Crypto Macro - Eth 2.0 Merge Part 2

Tokenomics, Sanctions, and Future Value

If you’re new and have a question, please read the FAQ post first.

Please refer to Definitions page for any terms or abbreviations that I use that you don’t understand. If a term is missing, please let me know.

Substack has launched an iOS app for those of you using apple devices. I am an android peasant and can’t tell you if its good or not, but check it out if you have an iPhone or some other such trappings of royalty.

This is the 2nd part of a 2 part post. Part 1 can be found here.

Table of Contents

Changes to Tokenomics

Capital Flows and ETH Price

ETHW Airdrop

Post Merge Risks

Philosophical Concerns

A Silver Lining

Conclusion

1. Changes to Tokenomics

One of the most important changes that the ETH 2.0 merge will bring about are changes to the tokenomics of Ethereum itself. If you are unfamiliar with tokenomics, I have a guide post here.

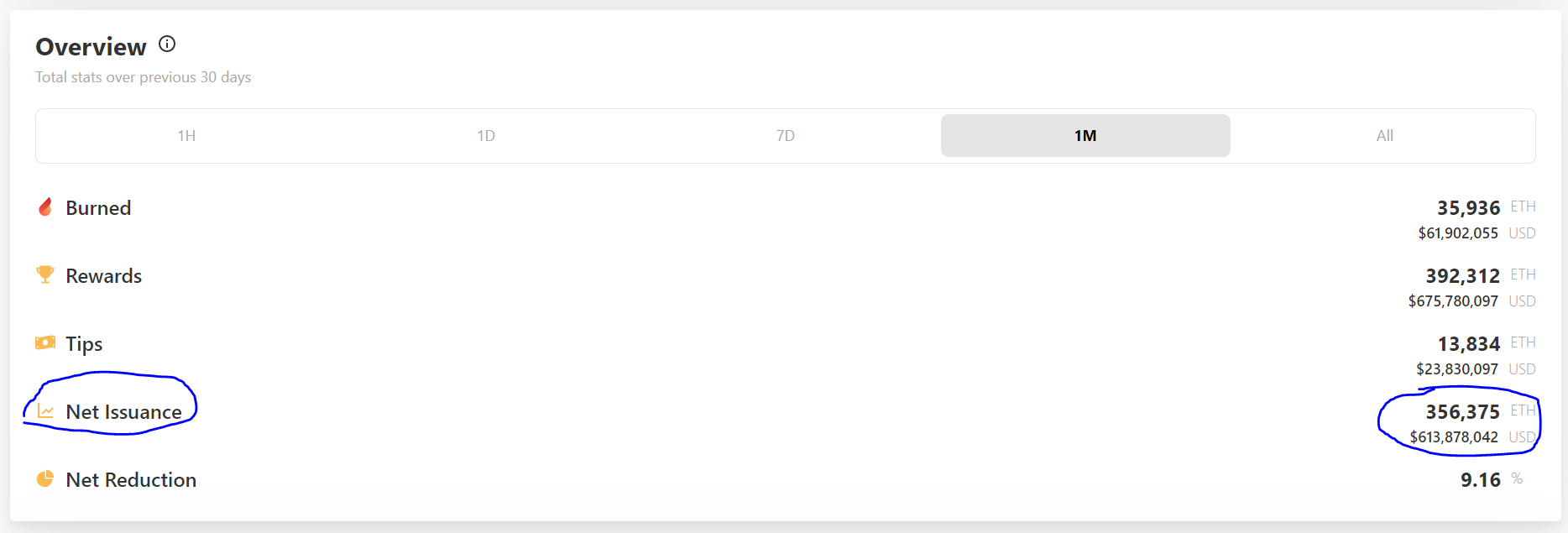

We’ve discussed net issuance changes to ETH prior here, but I’ll rehash that here first as it’s important to understand base inflation. We’ll be using metrics from WatchTheBurn which reads onchain data from ETH for each block solved.

In 1 month, we have a net issuance of 356,375 Ethereum to miners. As of 9/11, 10:05pm CST, there was 120.48M Ethereum in circulation.

The net monthly issuance results in a yearly net issuance of 4.27m new Ethereum. This would be a net annual inflation rate of 3.55% in new ETH issuance. The actual inflation rate of Ethereum from 9/11/2021 to 9/11/2022 was in fact 2.57%, but this is likely due to low ETH inflation in Q2 of 2022.

In roughly 2.5 days from now, the ETH 2.0 merge to PoS will be complete, at roughly 12:01am CST on 9/15/2022. The net issuance of ETH will drop drastically as the ETH miners will no longer be getting paid to solve blocks, and instead staking nodes will be solving blocks and the ETH inflation will be awarded to any entity staking ETH to those nodes. The new inflation rate will be dynamic and based on how much ETH is staked at any given time. ETH 2.0 net issuance is below.

Currently there is about 13.4m ETH locked in the ETH 2.0 staking contract. Which means that net issuance of ETH will drop down to ~0.6% net annual inflation after the merge.

This is a fairly sharp drop in token inflation, and while the ETH 2.0 merge will eventually drop the costs of transactions significantly, the update coming up on 9/15 will not decrease transaction costs in any meaningful sense. So we’ll see the issuance of new ETH decreasing, while demand for ETH to pay gas fees on transactions will remain high. So from a pure market perspective, net demand for ETH should increase. But obviously, the macro is more important than anything else. And as we will discuss in this piece, the price for ETH is likely to fall after the 2.0 merge completes successfully. The tokenomics of ETH will likely not play a major role in its price in the short term. It’s also important to note that once the shift to PoS is complete, the ETH that is locked up in the staking contract and receiving ETH inflation will still be locked. Users will be unable to withdraw them from the contract until later updates unlock this ability. So for an undetermined amount of time, none of the ETH inflation will be flowing out to the markets. How this will impact broader market sentiment is likely dependent on how long this will occur. In the short or mid-term this isn’t a big deal at all, but if the 2.0 staking contract remains locked for 6 months or longer there could come to be a decent shortage of ETH on the centralized exchanges.

Another important thing to consider is the following. Someone mining ETH on the PoW chain has expenses that they need to cover in order to stay profitable. So most miners really didn’t have very much choice on whether or not to sell the ETH they were rewarded into the markets. They had to sell to pay their mining expenses. The expenses to run a staking node are far cheaper compared to earnings, and users who stake their ETH to a node have virtually no expenses. So not only do we see a significant decrease in new ETH issuance, but we also see a significant decrease in recurring sales from miners.

The changes to tokenomics all point towards ETH price having to rise substantially after the 2.0 merge. It’s quite likely that we may see these tokenomics starting to take effect on ETH price within 4-6 months after the 2.0 merge, but there are some things that need to shake out of the markets first…

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.