Beginners Guide to DeFi

The Basics of DeFi and a Giveaway

This guide is for someone that has a basic understanding of crypto and has a decent amount of crypto assets and they want to deploy some of those assets for additional income.

In order to do the things outlined in this guide, you need to

own crypto

have taken custody of crypto in a DeFi compatible wallet

Know how to sign transactions and are comfortable sending assets from one wallet to another or from one address to another

A Definition list for the abbreviations, words, and terms that I use.

This guide exists to explain to you the basics of how DeFi works, and how to use a mature DeFi protocol. The things explained to you here do not apply to new protocols due to the mechanics of tokenomic issuances in a new protocol where supply is inflating rapidly and demand is also fluctuating rapidly. I will make a later post that is almost exclusively discussing the tokenomics of new platforms and how to exploit them. It is a much higher risk strategy though and is likely only for a handful of you. For those of you wishing to simply see the good returns that crypto offers without diving into the degenerate side of the pool, this is the guide for you.

This post is one that I would say is for amateurs. If you already know everything in this post, consider it as a good resource to share with someone else in lieu of explaining many of the complicated mechanics behind most DeFi solutions.

This post is too long for email and will get cut off, please find the entire post on the substack website.

This post contains a giveaway at the bottom. Please read section 6 for more info.

As a final reminder, the paywall is up. There will only be 3-4 free posts a month moving forward, and one other free post this month after this one. If you have not subscribed and don’t want to lose access, remember to subscribe. The free posts will be focused on beginner and entry level content. All crypto guides beyond this will be behind the paywall.

Also, I will cover this in section 4, but if you have less than 6 figures of USD value in ETH, you will want to engage with DeFi on alternate Layer 1 Smart contract platforms due to gas fees on ETH. This means that you will want to have a small portion of your investment in one of the chains I’ll cover in Section 4.

Table of Contents

What is DeFi

Types of DeFi

Basic Common Sense

Getting Started

Conclusion

Giveaway

1. What is DeFi

DeFi stands for Decentralized Finance. It is a catch all term for any financial instrument who’s rules and functions exist almost purely in code on the blockchain itself and can be interacted with through a pseudonymous non-custodial crypto wallet.

DeFi turns the entire institution of a bank into code. It replaces every single physical building, vault, server room, the army of employees, armored trucks, underwriters, credit checks, loan officers, market makers, insurers, etc; they are all replaced by networks of computers running cryptographic proofs over immutable code. So it stands to reason that DeFi can fairly easily undercut the banks and offer cheaper services, at a fraction of the price; but its also evident that if you can get a piece of the action that there is a significant amount of profit to be made as well.

DeFi is essentially code. Where and how is this code programmed? Well, blockchain is programmable. More can be done by the computing power supporting the network than simply tracking where assets have been sent like the bank ledger example from Section 1 of this post. The code is also programmable and programs can be stored and then uploaded to the blockchain to a contract address. A contract address is similar to a wallet address except that it is purely controlled by the code and the code cannot be changed without publicly broadcasting the change. As defined by IBM:

Smart contracts are simply programs stored on a blockchain that run when predetermined conditions are met. They typically are used to automate the execution of an agreement so that all participants can be immediately certain of the outcome, without any intermediary’s involvement or time loss. They can also automate a workflow, triggering the next action when conditions are met.

So this means that you can set up anything that you can imagine in code. You can turn a contract entirely into code. At my day-job, I had some experience with a company providing BaaS (Blockchain as a Service) to oil and gas companies. What they did is they turned a procurement contract completely into a smart contract on a private blockchain. The contract had established delivery points, delivery volume, and price for crude oil. Once the contract was agreed upon by both parties, it was entered into code at which point it could no longer be changed. When the conditions of the contract were met (a sensor confirms a specific volume of crude oil passing a delivery point), an invoice is automatically generated and a payment is automatically debited. Payments in this sphere can normally take 45 days and require quite a few administrative hours to confirm, approve, document, and execute. With BaaS payments can complete in less than a week with less than 10 minutes of admin time, and can be audited in seconds instead of weeks.

Now lets pivot to my own personal experience, with a dApp that is centered around a smart contract for controlling lending and borrowing rates of stable coins and other assets.

There was a morning a few months ago (4am my time), that I needed ~$2,000 to mint a handful of NFTs. I didn’t want to use any of my assets, as they were all appreciating. So I supplied them as collateral to a lending dApp, took a loan in roughly 4 seconds that I was paying ~45% interest on, and then flipped the NFTs in about 10 days for ~$5,000. My loan had risen to the point where I had to pay ~$40 in interest, and I pocketed the difference after paying my collateral.

In that same period of time a bank would still be reviewing my loan application. They also would have never accepted crypto-currency as collateral for the loan. This is just a practical example of what can be done. Maybe you don’t want to take a loan, maybe instead you would like to collect the 45% interest from me. You can simply provide assets to the smart contract platform. It collects the interest for you, and not once a month. It instead accrues interest every time a block is solved, so you can make a loan for 15 seconds if you want and collect interest for those 15 seconds. Blockchain solutions no longer have the same limitations that human actors do. The code is the law. The code can collect compounding interest as frequently as every 2 seconds if it is written to do so. Or every 5 seconds, or every 10 seconds.

Many DeFi platforms are governed by the users themselves who can vote to change things within the code. Does your mortgage company let you vote on what forms of collateral they will accept for a home loan? No. And certainly there is always the risk of tyranny of the majority voting for something you don’t want, but the beauty of DeFi, is that you can always leave the platform if the users vote for something stupid. You can withdraw funds in a matter of seconds at your own discretion. Your bank does not even give you this level of freedom, and your deposits pay their salaries.

You’d think they’d show some gratitude.

2. Types of DeFi

There are more types of DeFi in existence now than I am currently aware of, and we are still extremely early into this sphere. More types of DeFi will be invented that no one has ever thought of yet. I will provide some examples of common types of DeFi that exist and how you can use them to generate income.

Decentralized Exchanges

You already know what a DEx is, here’s how it works. If you want to buy or sell something in life, you have to wait for someone who wants to sell it to you, or buy it from you, and at a price you both agree on. To get around this delay, a practice called market making was created. Market Making is when an entity or individual quotes both sides of the markets to buyers and sellers and provides liquidity for people wanting to sell or buy right away.

In crypto, automated market makers provide both sides of a trading pair, below is a screenshot from ($BOO) SpookySwap, a DEx on FTM (Fantom) Where Decentralized trading can occur.

For someone to trade wETH for FTM, they would be selling wETH into the pool for FTM-wETH and pulling FTM out. So if someone wanted to act as a market maker by providing liquidity for the FTM-wETH pool, they would need to provide both FTM and wETH to the pool in equal dollar amounts at the time they contributed it.

The exchange rate of the assets in the pool is algorithmically determined by the balance of assets in the pool, so as someone buys FTM with wETH, they are changing the balance of assets in the pool, and as such are affecting the exchange rate by making FTM more expensive against wETH.

Trading fees are charged to people who trade, the industry average is 0.3% right now, and typically at least half of that goes to the market makers. But wait, if you look at the image above, the APR’s are all between 37%-82%, where is that APR for market makers coming from?

When a new DEx launches, they need some way to incentivize people to supply liquidity, because a DEx with low liquidity is unable to maintain accurate prices as even a small purchase can significantly affect the price. So DExes will create a token emission schedule for their governance token where large amounts of it are awarded to market makers for locking liquidity into a pool. Market makers can either keep this token, or sell it. Below is the emission schedule for DIKO which is the governance token for a DEx on STX.

You can see that in the amount of tokens emitted decreases on a daily basis until the emissions reach 2% inflation on year 5. These emissions are used as incentives for liquidity providers. So if you want to place assets into liquidity pools on a DEx, you can earn a fairly decent return. However, I will warn you, that as a beginner, you want to avoid the first 6 months or so of entering a liquidity pool unless you understand some of the more advanced mechanics of IL (impermanent loss) which I will explain in the advanced guide to DeFi in a few weeks.

After about 6 months in a stable/growing DEx, impermanent loss becomes much simpler to manage. I am directly copying an Impermanent Loss example in the text below from a great substack based on DeFi. I will be gifting a 1 year subscription to the “DeFi Education” substack in the comments to one of my paid subscribers on 1/28/2020.

Impermanent Loss Example

You have 5 ETH and 15,000 DAI (total value = $30,000)

You LP your $30,000 in the ETH/DAI pool

ETH price increases by 30% to $3,900 and you remove your LP

You would now have 4.39 ETH at a price of $3,900 ($17,121) and 17,103 in DAI (total value = $34,224)

If you had held your 5 ETH and 15,000 DAI instead of LPing, you would have had 5 ETH at $3,900 ($19,500) and 15,000 DAI (total value $34,500)

Your impermanent loss is $34,500 - $34,224 = $276

Note that at both the time of purchase and time of withdrawal, the quantity of ETH * DAI = 75,000 (x * y = k)

Simply put, the difference between holding the asset pair in your wallet and the value of your LP is known as divergence loss or impermanent loss. You can use impermanent loss calculators to estimate your IL in various scenarios, estimate you trading fees earned and add in the value of any liquidity mining rewards you expect to earn to determine if LPing will be profitable for you.

End of excerpt from DeFi education.

In the first 6 months, due to the amount of liquidity that can be added to a pool it is very possible to 6x-10x the dollar value of what you put in to the LP if you time an entry and exit properly. It is also just as possible to cut the dollar value of your deposits in half or more in a short period of time if you enter the LP at the wrong time during the first few months of the launch of the DEx. As I said, I will explain this later in an advanced guide. For now, if considering supplying assets to a DEx, you can avoid IL entirely by supplying to a stablecoin pair where both assets have a fixed price they attempt to maintain. The below example is USDC-Tether. They are both fixed to as close to $1 exchange rate as can be, however you will get lower rewards on lower risk pairs, so here you can only 18% APR.

Another strategy for minimizing risk is by pairing two tokens that have similarly bullish outlooks and where there is not an expectation of significant emissions in the near future. Below you can see that the BTC-ETH pool also has fairly low APR because they typically trade in a relatively stable range with each other (last year being the exception), and this DEx is on FTM where there is less use for BTC and ETH.

And finally there are the higher risk pools. They are either high risk because they have very low levels of liquidity which can ruin your dollar value if not careful. Or because they are new pools with large incentives, or because of the emission schedule of the reward token means that you will want a shorter term entry strategy.

You can see the pools above have very low levels of liquidity and can be fairly dangerous places to park money if you don’t understand what you’re doing. The mature and less risky pools in this space typically see returns between 28%-60% when you are on a mature exchange that is at least 6 months old. If you don’t know why the APR is high (over 100%), my general advice is to not supply liquidity. You need to know why and what risk you are accepting before putting your money in.

Decentralized Lending

This is a much simpler example than a DEx. Decentralized lending platforms work in a fairly simple manner. Below, I will be using examples from ($OMM) Open Money Market, which is a relatively new lending platform on $ICX (Icon). The platform has fairly simple rules. You can deposit any of the assets below, and borrow any of the assets below.

You are paid the supply rate if you lend, and you are charged the borrow rate if you borrow. The borrow rate is determined algorithmically based on the percentage of the total asset that is available to borrow and the total amount that is currently borrowed. Below screenshot is taken from the whitepaper.

There is essentially an Optimal utilization rate the platform is targeting. If utilization of an asset gets too high, the platform offers a higher interest rate to entice people to bring that asset to the platform. If the utilization rate gets too low, the interest rate drops in order to incentivize people to borrow from the platform. I’ve seen rates on this platform as high as over 100% and as low as under 1%. The rates are variable, so if you borrow, understand that the rates can change on you based on the behavior of others. The same is true if you lend, and is something you should be wary of.

Most lending platforms have collateral ratios they want to maintain. If your total debt hits 100% of the value of your collateral, your position will be liquidated and your collateral automatically sold to repay your debt. So one should be mindful if supplying or borrowing a volatile asset as its price can change significantly and can potentially cause you to default on your own loan.

This dApp is also incentivized as well. The OMM token is paid out to borrowers, and lenders, which they can claim and sell, or keep and use for governance. Even after paying interest rates for borrowing, you can still earn money by borrowing money. Are you starting to sense a trend here? On top of receiving interest every 4 seconds, you are also receiving a governance token that has a value and can be sold. Most every dApp that launches has this model. As a new person to DeFi, your best bet is just selling these tokens initially. The governance token usually leeches value slowly because most people are just selling the token. Game theory says you should sell too. If the governance of the protocol becomes valuable, or if the governance token itself has an income proposition, then you could consider holding it… maybe. But as a new person to DeFi, your focus should be selling to gain more of the base L1 token instead. Once you have a feel for token emissions, you can be more choosy about not selling.

Decentralized NFT exchanges

This is a new category that I am adding due to the recent launch of ($LOOKS) the LooksRare platform on Ethereum. NFT exchanges typically charge transaction fees and the older exchanges just had those fees go to the developers/creators of the platform. This is web2.0 thinking, and is outdated and antiquated. This is how OpenSea currently operates, and they are trying to sell their ownership to Citi Bank, its doomed to fail and is why and how LooksRare launched. LooksRare essentially copied the code for OpenSea, gave out an airdrop of $LOOKS to anyone that had used OpenSea, and then will share a large portion of the transaction fees with anyone that stakes the LOOKS token on their website. LOOKS will function as a DAO and allow token holders to vote on changes made to the platform.

This is Web3.0. The goal of any dev. isn’t to sell out, it’s to create a functioning and fair platform with equal opportunity for all, including themselves. Ultimately, the devs of LooksRare will make more money than the devs of OpenSea (if LooksRare succeeds), even if OpenSea manages to sell out to Citi, because LooksRare performed a vampire attack on OpenSea’s userbase. Of course their users are all going to move to LooksRare, its the same business model, except they get paid. And worse, as soon as OpenSea and Citi started discussion, OpenSea censored art on their platform that made fun of Citi. Try the link, it no longer works. This chased away many users and created a vacuum for LooksRare to form.

All code in this space is open source, so if you aren’t the best at what you do, you exploit your users, or censor them in any unfair way, then you are absolutely open to having your IP stolen, and your market cut out from under you. This is the way. Intellectual Property does not exist and should not be protected.

Anyways, these types of DeFi are fairly straight forward, you own the token, you stake it, and you get paid if people use the platform.

This should be obvious but just in case, you probably aren’t going to earn that 700%+ APR. Their estimates will probably keep dropping until it reaches a reasonable bottom (maybe 200%), at which point people will probably bid the price of $LOOKS up, (which decreases the APR) until it gets to something reasonable. That of course is contingent on the platform succeeding.

Decentralized Leveraged Trading

Leveraged trading is where people go to lose money in general. Maybe the top 2-3% have both the emotional control and market knowledge to really do this successfully. If you’re thinking about doing it, but unsure… just don’t. But if you must, you can do this on blockchain as well. Leveraged trading allows you to take loans to enter a larger trade position than you could otherwise afford. The platform charges interest on these loans on a regular interval, usually every 6 or 8 hours. Sometimes if too much open interest is all on a single trade in one direction, you can get paid interest for opening a trade in the other direction.

I can’t give too deep of an explanation as to how this works, because frankly I don’t care too much. When I need to scratch the itch I use dYdX, which is a L2 on ETH. It is affordable even for non-whales because all of the action happens on the L2 which is gasless. You just pay ETH gas fees to deposit USDC. The platform also has a governance token $DYDX, which you can stake to decrease your transaction fees. It is awarded to people that hold open positions on the platform.

Decentralized Mortgages

This is a new form of DeFi that will be launching this summer in a few states here in the US. The project is called Theopetra. It is intended to be a self-repaying mortgage, however you do lose some of the rights to your house in that you are not allowed rent it to someone else, their goal is to help homeowners, but this is the first attempt at such, in the future there may be more competitors and even one allowing for rentals by the property owner.

The NFT’s for this project currently exist on ETH and STX and can be considered a ticket to access the project.

They simply take advantage of DeFi and deploy the home equity into a low risk money market that pays more interest than current real estate loans charge. You have to be approved as a buyer first through standard credit and income approvals. Once approved and selecting a home, Theopetra buys the home in cash, and then turns around and refinances the property to pull the equity out. So they have the home, and they have ~92% of its value in cash. They then deposit the cash into basic DeFi strategies to return ~20% APR on the cash, while paying 3.6% interest on the loan. You sign a home ownership guarantee that gives you unlimited rights and control over the property for 99 years (including the right to pass it on in case you die). The only stipulation is that it cannot be rented out. Each month after you pay the mortgage, Theopetra pays you the cash earned that month.

I’m a big fan of the people behind the project and I own one of the NFTs that would grant me access to use the project if I so desired. The project currently cannot operate in my state, so I may just sell the NFT depending on what things look like this summer. I look forward to more inventive uses of DeFi like this in the future.

Decentralized Collectors Items

The example I am going to use for this one is called ($WIVA) WIV and build on Ethereum, and it allows users to buy NFT’s representing real wine in a real vault and to deploy those wine bottles as collateral in loans. This protocol is still new and it suffers from one major flaw. If you actually want to take delivery and drink the wine, you can’t. But you can deploy them on the blockchain, and you can also stake the token representing governance of the platform to earn a return, however its not clear how that return is being created to me, probably because I haven’t looked too hard.

A competitor that actually fixes the delivery problem is called Winible, which exists as a NFTs on the ICX blockchain. These cannot be deployed in DeFi, but you can burn the NFT and have your exact bottle shipped to you. However this project is incredibly new and the devs behind it have been slow and behind on the communication, so this might not be the winner either.

Both of these examples are still incredibly new, and as more developers work with people that want to unlock the value of their assets we may start to see tokenization and delivery of real world assets, from rare cars, to actual physical art, to baseball cards, and any other sort of limited collectible that has significant monetary value. I would keep an eye out on this sector for opportunities to join projects at the ground floor, especially if they have an income proposition alongside the base speculation and ability to use as collateral in DeFi.

P2E Blockchain based Gaming

Let me start this by saying that most all examples of blockchain gaming are just not fun. This sector didn’t really pop up until last year with the rise of Axie Infinity. This was the first P2E game that seems to have some staying power and a decent team of devs behind it. The basics of the game is that you battle, quest, train, and trade these monsters that are represented by NFTs. The game has two tokens associated with it. $AXS which is the governance token and will allow people to vote on changes of the game. The platform charges 4.25% on all monsters traded in the marketplace, which is split between the developers, and those holding the AXS governance token. The 2nd token in the game is called $SLP, which players can gamble against each other when battling, or can earn when questing with their monsters.

The game gained significant popularity in early 2021 as the amount that could be earned was enough to finance an upper class lifestyle in smaller countries like the Phillipines, and turned some established financial concepts on their head.

One stat that struck me: Sky Mavis says 25 percent of its players have never had a bank before, meaning their Axie wallets are the first financial services they’ve been able to access. Simpson told me that in some places in the Philippines, people are paying their rent with the game’s SLP token. That helps explain how Axie’s total trading volume now exceeds $2.4 billion.

Looking at the marketplace for these, they are fairly cheap at the moment, but there is a lot more competition entering into this space. Last year some of the cheapest monsters were ~$220, but today, there are some that can be bought ~$40.

The game has several ways to make profit. One, you can just play the game and cash out the $SLP twice a month. Two, you can buy $AXS and stake it to take a portion of the trading fees on the market. Third, you can actually join a guild and lend your monsters to the guild. Guild members can borrow your monsters, and then pay you 30% of the SLP they earn with your monsters.

Competitors for this style of game are starting to pop up, with a few on the L1 $MATIC (Polygon) that may be pulling some of the liquidity out of the markets that previously pushed the price of monsters on Axie up to $220. Of interest are Crypto Raiders and Vulcanverse. I expect to see more of these games develop in the future, and if someone makes one that’s actually fun we could see long term adoption take place. For now, your best bet is to join one early, buy the governance token and one or two NFTs and just sit on it. You don’t want to be coming to one of these games late. Crypto is all about catching waves and riding them, not about finding projects after the fact.

Decentralized Yield Aggregators

A yield aggregator is essentially an automated contract that deploys your funds into DeFi for you, and collects the yield on your behalf. You obviously have double the smart contract risk as compared to engaging with DeFi yourself, but you have less of the user risk for error since the activities are automated.

We’re going to use Yearn Finance ($YFI) as our example, it is the oldest yield aggregator on ETH and a good example of what a mature aggregator can look like.

These are designed to do most of the work for you. All you have to do is show up, deposit your assets into a strategy, and YFI will do all of the work to maximize your returns on your behalf. Sometimes DeFi requires multiples claims, you won’t get notifications when rewards have arrived, or when its time to compound, or when you need to shift capital back into a queue again. You aren’t always at your computer or available to do this. An aggregator automates this work so that you can be more hands free and less likely to cause a user error. Usually the governance tokens of these platforms can be used to vote to add new strategies to the platform, and the assets of the platform can be deployed on behalf of the holders of the governance tokens, even with profits of the platform paid out to the token holders. Yearn is mature in the sense that I wouldn’t be trying to buy their governance token as there is probably not much speculative appreciation to be gained. However on other chains if you’re able to find new yield aggregators launching, they can be significant sources of income.

And there are a lot more than just these examples, and there will be even more as time passes because people are constantly inventing new ways to deploy assets. These are just ideas for you to understand some basic forms of DeFi.

3. Basic Common Sense

When you go out and start signing more transactions, you put your wallet and funds at more risk. While I was making this guide, I accidentally went to the wrong URL for the LooksRare NFT platform. It looks nearly identical, take a peek if you want.

The fake website - looksrares.org

The real website - looksrare.org

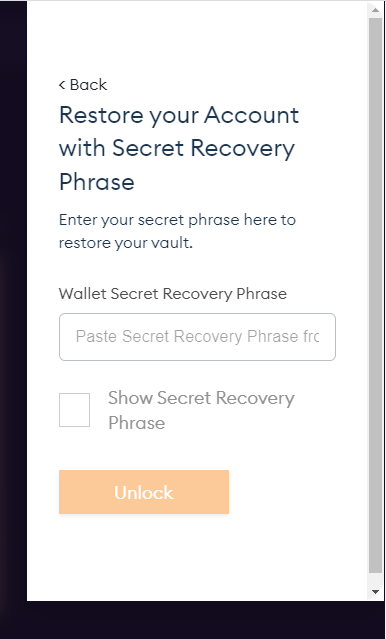

I didn’t notice at first but when I tried to open Metamask, I was prompted with an obvious scam intending to drain funds. Be very careful when visiting dApps, your wallet will never ask you to restore it with your seed phrases or recovery phrases; like in the screenshot below. If it does, just leave.

If you ever enter your recovery or seed phrases anywhere, your wallet will be drained of funds and there is nothing at all that you can do. No cops, no regulatory authority, no nothing. This site is not using an actual meta-mask integration but instead a spoofed version that looks real but has no functionality except to collect recovery phrases, and then duplicate your wallet elsewhere to then drain the funds.

There is no DeFi emergency so significant that you should ever ignore your common sense. If a site isn’t working the way its supposed to, leave. Don’t try to make it work. Just leave. Find the devs on twitter, telegram, or discord. Confirm with others that you’re at the right site. Confirm with others that the site is functioning properly. There have been instances sometimes when the security of the site can be hijacked and you can be asked to sign faulty transactions. There is no need to rush signing for a transaction if the output you are signing for looks weird. There is always another opportunity tomorrow. This market is evergreen for now.

4. Getting Started

So, for those of you that have followed the beginners strategy, you probably have some BTC and ETH at hand. However, there is no DeFi on BTC (except through STX), and unless you have over 6 figures in ETH, you may have trouble engaging in DeFi due to how many transactions you may have to sign and the gas fees charged for each one. So how do you get started?

Take some of your savings from ETH and BTC and move into alternate Layer 1 smart contract protocols that have affordable gas fees. Or on L2’s built on ETH that have gasless solutions. This is where you will engage in DeFi. Some decent choices here are below in no particular order.

FTM - Fantom

AVAX - Avalanche

TLOS - Telos

STX - Stacks

BNB - Binance Coin

NEAR - Near Protocol

XTZ - Tezos

LUNA - Terra

ONE - Harmony

ATOM - Cosmos (technically a Layer 0)

ICX - Icon

DOT - Polkadot (technically a Layer 0)

SOL - Solana

ALGO - Algorand

ZIL - Zilliqa

And I’m sure there are probably some I’m forgetting, and even some that are about to blow up that I didn’t list here. Leave them in the comments if you want. These L1’s I’ve listed are L1’s that have established and functioning DeFi dApps that can be used by a new user today if they have these assets in their wallet. No, I will not add ADA - Cardano to this list.

Another note, before you purchase any of these assets to use, you should find out which wallet is compatible with the coin you are about to buy and is used by the DeFi dApps on that L1. Google (DuckDuckGo), and sub-reddits are your friend for finding this information. Do not just assume that you can put the assets in your metamask, and even if the asset is compatible with metamask, you need to make sure that your wallet address is the same when used on a different network, this isn’t always the case, and its best to double check, there is no reason to rush when using a new network; you’re still early.

I also don’t recommend deploying 100% of your assets into DeFi due to the risk. As an FYI, only about 20% of my total crypto is in DeFi. Could I deploy more? Yes, of course. Do I plan to deploy more? Yes. But you slide into this slowly, and always need to have something outside of DeFi just in case something goes poorly.

5. Conclusion

Crypto is programmable currency, meaning contracts can be programmed into the very fabric of the currency itself. This is superior to other forms of currency that require constant administration by humans in order to deploy that liquidity. Now anyone, anywhere can engage in finance without any middlemen or gatekeepers profiting off of them. The move towards further decentralization will foment the further growth of dApps that empower users over the next decade. Engaging in DeFi allows you to actually turn the kind of profits that banks typically turn behind closed doors (using your money). If you are beginning to enter into this space, your best bet is to begin with a lower cost blockchain instead of ETH and to begin getting your feet wet. ETH is a whale chain and the people engaging in these activities in ETH typically have mid to high 6 figures in ETH alone to make the gas fees a bit more manageable, but even then there may be some returns from DeFi they get that are too small to be worth claiming. Learning how to do this now and be familiar with it will pay dividends. Credibly, maybe only 3-4% of the world population is regularly engaging in DeFi. You are still really early.

6. Giveaway

As I stated in Section 2:

I will be gifting a 1 year subscription to the DeFi Education substack in the comments to one of my paid subscribers on 1/28/2020.

This substack is a great place for information, its a group of ex-wall street guys that are extremely up on the tech as well. They combine a financial and technical assessment of how to value DeFi protocols with the assumption that you already know how to do the basics. It’s extremely useful for anyone wanting to dive further into this space. I am going to be purchasing a years subscription for one person ($100), the only rules are that you have to be a paid subscriber to my substack. I will be reviewing all answers given on this post and selecting a winner on 1/28/20.

For the prompt, you have 2 choices to choose from.

Leave a comment telling me a story about a negative experience you’ve had with an entity that you would hope to see replaced entirely by decentralized dApps and DeFi. Or leave a positive comment telling me about a future you could imagine being facilitated by the adoption of DeFi either through a type of DeFi that already exists, or maybe about a new type of system that you think could exist (you don’t have to flesh out all of the details).

For those of you that follow me on Instagram, you’re probably aware that my bank accounts have been frozen by mistake, and that it will take several weeks for them to unfreeze my accounts. Crypto fixes this. I look forward to the day when these banks no longer exist. I also am happy that I have crypto, it’s paying my rent and buying me groceries right now until my account gets unlocked again. I hadn’t planned on spending crypto right now, but I’m grateful that its here, and I’m grateful that I can convert my DeFi income into spendable currency right now. Without that I’d probably be running up my credit card right now. This only further strengthens my conviction.

Fiat is dead.

An article on using NFTs to conveniently fix some of the (albeit orchestrated imo) supply chain issues that seem relevant to the topic https://www.sdcexec.com/software-technology/ai-ar/article/21915598/spice-vc-nonfungible-tokens-for-the-supply-chain

For the loans could anything be written in? Like prepayment penalty or lack there of?

Confused about the difference between a liquidity pool and just buying something and selling it - but maybe the next level defi article will answer. I see it now as advanced payment and advanced sale price so to speak but perhaps that’s just my limited understanding.

Would you recommend the same wallets for defi as you did in the earlier crypto post? Ledger can’t handle much more than ETH/BTC from what I see or what I have - I like the cold storage concept.

Is there any way to tell other than relying on someone like yourself to identify what DeFi will truly replace banks like auto payment and deductions etc?

Apologies if these are all rudimentary, just the questions that come to mind. Not looking for a comp sub.

Is there a way to decentralize alimony payments so that someone else pays for them. Like this other person thinks they're investing but really they are paying for my whore ex-wife to vacation in Costa Rica??