February US Bond Auctions

The Taper begins, and its not pretty

I have now segregated US bond auction updates into their own separate post. This will be the first of a monthly series of posts updating the bond auction rates and bid to cover ratios. I have previously covered these within the weekly updates. I consider this to be the most important part of what I am covering on the substack and it is where we will see the first signs of distress within the market that the federal reserve cares about the most.

Please refer to the Backdrop Post and trade with mindfulness.

Please refer to Definitions page for any terms or abbreviations that I use that you don’t understand. If a term is missing, please let me know.

As usual, this post has become too long for email, please be sure to visit the substack website and view the post there.

Table of Contents

State of the Narrative

Primary Auction Results February

Bid to Cover Ratios

Interest Rates

Secondary market Treasury rates

Market Impacts

Conclusion

1. State of the Narrative

All future monthly bond auction updates will begin with a review of the existing narrative from the federal reserve as well as recent actions from them that affect the bond market.

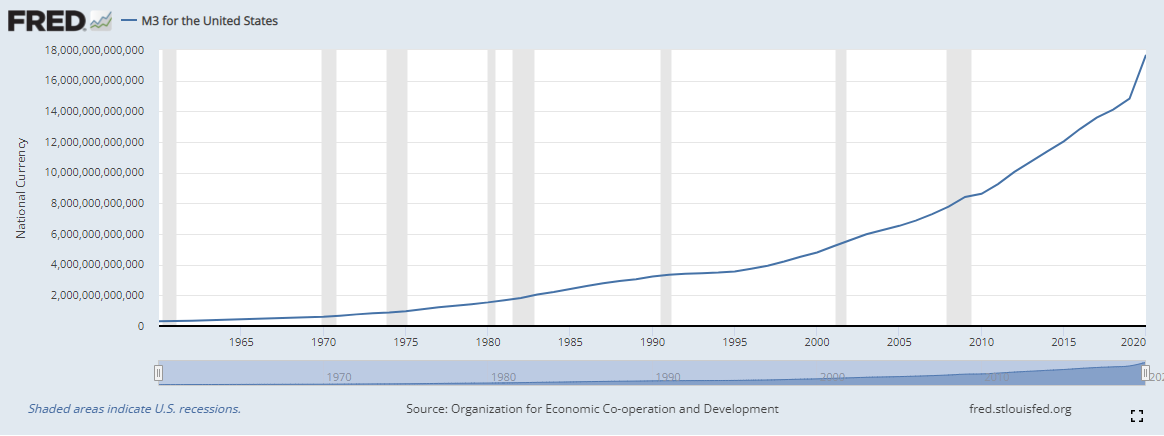

As I have covered in the Backdrop post, the US federal government has been running deficits for quite a few decades now. In fact, every president over the past 60 years has run a deficit (yes, including Clinton, they lied about that, he spent Social Security money in place of selling treasury bonds). To fund deficit spending, the US government sells treasury bonds. When real people buy these bonds with real money they earned from participating within the real economy, there is absolutely nothing wrong with that system and no undue negative externalities occur. The problem occurs when the US government has the federal reserve print money to buy those treasury bonds. We have been engaged in this sort of money printing for deficit spending extensively since the mid-1950’s. I’m not here to blame Joe Biden, he is an extension of a system that has been in place. His only fault is in failing to fix the problem and making it worse, which every single president before him, except for Jimmy Carter, is also guilty of. Jimmy at least tried, although he also failed to end the problem, he did at least strengthen the currency through his Federal Reserve appointment. This may sound extreme, but without Carter appointing Paul Volcker to head the Federal Reserve in 1979 the country likely would have descended and the 90’s would be remembered as a very different decade. The US today might resemble something closer to Brazil or South Africa.

Currently the US Federal government has over $30T in bonded debt. When this substack started, there was just short of $29T in bonded debt. We are budgeted to run about a $3T deficit every year. This means that the US treasury has to sell at least $3T in treasury bonds every year in order to cover the deficit spending of the government. The US treasury pays interest on these bonds to the entities that buy them. This works in the following way.

Treasury notes have a fixed redemption price. At maturity you can turn it in and receive the amount of cash on the note. So lets pretend you are going to a treasury auction. On auction is a treasury note that can be redeemed in 1 year for $1,000. Entities make bids on this note and the winning bid, lets pretend is for $970. This winner now has to pay $970 to the treasury, and in 12 months, whoever is holding that note can return it to the treasury for $1,000. The treasury is paying $30 in interest on a $970 loan over 12 months. This amounts to 3.09% interest. This is the only interest number that the treasury sees. The entity that bought that note, may decide to sell it on the secondary market. This note might fall in price or rise in price on the secondary market. Lets say it gets sold 1 month later for $950. The entity that bought it is now receiving $50 in interest over 11 months, and we could say that on the secondary market this 1 year treasury is now trading for 5.62%. This activity has no direct impact on the US treasury.

The distinction in the paragraph above is important for you to know. Treasuries have a primary market, which is the only interest rate the US treasury has to pay. Treasuries have a secondary market and people often talk about that interest rate, but it has no bearing on what the treasury is paying. In these posts moving forward, I will be outlining both the primary rate, and the secondary rate.

When the federal reserve prints money, they do so to buy up treasuries exclusively in the secondary market. They do not participate in the auctions in the primary market, probably because that would be an incredibly naked conflict of interest. They instead print money to buy treasuries on the secondary market. Entities that are well aware of this because the federal reserve tells them months in advance how much they will be buying go to the primary auctions and are willing to pay extremely low interest rates for these treasuries. They do this because they know that the federal reserve will still buy these treasuries from them at an even lower interest rate. So they buy a treasury and flip it to the federal reserve in the following week. If they do this every month or every week, they can turn a note yielding 0.2% into a 6-7% profit margin. This is absurdly brainless work, but is one of the few things you can do when you need to figure out how to make money on a couple hundred million dollars. Last year that would have outperformed the official CPI number. Many people ask why anyone would pay 0.5% for a treasury bond when official inflation numbers were 3% or 4%. The answer was because they had no intention of holding the treasuries to maturity.

The federal reserve tells these entities many months in advance when and how much money they will print and allocate to buy treasury bonds on the secondary markets. Now as many of you know, the Federal Reserve has committed to decreasing their purchases of these treasuries on the secondary market every month. And we have seen interest rates paid at the primary auctions steadily increasing as these entities that were making money by selling treasuries to the federal reserve have stopped bidding as high for US government debt as the money they were receiving has been drying up.

Officially, the Federal Reserve is scheduled to turn off the money printer on March 15th, which means that next months primary treasury auction will be the last one where entities can still turn around and sell those treasuries to the Federal Reserve on the secondary markets. Below is a chart of the US 2 year treasury bond on the secondary markets. In September, they were trading for 0.2% on the secondary market, it’s now february and they are trading for 1.5%. The federal reserve has essentially already lost control of interest rates on this note.

It will likely spike up significantly in March and April. And as I am writing this paragraph right now, I have yet to look at the primary auction rates. To be honest, I don’t need to look at them to know what is happening. You do this long enough and you know whats going to happen. In much the same way that if you do technical analysis on a chart long enough, you no longer need to draw any lines. Like Cypher in the matrix, eventually he didn’t even see code anymore. The end result of this is obvious. The entities that have been making money by selling treasuries in exchange for fresh inflation are either leaving this market, or are bidding far less in the auctions.

We’re going to now take a look at how the February primary auctions performed, and then we are going to cover what the consequences of this retraction of liquidity will be, and how those consequences will manifest in the markets that matter to us all. The primary and secondary treasury auctions should best be thought of as the price of money. The price of money ultimately affects the price of everything else in exchange for that money. I firmly believe that it is impossible to understand prices in any other market if you do not understand the price of money first.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.