The last few crypto posts have been heavy on STX. Each week when I sit down to write I find myself running into the most growth, activity, and excitement there. Several things have happened and are happening that I still haven’t covered beyond the airdrop opportunities so it’s better that I concentrate them all in one place so I can simply link back here instead.

Currently, the BRC-20 space is the most exciting to be in for the current crypto market. You can consider this post to be an extension of my previous two STX reviews which are linked below.

From an investor standpoint, this is a good thing. All successful blockchains become clogged at some point or another. Over the last 5-7 days (I wrote this on Jan 16th) the chain has gotten so clogged that many attempted transactions are eventually falling out of the mempool without ever getting processed. If this sounds like mumbo-jumbo to you, then you need to simply understand this; a transaction needs to be processed in a block by a miner within 2-4 days of submission, otherwise, it will be deleted (and you will lose your gas payment). So you need to choose a transaction fee that matches the current network usage, which you can check here.

While the network is congested, you can get estimates for suggested gas costs to get transactions through. It changes on a semi-regular basis. You’ll note that different types of transactions have different suggested gas costs. A transfer is the simplest form of transaction (underlined in blue) and requires the least amount of gas, while a smart contract call (checking a function but not making a transaction) is the second simplest form and requires the amount underlined in red. The last value does not matter to most of us, but it’s the cost for deploying a new smart contract, you can see those costs are 15-20 STX at the moment and slowing down many of the updates and deployments that dApps are trying to do now.

So for now, check the transactions page of the block explorer before making a transaction and use the medium-high priority number underlined in red if you are using DeFi, and the number in blue if making a simple transaction.

Unfortunately, it seems every week a new version of inscriptions/ordinals is launched on STX so as soon as the first set finally clears out a new version launches and we go through the same thing all over again.

The suffering never ends

I feel angry that all of these degenerates are getting in the way of my humble airdrop and DeFi farming. But rationally, I know that this is the best sign I could get regarding long-term price appreciation and usage of the chain. I sat in an empty restaurant and happily ate the food for the last 2 years, and now I have to wait in line to eat the same food.

Inscriptions take up a lot of block space compared to their tx cost

Earlier in the week, I was hopeful that this spike in transaction costs was because something was wrong or the network was broken in some form or fashion, and thankfully there kind of is. Inscriptions with images in them eat up a lot of block space, but the miners view them as simple transactions. So when choosing which transactions to prioritize for block-space, the inscriptions get prioritized despite being under-priced for how much data they consume. I have been told the team is attempting to fix this.

Thankfully, the team is trying to optimize this

Even though I am happy people are eager to do things and new launches seem to be every week, I am tired of gimmicky inscriptions being minted by airdrop hunters clogging up blocks with pixelated images that will be forgotten less than a month from now.

Unfortunately, that also means that as I’m writing this, the chain explorer I would typically use (stxstats.co) is broken and not functioning, so I had to trust a 2nd party for the data as I’m unable to look at it myself.

It would appear as if the number of daily transactions on STX has increased from our average of 5,000 daily which was established in 2022, to roughly 9,000 daily for most of 2023, to a range of 20k-60k a day since mid-December 2023.

Like ETH users in 2020 during the second half of DeFi summer had to get used to rising gas prices, so too will we in STX have to get used to rising gas prices. When farming and utilizing DeFi, it will be important to consider round-trip gas costs before making transactions, I’ll get into some of those in section 3.

Because the stats page is down due to network congestion I also have no picture for unique address growth since Summer 2022 nor for active addresses in Summer 2022.

We can guess though that daily active addresses are probably in line with the recent pump in transactions and are nowhere near the 2k-5k we had in the summer of 2022. There are probably 20k-40k daily active addresses if not higher now.

Stacks transactions were only considered final according to the history of the Stacks chain itself. Although block history was recorded to Bitcoin, Stacks could fork, meaning an attacker could rewrite the history of the chain by only outspending Stacks miners. With Nakamoto, Stacks does not fork on its own and miners are required to build on top of the true chain tip at the protocol level, so there is no way to change the history of confirmed Stacks blocks without changing the history of Bitcoin blocks themselves. And, with Nakamoto, after a mere 2-block time period, Stacks transactions will become as final and irreversible as Bitcoin transactions themselves.

I’m not going to get too deep into the current state of mining or what it used to look like, that’s not really relevant right now, you can read up on that on your own here. Just know that in the current network state, incentives do exist whereby a malicious actor could 51% attack the blockchain without risking too much permanent capital. With the Nakamoto upgrade this will become far more expensive and a malicious actor could only alter the current block being mined and not previously mined blocks.

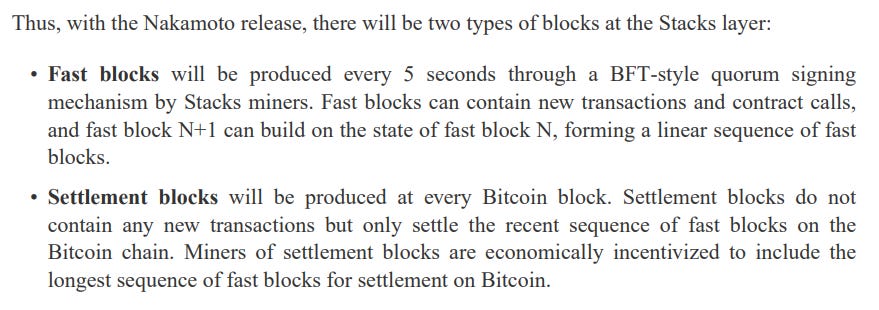

An important part of this upgrade to users will be about speed. Currently 1 STX block is mined alongside 1 bitcoin block. Bitcoin has a block time of ten minutes, which means that STX also has a block time of 10 minutes, so the finality of STX transactions can take 30 minutes or more at times. However, if you look at the updated whitepaper for the Nakamoto Release, you’ll see that the new block time will be every 5 seconds allowing for much faster transactions on STX and much more throughput than currently.

sBTC

We get a new asset sBTC as a result of this upgrade as well. sBTC is a form of BTC on the STX blockchain. It is fundamentally different from all other forms of wrapped BTC (xBTC, aBTC, wBTC, etc.) for one simple reason. Since STX miners are writing to the BTC chain directly and can read the entire state of the BTC chain and write modifications to it in the settlement blocks, this means that they can trustlessly manage BTC without involving any centralized authority.

Now a user on the bitcoin chain could lock a certain amount of BTC to a “peg wallet” on the bitcoin chain, which would mint an equivalent amount of sBTC to their STX wallet. This sBTC can now be deployed into smart contracts or used in DeFi. What makes this different is that rather than having a single custodian or a multi-sig wallet controlling the native BTC sent to the peg wallet, this wallet is now controlled by the entirety of the stacking network itself (anyone can become a STX miner or unbecome a miner at any point in time), and since STX stckers are paid out in BTC themselves they have a strong economic incentive to ensure that all transactions are legitimate. 70% of STX stackers must sign off on “peg-out” or withdrawals of sBTC back to the BTC network, and to do so would currently require $186,377,284.52 of capital to perform.

70% of this is required to maliciously over-write sBTC activities

Not only would that 70% have to be put at risk and stacked, but it would also have to go unnoticed for 24 hours to be confirmed, which is highly unlikely. This also allows for atomic swaps of sBTC for BTC since STX miners can write to the bitcoin chain, and we will likely see protocols arise that allow for users to swap BTC and sBTC between themselves in a handful of settlement blocks if they do not wish to wait for the 24-hour confirmation of the sBTC withdrawal.

I view this upgrade as a massive game-changer for the current bull market and do not think people should be sleeping on it or STX as it heads into the summer.

STX Halving

Did you know that STX (just like Bitcoin) has a halving cycle? Current block rewards for STX miners are 1000 STX per block, but in year 4 of the STX network this is supposed to drop to 500 STX per block.

When is year 4? It’s January 2025. But the date isn’t set in stone. There is an ongoing discussion in the STX forum about an appropriate halving schedule and it’s possible this initial halving gets pushed back to 2028.

Currently, the budgeted supply of STX in 2050 was set for 1.818 billion STX in circulation. Even if the initial halving is pushed back to 2028, this will place the STX in circulation by 2050 at 1.87 billion, which isn’t much higher than the current outlook. Sticking to the original schedule, or even pushing the first halving to 2026 or 2027 would still keep STX under its target for STX in circulation by 2050.

This is important because as the SEC eventually matures into the understanding that crypto is here to stay and cannot be bullied, it will have to allow for a legal framework to be drawn up by the legislature for how to treat cryptocurrencies.

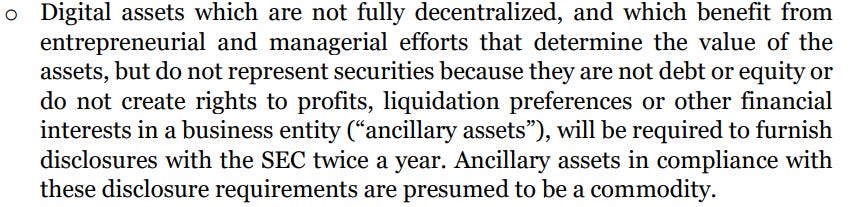

This is the big negative one here. They are essentially going to apply the Howey test to all digital assets and require those that classify as a security to furnish disclosures to the SEC twice a year. Basically nothing new will be developed in the US unless it has major VC funding behind it. These sorts of filings with the SEC are extremely difficult. Only a small handful of protocols have even attempted this, of which $STX is one of the few (my review of $STX here). $STX was one of the few filing reports with the SEC (despite not being required to do so). This is a difficult, time-consuming and expensive effort to undertake. STX had significant backing and a strong legal team which made this possible for them to do.

My gut tells me that the rules in the US will eventually flow into the following framework. Decentralized Layer 1’s and Layer 2’s will be treated like utilities and allowed to function without registration with the SEC. All protocols built on top of them or that fail to decentralize will be treated like securities and required to register and make twice-yearly filings. It’s quite possible that entities like UniSwap (based in NY) or dYdX (also based in NY), will have to start filing with the SEC regularly and we may see these entities doing token buybacks or simply moving to get rid of their tokens in circulation.

Many protocols have tokens for no reason. If all it gives is governance votes to the user base, there is no practical purpose for the users to hold them. Both Uniswap and dYdX do not share a portion of protocol revenue with token holders, and token holders only get nominal benefits. In such a regulatory future I think we likely see more companies launching products and protocols on-chain that have NO token. Coinbase’s BASE network has no token and states it never will. I get why, the network is fairly centralized and they likely have no plans to decentralize it. Why open themselves up to that future regulatory risk if they have no plans to decentralize?

Expect a future where only the truly decentralized assets in crypto have tokens. The current market where every protocol launch comes with an airdrop of pointless tokens with no function will one day be something we wistfully look back on in memory. Right now, they are just giving away free money in the hopes of buying market share. In time this will come to an end.

And you will miss it when it does.

But that is not this day my fellow degens. Let’s get back to talking about the present. These airdrops won’t farm themselves.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.