7/3/2023 - Crypto Valuations

7/3/2023 - Crypto Valuations

Prime Trust gets in the forever box

If you are a new reader, there are helpful links at the bottom of this post.

All times in this update are in US Central time (UTC-6 clock).

Song of the Week - Lit - My Own Worst Enemy

Because Sometimes, Crypto Execs are their own worst enemy.

Table of Contents

Valuing Crypto

Economic Calendar

Australian Interest Rates

US FOMC Minutes

US Employment

Crypto Macro

Price Action

Prime Trust

xCall Incentivized Testnet

Conclusion

Internal References

1. Valuing Crypto

Depending on what part of the cycle we are in you have probably had the experience of someone or multiple people telling you about a new project, new NFTs, or new token that they think is the next big thing and why you should value it.

Personally, when I have those conversations I usually presume what I am hearing about is valueless, harsh I know. But the real truth from a tokenomic standpoint is this; very few tokens and projects actually generate more revenue than they emit through inflation.

This is the harsh truth of crypto.

In traditional business, the simplest way to value any potential acquisition is by comparing how much profit it makes, and how much it costs to operate. There is little reason why we can’t do the same with crypto, what we see in the crypto world is kind of bleak.

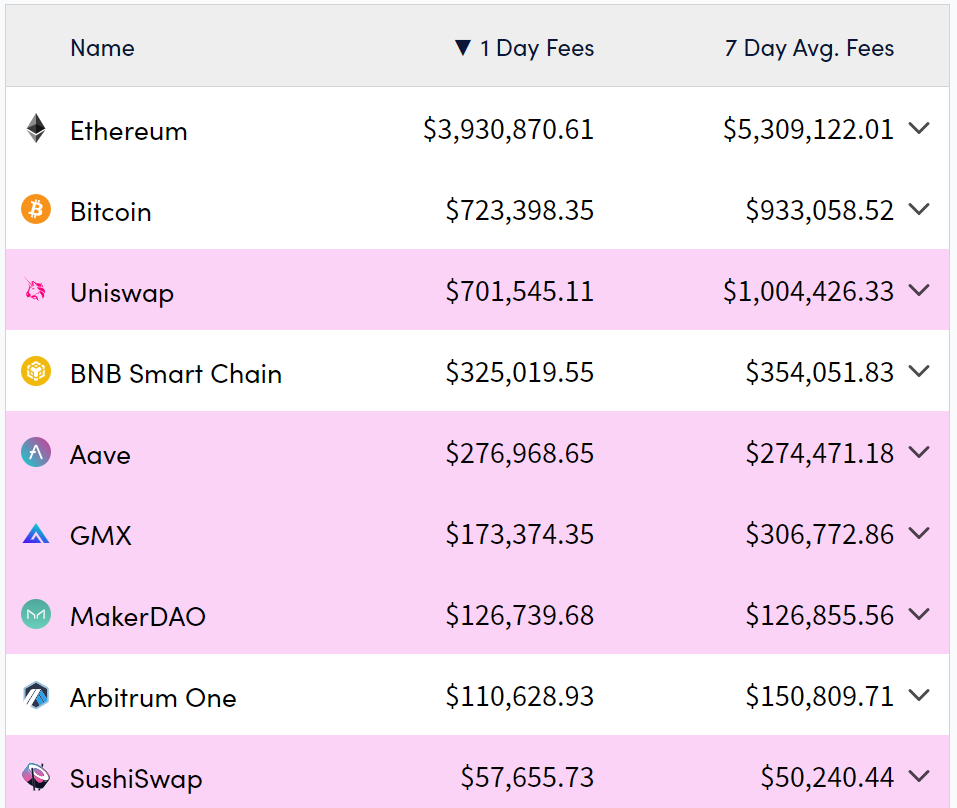

Let’s look at cryptofees.info for a live peek at how profitable the most profitable crypto projects are today (Monday 7/3).

We can start our assessment with ETH, which is one of the bright spots in crypto. We’ve already discussed tokenomics before and how ETH could become deflationary, but now we’re going to run the numbers and compare it to other protocols in crypto as an example.

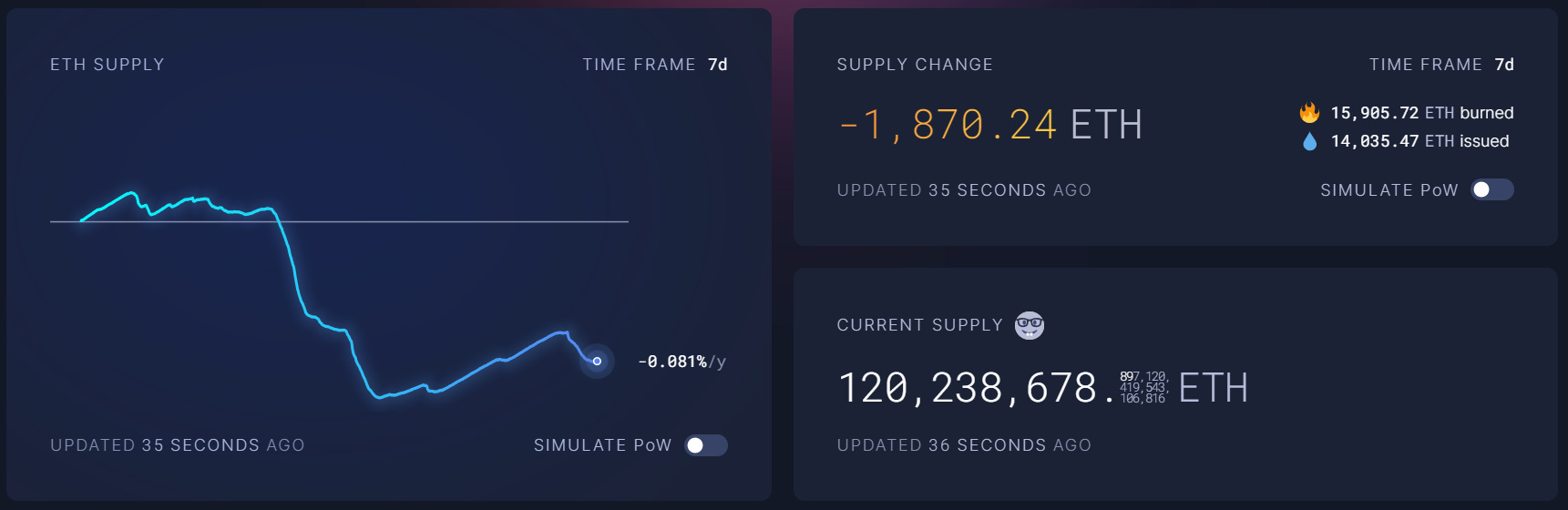

Depending on how much ETH is used, there are times when more ETH is burned from gas than how much ETH is minted and distributed to stakers. Which puts ETH in an interesting position.

If ETH is being used to the tune of $5.3m a week in terms of fees, and the supply of ETH is decreasing by 1,870.24 ETH a week (~$3.6m at today’s price). Then there is an implied accumulation of value within Ethereum as a whole of $8.9m a week. Eth is a horse, and it’s running, this is a no-brainer. And it’s been a no-brainer. Of course, the math I’ve just done for ETH is highly simplified. However, ETH has been deflationary since the merger (as you can see below).

It’s very simple, you have a project that is generating money from genuine demand, and its supply is decreasing faster than new shares are issued. It’s the same math you might do if you buy a stock because you know the company is planning to do stock buybacks, as the supply decreases you get to ride the valuation up for easy money.

Where this picture gets bleak is if you look anywhere else. You may notice Bitcoin is number 2 in the first chart with a 7-day fee generation of $933k, and we’ll just round it up to $1m for ease of math here. Unfortunately, about 900 bitcoin are mined a day, and at today’s price that’s $27m of issuance. From a simple business perspective, Bitcoin is not making money. Sure, Bitcoin issuance will be halved next spring and we’ll have $13.5m of Bitcoin being issued, but if fee generation is stagnant it still won’t matter from a valuation standpoint. Sure, there is considerable value in the store of value function of bitcoin being truly decentralized and that value statement does not come from usage but from the knowledge that it can be held and never taken from you unless you make a mistake.

Old school users may value this of bitcoin, but from an institutional standpoint, the only token they can look at and understand is ETH. For the simple reason that it’s one of the only cryptocurrencies that earn more fees than its token issuance. There are other projects in that first list that also make money and make sense to outside institutions.

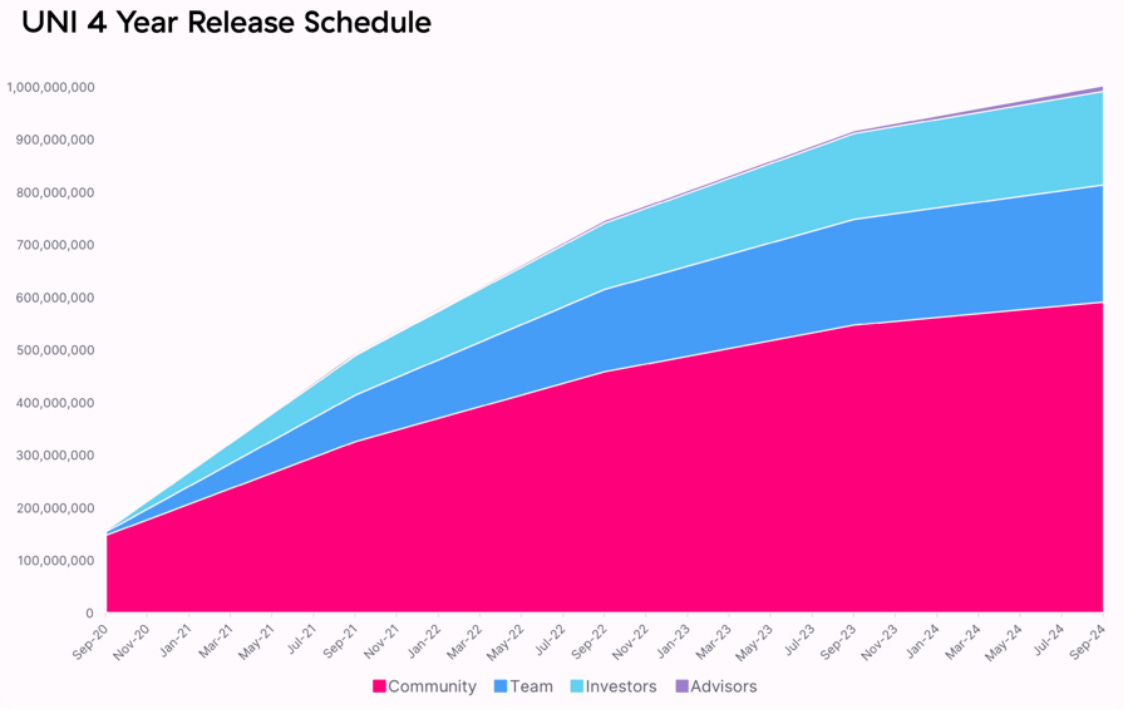

For instance, the DeFi protocol UNI makes $1m a week in fees, meanwhile, UNI’s release schedule has been slow and steady and it’s nearing the end of its 4-year initial token release period that started in September 2020.

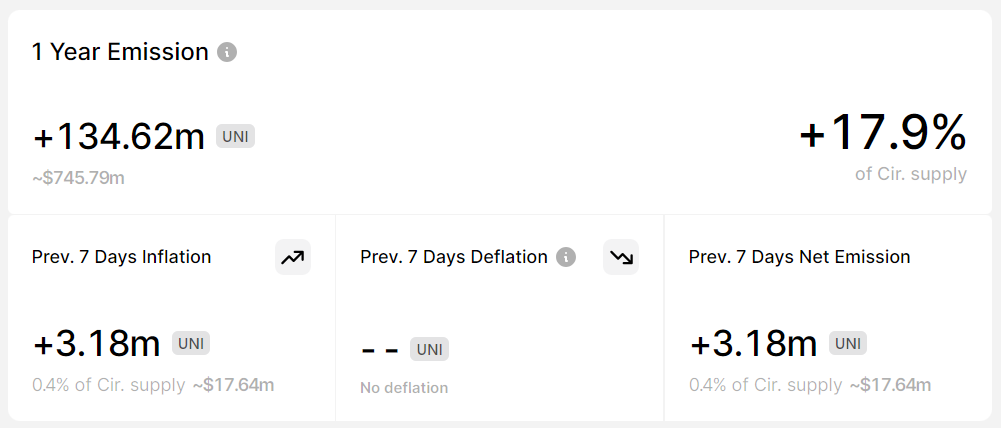

Unfortunately, UNI’s token unlocks at a rate of ~3.18m per week, which amounts to ~$15m per week. Currently, UNI’s token unlocks also outstrips its daily fee usage.

However, UNI is 88% unlocked, and once it reaches the end of its 4-year initial release schedule, UNI will switch to a 2% inflation per year. At current prices, that would put its mature inflation at ~$2m a week, so realistically, it only has to double its fees within 1 year. Considering we are looking at protocol fees during a bear market, it’s not very tough to expect UNI to be profitable during bull markets. Other Protocols like AAVE and GMX can also be analyzed in this manner, and we come to what is likely the institutional conclusion about Crypto.

ETH is the clear winner, and a few ETH DeFi L2 tokens also have clear value. Scrolling down we see some clear issues with some of the alt-coins.

The fees generates by some of the alt-coins being tracked are horrid. $30k a week for Solana and Polygon. Cardano and Fantom less than $10k a week.

This is the transition of value propositions we discussed last year that the ETH-killers would invoke. They will have trouble justifying their existence and attracting dApps and users with the changes to ETH tokenomics and gas fees. Whether they succeed or not is directly dependent on if they can form a niche and set themselves apart as the top choice for protocols of that type. We’ve discussed how Polygon is trying to make itself the hub for blockchain gaming, what will these other chains do?

I don’t know. But if you are struggling to understand how to value crypto, this is the simplest method to do so and to understand why ETH is the horse to make sure your wagon is hitched to. As sexy as alt-coins can be, your primary allocation should be to ETH and BTC. I have always leaned more toward ETH, and the above math supports that as well. Alt-coins are for a small portion of your crypto portfolio, I wouldn’t recommend more than 25% allocation to Alts for the simple reason that in general, ETH will outperform them except for a few short occasions. Unless you are an active trader, you are taking on significant risk with very small windows for upside. Your investments in alts should be because you believe in and use that protocol, and it should be small.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.