to try some sneaky moves within international waters. At which point, Greece can either take it as an act of war, or Greece can do what other western allies have done when their EEZ has been encroached on, which is ask the west for help and await a strongly worded letter to be sent by the UN.

4. Canadian Interest Rates

The bank of Canada hiked rates by 0.75% and the overnight lending rate is now 3.25%.

My view of Canada is similar to my view of Australia. They produce significantly more energy and food than they consume, and if they also were to attempt to enforce more US demand for Canadian dollars on those exports, they could similarly ride out this storm without much pain. Their government budget deficit is not nearly as egregious as the US, but I think they will likely stick with the western sphere as a vassal state rather than trying to enforce any fiscal autonomy of their own, so I suspect that they will also be dragged down by this conflict unless a significant change occurs in their populations voting patterns so as to elect a populist government.

5. Crypto Macro

Price Action

If you are new to looking at my charts, please refer to my post on Basic Technical Chart Reading to understand how and why I identify certain zones as well as some of the basic information on the chart.

The week started out bearish, and that trend continued until the ECB’s interest rate decision at which point Bitcoin (and the crypto sector as a whole) went on a rally and we saw BTC push through 2 resistance zones. I’m not entirely sure why the market reacted to the ECB’s rate decision like that, or if that was even the event that triggered the move. The run in crypto began around 11:30pm CST Thursday night, while the ECB rate decision occurred at 6am CST Friday morning. I wouldn’t expect that move to signal a major reversal in price sentiment and expect that the same macro persists of prices being flat or down. I would expect BTC to retreat back below the $20,791 support zone during the coming week, but it’s plausible that it might catch another bid on the US CPI number next week. Next weeks’ CPI will be low as the sale of the US governments Strategic Petroleum Reserve will begin to show its impact on the coming CPI figure. The markets will interpret a lower CPI as a chance that the Federal Reserve will pivot soon as they expect the Fed to slow/stop tightening if inflation returns to average 2%. So any sign of CPI coming down will be viewed as positive from the markets. So it’s plausible that BTC could stay in this price range for the next week.

A Lesson Learned

So, as I stated in the beginning of this post; this post is coming late because I spent most of last night poring over transactions as I was the victim of an exploit on an NFT platform. I worked with some of the devs and the exploit has been fixed, but it was a rather long night (I went to bed at 9am this morning), but I will make a longer post outlining what happened, and how the exploit could have been avoided.

The short of it is this. Myself and 4 friends agreed around 1:30 am CST Friday night (Saturday morning) to pool assets worth ~$20k (68,345 ICX) and sell in a bulk order to meet an offer on the NFT marketplace. The marketplace had been tricked by a malicious set of transactions. To be fair, we had received these assets for free in an airdrop.

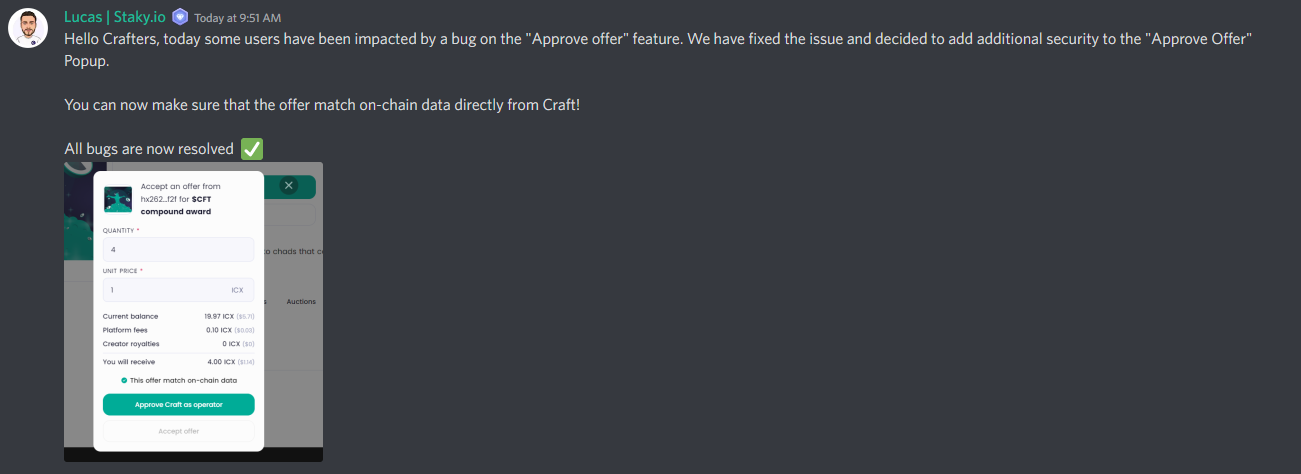

Essentially the scammer sends a transaction to the backend code for an escrow contract that would normally hold the funds if someone makes an offer on an NFT. They sent a transaction to reserve the funds, but then cancelled it after the backend had received the transaction but before the blockchain had finalized the transaction. He withdrew 90% of the funds in the red transaction above after the offer had been reverted on chain. Once the backend had been tricked into thinking that the full amount was in escrow, it displays the offer on the NFT site so as to look like a legitimate offer. When a user attempts to accept the offer, the transaction keeps failing, but the malicious wallet sets up an automatic transaction to go through in its place to send a new amount to the escrow wallet for 1/10th of the actual offer price. I’m still unclear about how the second transaction was pushed through. But it doesn’t matter. After a long night and working with the devs we put in place some traps for the scam wallet, I went to bed after the code had been updated.

The NFT platform now initiates a “read” function to confirm the transaction matches the amounts the back-end thinks are being sent. If it does not match on-chain data, the user is given a warning and any attempt to sign the transaction will be auto-failed. This makes the contract slightly more expensive in gas fees, because a “read” operation in the coding language of this blockchain requires some gas to perform.

This is the kind of thing that only time can reveal on a blockchain. Platforms, dApps, and code cannot be perfected with just a smart contract audit. The longer it has been in existence, the more of these small adjustments can be made to the underlying code and function to improve security and efficiency. This is the main problem with launching a new blockchain as compared to building on an existing one. You can copy past code on an existing blockchain and you gain all of the years of experience that dApp has up to that point. All of the minor security fixes, bug patches, and quality of life changes to remove exploits.

This is one of the biggest arguments for Ethereum. It’s competition simply lacks the deployment time in a real financial environment that all of the code on Ethereum has. ICX is the main Java chain, and as such, all of these types of lessons have to be learned in real time all for this programming language, as dApps cannot be copied over from ETH, they have to be rewritten for Java which has its own constraints and benefits compared to Solidity or other coding languages. When someone tells you about a new chain that someone is starting and why it’s better than Ethereum, or any other chain that already exists, please remember that the new chain has 0 years of real world testing in a financial environment. ETH is going on 5 years now of having dApp deployment with real money. ICX is at almost 2 years of dApp deployment now. A new chain starting (such as Aptos) will be at 0 when it launches. Time in an IRL deployment environment cannot be bought, it can only accumulate with the slow grind of the second hand on the clock. VC’s trying to launch new chains do not yet understand this. Either they make it fully EVM-compatible and ETH dapps can be copied, but then, why leave Ethereum? Or they don’t make it fully EVM compatible, and they’re significantly behind in security testing, and the big money asks the same question, why leave Ethereum?

I’m not an ETH maxi. But I am an ETH realist. In my quarterly crypto macro posts (I will have a new one this month, lots of updates!), I make the case for legitimate use cases in blockchain that I expect to emerge. But just like ETH, they also need time IRL in a deployment environment. Rome was not built in a day.

Grid+ Wallet

How can you avoid a malicious transaction when the site you are interacting with has read the code wrong?

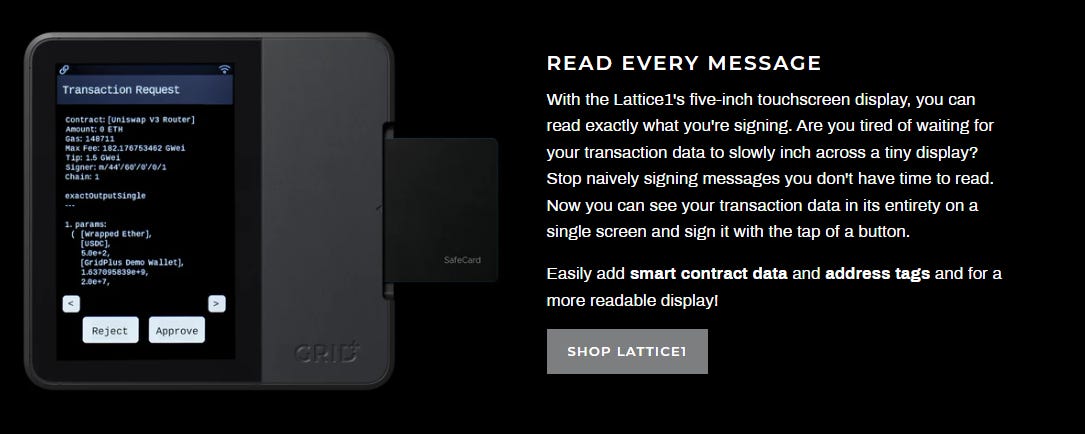

You have to look at the blockchain transaction itself. Unfortunately, the group chose a member to handle our pooled assets who was trusted for his honesty, but was not exactly savvy enough to have thought to inspect the actual transaction itself before signing it. This means either reading the transaction on chain before signing for it, or using a hardware device like the Grid+ wallet.

The above link is an affiliate link, they pay me an 8% commission if you make a purchase after clicking the link. If you like it, you don’t have to use my affiliate link. It’s not that big a deal. The Grid+ wallet is currently compatible with all blockchains that are metamask compatible, and the big draw here is that anytime you initiate a transaction the entire transaction is displayed on the touch screen. You can see how much of a token you are sending and the address to compare against what you think you are doing. The exploit that occurred last night could have been more easily avoided if the person signing the transaction had inspected the on-chain transaction and not the one displayed by the dApp website. A hardware wallet like the Grid+ wallet makes reading this information easier, and if you are moving large amounts of money in a single transaction, double checking the on chain data before signing is key.

The lesson I learned from this exploit is two-fold. One, I’ve gotten lazy about signing transactions and should be more careful to double check them. Two, if something seems too good to be true, I can and should sleep on it and see how I feel in the morning. When it comes to your money, no decision is so urgent that it can’t be slept on, and if you feel as if you can’t wait to make the decision, that is often a sign that you are being manipulated in some way or another. Were the NFT’s worth $20k? Truthfully we don’t know, the only legit sales put them at combined ~$13k. We probably should have taken pause. And lastly, when transacting as a group, its not enough to trust someone’s character with your money, you must also judge their competence. Nothing against the guy who signed the transaction, I may well have made the same mistake. But moving forward, I won’t, and I would do well not to trust anyone who does not feel the same way.

6. Conclusion

Dollar/Euro invoicing dominance on the global stage is collapsing. A new world order is emerging (I laughed as I typed these words). Western economics is more about social control, while Eastern economics are (for now) just statistical reporting as social control is effected through other means.

The macro is still for markets to be flat/down, and we can expect more panic to emerge in Europe over the coming months. I expect to see turmoil begin to emerge as interest rates on European 10 year bonds begin pushing upwards. Most of this pressure will ironically be felt in Germany, because as we stated previously, Proceeds from German debt maturing will be used to buy up Greek, Spanish, Portuguese and Italian debt to avoid those treasuries from running up sharply as they are the most distressed markets. It’s QT for Germany, and continued Easing for the rest of Europe.

How and when that distress emerges will be anyone’s guess. Germany has an extremely solvent economy and can likely bear a significant additional burden from its irresponsible Mediterranean debt anchors. But this will be a cold winter for Germany, and no matter how much preparation the grasshopper put in for this, the octopus is going to eat all of his acorns.

Is any of this getting through to you?

If you've not read it, you might enjoy the new book The Lords of Easy Money about the Fed, the beginning of QE and the lone dissenter who was vilified for it (the president of the Kansas City Fed). I've just started but it's good so far.

Looking forward to the crypto macro post on emerging blockchain use cases! Particularly interested in ecommerce ones (if any).

Have to recommend Singapore for its sheer economic and political stability. Extremely safe with low crime, relatively low taxes, diversified food and energy supply (when Malaysia stopped supplying chickens we simply replaced them with Thailand and now MY is crying for our business). Also no left/right wing drama, it was never even a concept here. Singapore really is one of the best places to build wealth/a career if you don't mind the tropical climate.