6/19/2023 - The Black Cube of Saturn

6/19/2023 - The Black Cube of Saturn

Do large entities plan to consume the crypto markets?

If you are a new reader, there are helpful links at the bottom of this post.

All times in this update are in US Central time (UTC-6 clock).

Song of the Week - Offspring - Why Don’t you get a Job

Table of Contents

Powell Testifies Before the US Senate

Economic Calendar

BOJ Minutes

Swiss Interest Rates

British Interest Rates

Crypto Macro

Price Action

Black Rock ETF

Conclusion

Internal References

1. Powell Testifies Before the US Senate

The Head of the US Federal Reserve always testifies before the US Legislature twice a year, once before Congress (earlier this year) and this week, Powell will be testifying before the Senate Banking Committee.

For the same reason that Gensler’s testimony was mostly tedious, this will also be similarly tedious.

The Senate Committee is mostly idiots, just like the congressional financial services committee is also idiots. You can expect maybe some decent questions from Tim Scott, but we’ll get some genuinely atrocious content from Elizabeth Warren, and hopefully, John Fetterman relinquishes his time to another member, otherwise, the last question asked will be incoherent as he is the most junior member of the committee.

This is mostly a non-event, but if you decide to torture yourself to watch the public hearings they will be aired on Thursday starting at 9 am CST and going on for likely 5 or 6 hours.

The questions of note mainly dovetail from last week’s FOMC meeting where the Fed decided to leave rates where they were at, as we expected. Currently, there is a slow-moving banking crisis occurring in the US and if any government entities should be aware of and asking about this banking crisis, you’d think it would be the Senate Banking Committee. But most of the members won’t live up to their name.

So, what’s important during this testimony?

Questions about if this is a pause of rate hikes or the end of rate hikes.

Questions about the banking sector's solvency, and if any other potentially distressed banks are being monitored by the Federal Reserve.

Questions about duration risk and interest rate risk collapsing the commercial real estate market.

Questions about the US banking sector’s exposure as a whole to distressed industries.

Some dolt will likely ask about inflation and give Powell a layup, but it may still be of use to hear what he says about the Fed’s expectation for inflation in the future. All that matters is for the CPI (4.00%) to stay below the Federal Funds Rate (5.08%).

As you can see the major concerns looking forward are purely about the US banking sector and its exposure to assets and industries that can’t keep up with an interest rate environment that is not 0%. The big danger zone right now is commercial real estate, I’ll have a more expansive post on that issue coming soon, but there are certainly other sectors the banks have exposure to that may require a significant revaluation of assets that banks have already lent money for.

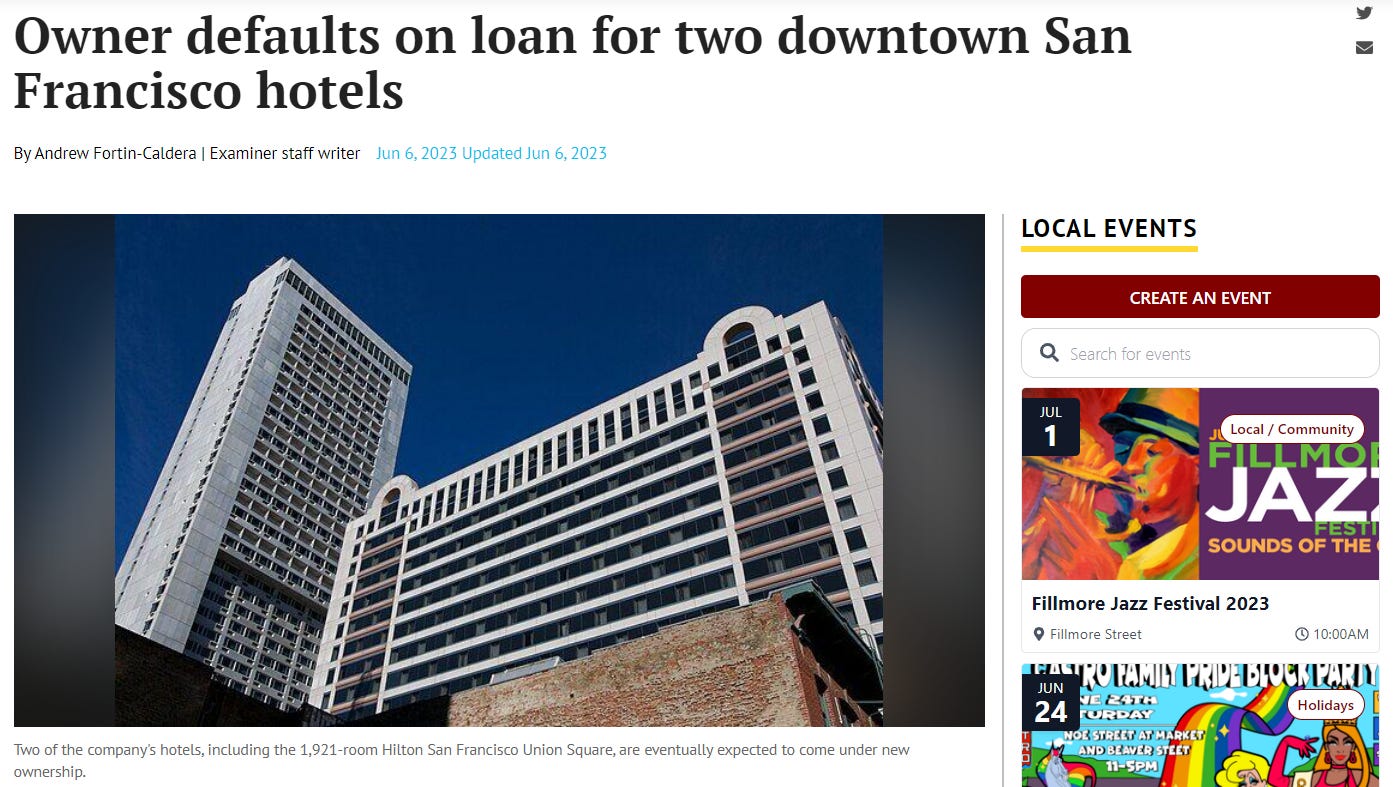

Essentially, what sorts of problems does it cause for the bank when a large asset like this with significant maintenance and operating costs is turned over to a bank that has no staff or expertise to maintain such a property? The bank lent X amount of dollars for the construction back in a 0% interest rate environment. But now the hotel has dwindling revenues, and money is now worth 5% at the bottom of the lending curve. Can the bank recoup the money that was dumped into this building? Can the bank even keep the facility open and maintained? Some people think that these sorts of commercial defaults will lead to a cascade of sales by banks that can’t afford to hold on to these assets and will dump them at any price just to keep the operational expenses off of the bank’s budget. And while banks would ideally like to sell these assets, the question is who will even be there to buy them? It might be that something especially toxic like this (hotels in SF) has very limited or no buyers unless the bank is offering a steep discount (60% below the original valuation, or worse).

What happens to the banking sector when a bank is forced to take on assets like these where they lent $725m with these 2 hotels as collateral? The hotels themselves have been renovated many times with nearly $100m spent on renovation in the last decade. How much is the property worth? The bank might have presumed they were worth over $700m when the loan was made, but how much is it actually worth? What happens if the bank has to take a $300m hit and sell these on a firesale just to get rid of the maintenance expense? What happens if this bank has several other loans for commercial real estate? SVB collapsed over a $2b mistake with treasury allocations. Who’s to say a bank focused on commercial real estate couldn’t find itself with a similar hole on its balance sheet over the next 2 years?

We’ll get into this more in its own (free) post, but these are the questions of most import that could be asked during the Senate committee this week. If you do decide to watch it, consider how many horrid and time-wasting questions will get asked instead. Our government is a joke.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.