The Real Estate Problem

The Real Estate Problem

There is no crash in sight... and that's a problem

By now I presume most of you are familiar with the concept of a K-shaped recovery. I am going to explain it here while focusing on how it is affecting real estate in the US both for renters and for property owners. This post is not actionable trading advice and as such will be free.

For those of you that follow me on Instagram, I left an open-ended question in my IG story asking people how much their rent was going up and included an example from NYC showing rent going up by 32%. I wanted to get a feel from my followers what if any rent increases they had been experiencing and where they were so as to be able to get some informal data together in order to provide some conclusions to you all from this information.

I have added a Definitions page which will include all of the terms and abbreviations that I use from now on and will be referred to on every post.

The images will make this post too large for email, please come to the substack website to read the post in full.

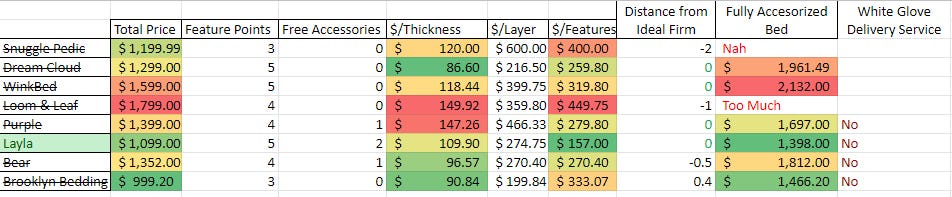

Back in 2020, I made a spreadsheet comparing all of the different states to see what I stood to gain or lose by moving to any specific state. I am sharing it here for you all, you can simply download it and make changes to the input tab to see what the best states might be for you to consider. There are instructions on each tab for how to use the spreadsheet. It may be a little behind the times as things have changed in the past 2 years (tax rates, constitutional carry, etc). Be aware that the rankings will change based on your income, annual expenditure, and the value of your property.

Also, I love spreadsheets. I use them for everything whenever I am making decisions, even on things as simple as “which mattress should I buy?” I find it much easier to make decisions and to live with them when I can quantify my options.

Table of Contents

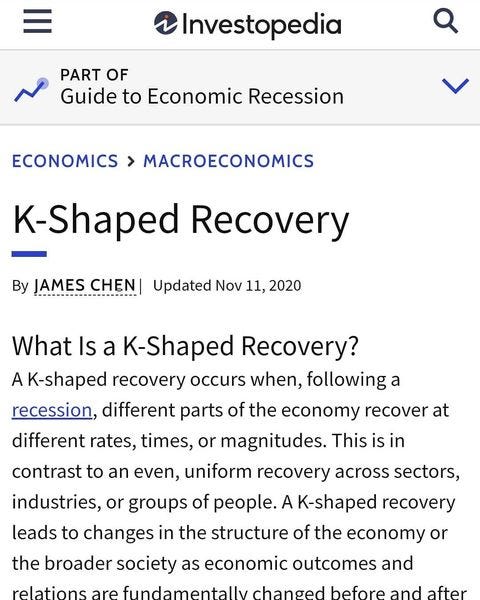

What is a K-shaped Recovery

What are Rents Doing

Cost Increases

Housing Shortage and Demand

Will Real Estate Crash?

Should you buy Real Estate?

Conclusion

Instagram Responses

1. What is a K-Shaped Recovery

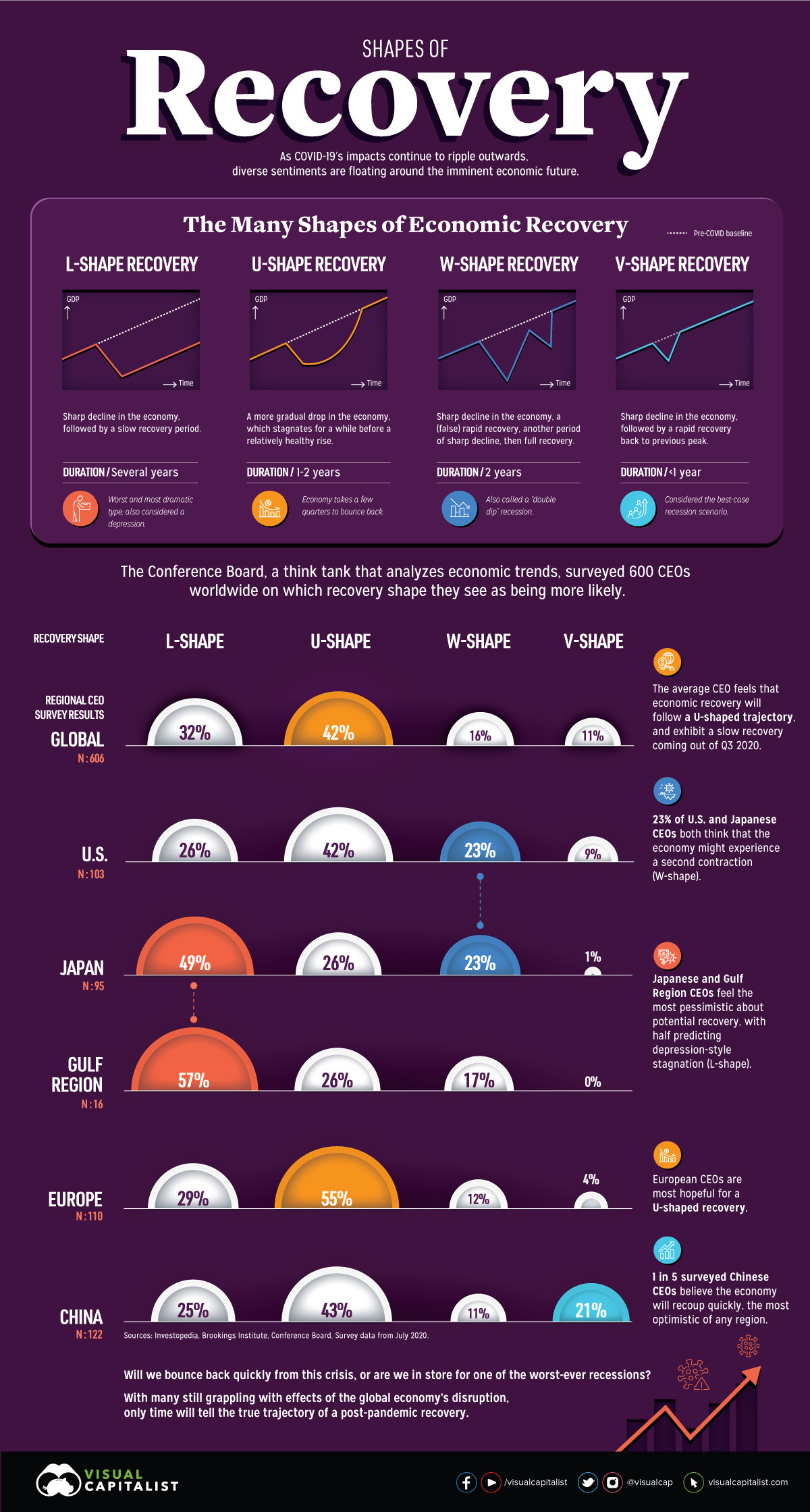

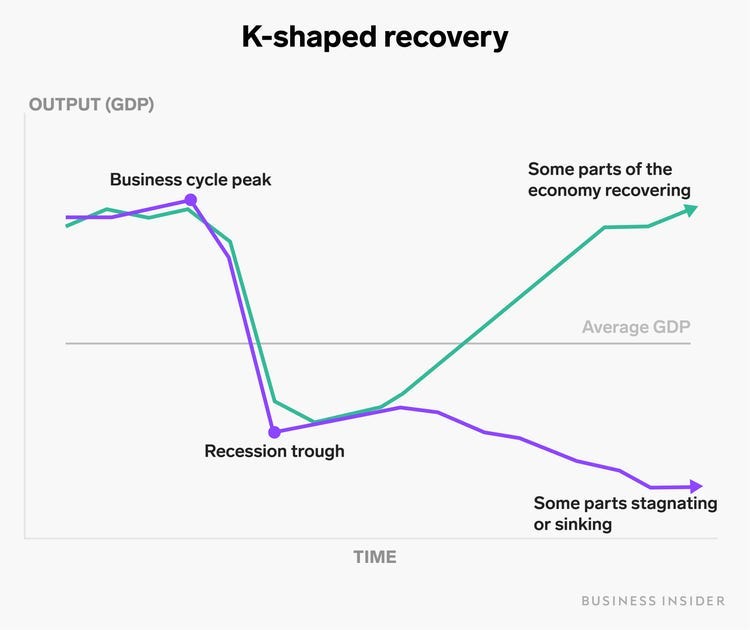

When economists discuss recessions, they typically also discuss what sorts of recovery might be made after the recession is complete. Typically, they just use letters to denote the shape of the recovery.

This is fairly straight-forward so far, the type of recovery we are going to focus on here is K-shaped. The basic thesis of a K-shaped recovery is that two pieces of an economy that were otherwise moving and thriving together end up separating after the recession. With one piece recovering back to normal, and the other stagnating and falling behind.

I started using the term to describe the recovery from the March 2020 crash later in 2020 on Instagram. My first explicit post on the matter is below and was mainly focused on how publicly traded large companies would be insulated by imbalanced regulatory enforcement (Walmart open, but smaller stores closed), while smaller companies would go under.

Since then, my interpretation of the K-shaped recovery has evolved quite a bit. I am mainly focused now on how different states, and different cities and different countries will recover from the last crash. If you’ve been reading the substack for a while, you are probably aware of how different countries central banks are setting them up to either fail or thrive post-CoVID. The same concept applies to US states and even applies to different cities within the same state. Simply put, not everyone nor every place will recover from 2020, and in truth, every recession has a K-shaped recovery because there are always people and sectors that get left behind. But that’s not relevant for today’s post, it’s mainly important that you understand what the concept is behind a K-shaped recovery.

2. What are Rents Doing

So yesterday I posed the following question on my instagram.

So far, 65 people have responded with data. Not everybody told me where they were from, and not everybody told me what the percentage increase in their rent was, some people answered in dollars. This is fine, I prefer not to pry where people’s privacy is concerned and will share some anonymized responses here as well as some of the data and findings I noticed.

Keep in mind, all of these responses are the anecdotes that my Instagram followers and friends have chosen to share. There is always the possibility that someone is embellishing, mis-remembering, mis-calculating, or doing something on purpose or accident that invalidates their response. So we can take these with a grain of salt, but the trend holds true. Also, please ignore my spelling, I don’t spell check at all in DMs.

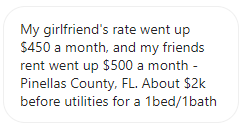

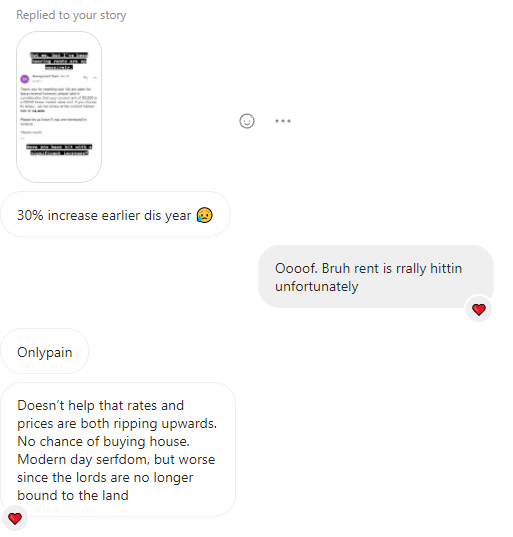

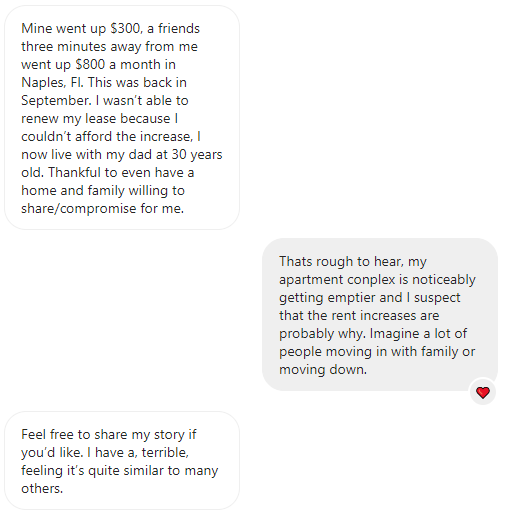

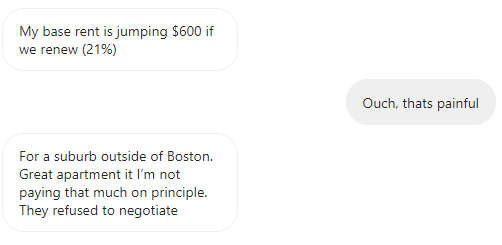

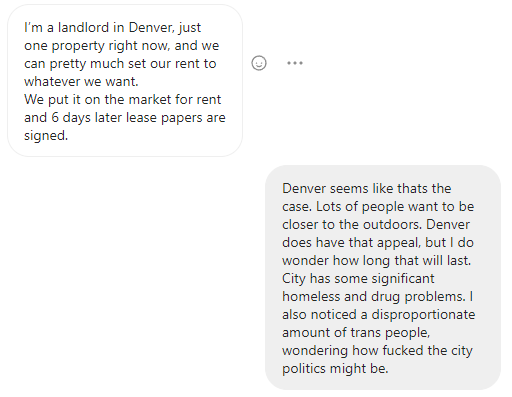

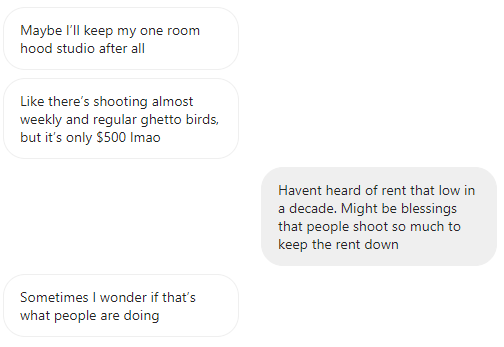

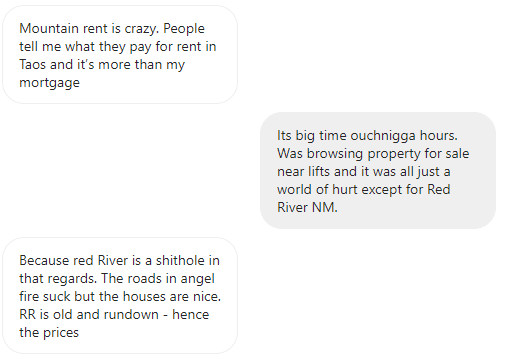

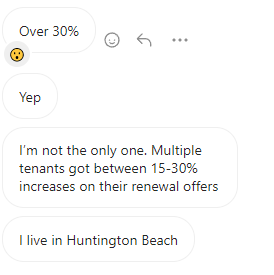

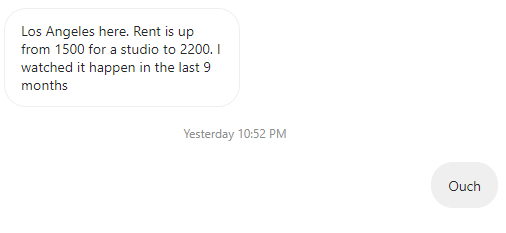

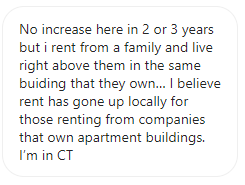

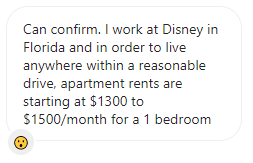

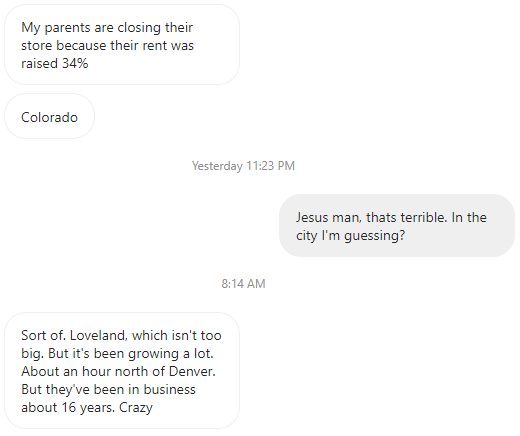

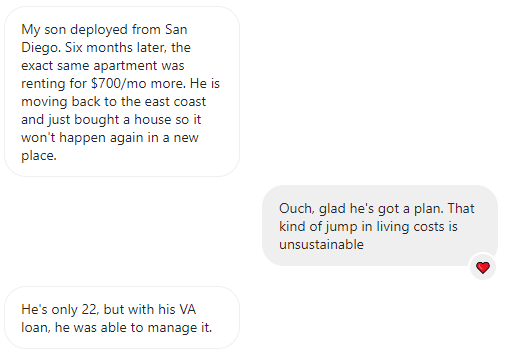

I included most (but not all) relevant DMs in section 8 if you wish to read through them.

The main trend that stuck out at me from everyone’s responses were that the largest increases in rent that I was consistently seeing were in two types of places.

Warm, beach cities

Near the mountains

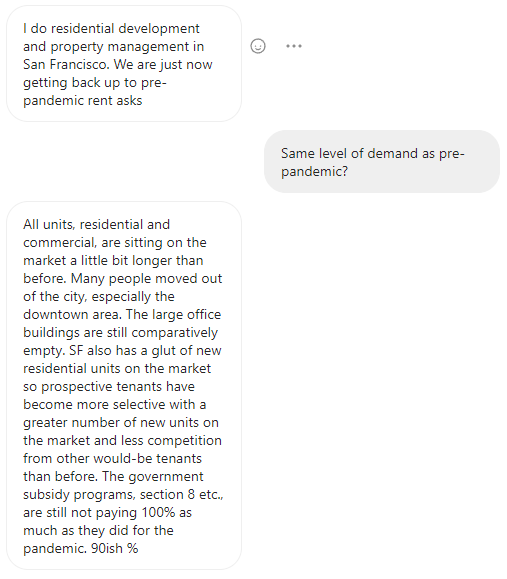

This, of course, makes sense for a few reasons. The most obvious reason is that there are quite a few people who were shifted to remote work by CoVID and no longer had to live in whichever city their job had required them to live in. You’ll notice that one DM showed that San Francisco had only just gotten back to it’s pre-CoVID level.

While there are several responses from SoCal (San Diego, Los Angeles, etc.) discussing rents going up significantly. San Francisco and NorCal are probably less desirable for Work From Home, than San Diego is, so I would suspect that of those people moving purely for a better work from home environment, more would have left San Francisco than left San Diego.

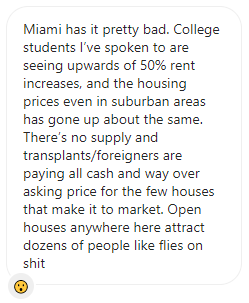

Then of course we have several examples from Florida, in fact, I would suspect that the majority of responses were from Florida despite the top 5 cities my followers reside in not being in Florida.

There are a lot of responses with people from Florida seeing significant increases in their rents paid.

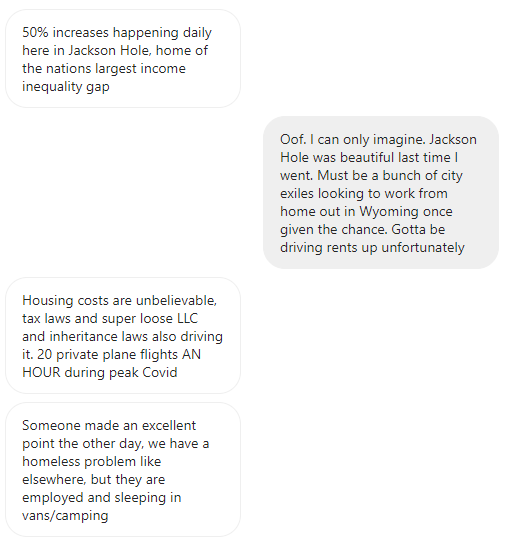

This seemed to be representative of a lot of Florida, with people mentioning the same issue across a number of different cities and counties in Florida. So when it comes to beaches here in the US; Southern California, and Florida consistently showed the largest increases in rent. The other side of this are the mountain towns close to winter-sports and recreation. I received some significant responses covering rents in Denver CO, Salt Lake City UT, and Jackson Hole WY.

There are several more examples in section 8 below if you wish to browse through them. Currently, I see two factors at play causing rents to be driven up this high, and in some places it’s a combination of both factors occurring. The first factor is simply demand re-pricing market rents in desirable areas as people who previously had to live in Grand Rapids, Buffalo, Fort Wayne, Des Moines, or another such city for work have been freed to move where they please. People in general are going to be choosing leisure or to decrease their expenses. Someone moving from a state where they pay 3% on their income to the state to a state with no income tax might be willing to pay that additional 3% of their income in rent and as such drives the market along, not to mention those able to move tend to have more disposable income and are skewing the income distributions of the cities they move to We discuss this in Section 4. The second factor is cost appreciation driving up landlord expenses. Part of those costs are inflation related, as appliances and qualified labor rates are increasing significantly. The other major parts of those costs are in property tax rates. Property tax expenses are passed along to the renter, so when the state raises property taxes or when property appraisals appreciate significantly this can represent a large increase in costs to landlords. We’ll cover this appreciation in costs in section 3.

3. Cost Increases

There are several sources of cost increase on the landlord side that are driving prices up. On the one hand is the obvious, inflation, which is driving up the prices of repairs, roofing materials, labor, and appliances. We won’t go too far into that here. The other, which is far less understood is taxation. Yes, one of the big pushes for cost increases is taxation.

This is probably the most important post I ever made on Instagram about what was coming down the pipe, and as always, that which is the most important is often the least understood.

Back in 2020, state budgets were experiencing an unusual and unexpected crunch. Those states (and cities) dependent on state income taxes were finding that when the IRS allowed for people to defer their income tax filings to July 15th instead of the normal April 15th that it put them in a crunch. The states have to balance their budgets, with an initial draft budget in June, and often a finalized budget in July. But with the IRS allowing people to defer income tax payments until July, this meant that states (and cities like New York City) dependent on income taxes were unable to write their budgets as they could not estimate the missing tax income. They also had to account for decreased income and sales taxes in 2021 for the 2020 tax year when making budgets for themselves. Some especially short-sighted cities like Seattle, wrote a loan for themselves in 2020 based on projected income for 2021-2022 (they are so far making less than they projected to pay back that loan). Their only options were either to be bailed out with printed money from the federal government (which many states were), or to enact significantly more taxation in the future. Almost every single city, county, and state saw increased expenditures during 2020, and quite a few sold municipal bonds to cover over-runs in their budgets. But, as stated, they could not print money to cover these shortfalls, and have to pay these back in some way, either by cutting spending or increasing taxes.

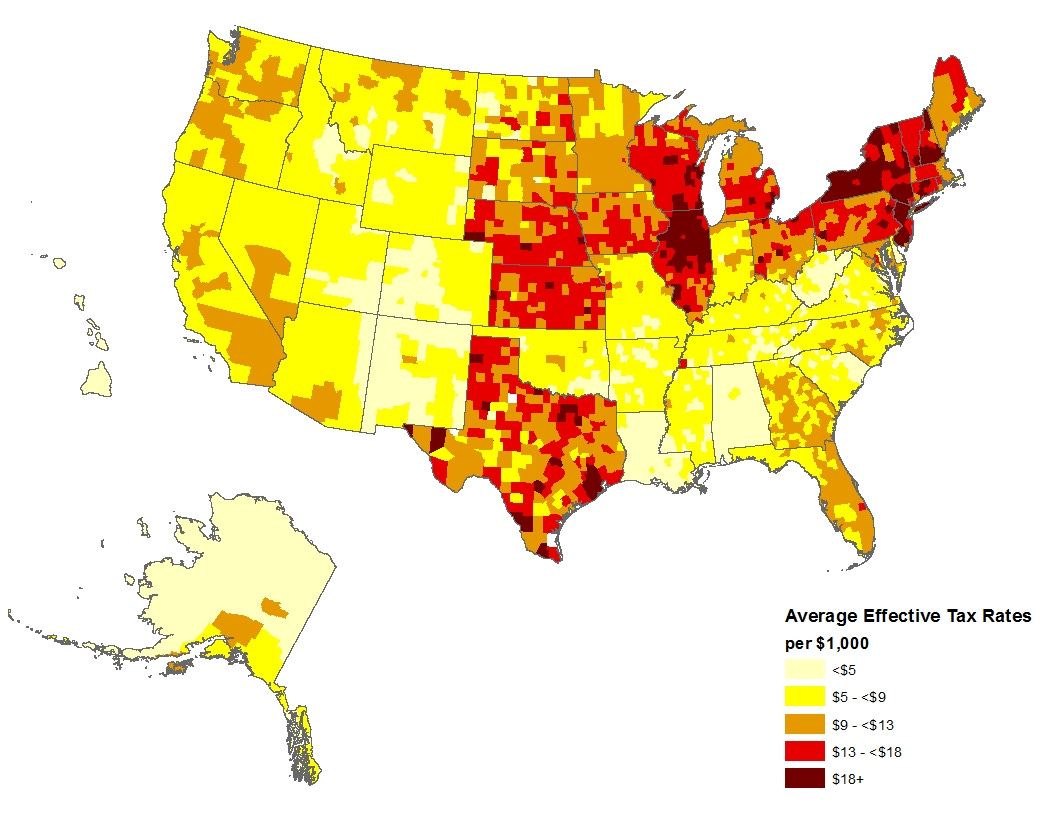

Now you see why one knock-on effect from pandemic spending comes out in rents. Property taxes. Below is a map of property tax rates, with the darkest red being ~2%.

But of course, just knowing the bare property tax rate is not very helpful. Some counties in Nebraska may have a 2% property tax rate, but $50,000 might buy you a 10 year old 5-bedroom home with a 3 car garage. While in California you might be paying 1% on a 2 bedroom crack-house that cost $800,000. Nebraska’s 2% costs you $1,000/year, while California’s 1% costs you $8,000/year.

The real issue driving the change here is a combination of appraisals rising, and property tax rates rising at the same time. Typically municipalities account for this by setting a dollar value of property tax money in their budget, and then moving the tax rate up or down. Some areas that saw significant property appreciation actually moved tax rates down because they didn’t need as much money as they would have taken in. Some states also have caps on how much municipalities can raise revenues in a single year, which is forcing some areas to cut tax rates due to appreciation. But these sorts of caps, don’t exactly apply evenly. Some property values increase significantly faster than others, and some types of exemptions to property taxes only apply to residences, while rental properties and apartments can have their property tax payments rise with no cap on annual increases. You can see how this ends up shaking out then. During time periods when properties rise in value the fastest, the largest burden of changes in property tax payments are felt by rental properties, which means the people that are renting their domicile take this on the chin the most.

One thing people also forget when comparing property tax rates is that there is a state property tax, and then counties, cities, and even municipalities within a city can add an additional property tax on top of the state tax rate. You may find that living in a rural county in Texas has a far lower property tax rate than living in Denver Colorado, or Phoenix Arizona, despite the state property tax rate being less than 1/3rd that of TX’s state property tax. It is quite advantageous to be considering property that is not in a county with a large city. For instance, if we take my city (Houston), Harris county has a 2.03% property tax rate, while just one county over it drops half a percent. For those wishing to live near large cities, it can be a significant benefit to simply move to the cheaper side of the county line, especially considering how the impacts from 2020’s budget issues will echo across the next decade.

Those areas most likely to be distressed are going to be those that have large population centers. Counties neighboring large cities may find significant inflows of taxpayers, while not seeing significant increases in expenditures. While cities will see the opposite occurring. Even from the perspective of a landlord, the return on investment from property that is a 30-40 minute drive from the city center might be more profitable than that within the city simply due to less uncertainty in changes in tax rates. This sort of disparity in outcome is what drives K-shaped recoveries. As local government budgets get stretched, they will drive people in their decision making. Whether those decisions are to lower property taxes further, or whether their constituents drive them to further punish landlords. Its not so far-fetched to imagine that in 2023 or 2024 there is sufficient political will for a landlord tax which will only further constrain the number of rental properties available in an area, and I’m sure as landlords decide to sell, Blackrock will be there to outbid anyone wanting to own.

Of course, living 30-40 minutes outside of town has many drawbacks, especially if the recovery is stronger than I currently expect it to be for the middle class. Being a long drive outside of the action of a city means you can’t do certain things, and life is short after all. Who wants to live in a rural area if you don’t really enjoy and prefer it? It’s a tough question, and we are all taking bets when we choose where and how to live, especially if we have a career with few options in rural areas for employment. But, where there is a will, there is a way.

4. Housing shortages and Demand

The other half of considerations driving rents up are housing demand imbalances. One issue that has occurred is that home building has slowed down significantly since 2008.

The housing crash significantly shocked generational decision making. Many cheap properties flooded the markets in the decade after the 2008 crash. There are still some towns in Michigan and the rust-belt where over 1/4 of all of the homes in the town are owned by the bank and have been owned since foreclosure in 2009. When banks foreclose on a lot of properties that are close together, they can’t put them all on the market at once, otherwise they will drive prices even further down. They instead keep a small portion of them listed and hope to slowly sell them all over time. In a hot market, this strategy works fine. But what happens if you have 30% of all of the vacant homes in Flint Michigan owned by the banks? What happens if no one comes to buy them because no one wants to live there? Well, you have a market flooded with supply with little incentive to build. Across the board, as these foreclosed homes slowly sold back into the market, demand for new construction in areas of high demand rose. But many areas stagnated and never recovered.

But now think, where would all of this new construction have occurred? Would those areas last decade, be the same areas of high demand this decade? Well, no. The desirable cities in Florida are either geographically limited in suitable land for construction, or they are significantly behind demand. You will remember that in 2020 there were significant supply chain and cost disruptions for building materials. So builders have been perpetually 6-12 months behind demand, and the locations where property are now demanded (leisure and low taxes/expenses) are now seeing a significant imbalance in people trying to live there and homes available for rent, while the amount of construction companies, and capacity for throughput of materials has not adjusted yet to match this demand. Not a lot of additional construction capacity has been added to Big Sky, Montana even though demand for construction has gone up 3x its pre-pandemic levels.

This imbalance in demand is driving prices up significantly in desirable areas. It will likely be half a decade or more until supply can catch up… if ever. Many areas may see their real estate situation come to resemble California’s.

Consider especially the plight of area’s that previously would have mainly only been tourist areas. A significant portion of the work-force has permanently shifted to remote work. In 2020, no one was sure how long this would last or if it would be permanent, but by this point, just about everyone knows if they are going to work remotely or not for the next decade or more and so are making real estate choices based on that. What were previously sleepy mountain towns with a small permanent population and 5-6x as many tourists during the winters and summers are now finding that they are having an influx of people moving there who’s employers may be a thousand miles away. It’s so dire that some towns in Montana are finding that less than 1% of rental properties are vacant at any given time. For reference, 4% is considered healthy. This same phenomenon is occurring in beach towns as well. Simply, there are not enough homes in the places people have very recently decided they wish to live in.

5. Will Real Estate Crash?

This is a contentious question. My belief is that no, it will not. Many times people try to understand the next recession/crash by looking at the last one and trying to fit events from the previous one on to the next one. There are many people that have been sitting on the sidelines with cash waiting for a real estate crash because they have plans of “what I would have done in 2010,” and they want to enact their perfect strategy. You will always lose if you are using 10 year old tactics. In the 2000’s there was an over-production of real estate in excess of real demand and so as the decade moved along and financing costs dropped due to Alan Greenspan (then chairman of the federal reserve) cutting overnight lending rates down to 1% from 6.5% after 9/11 the ability of people to finance homes increased significantly for the first time. People’s behavior changed significantly because of this. Each subsequent year there was more money chasing real estate than the previous and so such behavior as flipping homes (and even flipping them without paying the sales tax by floating the title) became the norm. Similarly banks kept expanding the pool of people they were willing to lend to because this was such a large growth sector in financial services during that decade. Similarly, builders kept ramping up construction because there was significant demand and appreciation, they were regularly exceeding their profit models and so kept expanding their constructions.

Eventually the markets hit an inflection point where quite a lot of people ended up having to hold homes they didn’t actually want. Specifically builders that couldn’t sell, but needed to. Flippers stuck in a home they couldn’t move for a profit. Banks having to foreclose on properties they had lent out to people who couldn’t really afford the loan. The crash occurred because there was an over-supply and no one really wanted to come in and buy that over-supply quickly.

Is that whats happening now? No, not even close. As I’ve shown you here and in Section 4, we have the exact opposite problem. There are not enough homes in any of the places people want to live in. So how would housing crash? It can’t. It won’t. And in fact, the main thesis of this substack is one of the dollar continuing to inflate significantly. If you are looking to buy a home, I wouldn’t be sitting on the sidelines with an expectation that prices will come to you. They won’t unless you are trying to move in to an area that is significantly undesirable.

The only thing that could stop this is if lending rates continue to rise significantly. But, again as covered in this substack, the US treasury can’t afford to allow lending rates to appreciate significantly, and so they will pressure the Fed to intervene before the treasury defaults, which means that mortgage rates will never be allowed to rise high enough to constrain housing price appreciation. I would be surprised if at the end of the summer, the Federal Reserve hasn’t returned back to buying Mortgage backed securities like they have been since 2019.

6. Should You Buy Real Estate?

This is a question I see people posing often when we are discussing counter-inflationary investment strategies. Will real estate appreciate in an inflationary environment? Yes. That part of the question isn’t complex. The part of the question that gets complex is centered around “will holding real estate be profitable?” As you may have deduced from section 3, the cost increases of holding real estate are mainly borne by those holding rental properties. A significant consideration for real estate needs to be centered around whether or not it will be your primary residence or not. Owning your the home you live in does 3 things. The first is it stops your monthly expenses from going up as fast as they do when you rent. The 2nd is that you retain a portion of your monthly expenses on shelter as equity you can get back when selling your home. The 3rd is your equity appreciates above your contributions so long as inflation is occurring.

But owning the home you live in isn’t where the debate about real estate lies. Currently, many people believe that owning rental properties is a path to wealth, and over the past 30 years it did alright, but looking forwards into the future we have to consider many risks at the political and regulatory level. The current political landscape could very easily lead to additional taxes on rental properties, take a look at the changes made to Singapore’s property tax for fiscal year 2022 below. You will note that they raised the tax rate on non-owner occupied property.

The current tax regime can always change. Let me repeat that again. The current Tax Regime can always change. If you’re going to make a 10, 20, or 30 year investment, you need to make 30 year considerations into the future. You can’t reasonably invest in an IRA if you haven’t reasonably considered the possibility of the tax advantaged nature of the account being changed by the time you are 55. Similarly, you can’t reasonably decide to become a landlord if you have not thought of the possibility of a separate landlord tax being enacted. The political will and the ire that is currently being generated by large financial entities like Blackrock could easily result in populist pushes for additional taxes on landlords. It’s an easy move for a politician to make. Likely 90% of their constituents would support such a move, especially as rents rise. Such a tax would only raise rents higher, but that’s inconsequential, all that matters is that the risk is there. Such taxes only make it harder to stay in business, especially if you own only a half dozen properties or less. Large entities can more easily absorb the taxes than you can. I would posit that rental property is less likely to be a path to wealth in the future than it was in the past. While owning your primary residence is going to be paramount moving forward as the real estate markets will only become more supply restrained than they already are. The trends outlined in Section 4 will only continue to exacerbate.

6. Conclusion

Rents up across the board.

Mainly felt in areas that work from home is allowing more people to move to than previously.

Supply of properties in these areas is constrained.

State budget constraints due to CovID have led to more states, counties, and cities needing more tax income. Property taxes on rental properties tend to rise the most, this is passed on to renters.

If you can, you should make an effort to own your primary residence.

Owning rental property is a questionably risky proposition looking forwards into the potential future tax regime and towards potentially populist political trends.

An incoming crash in housing prices is unlikely.

7. Instagram Responses

Keep in mind, that these are semi-anonymous responses to a question I put out on my instagram page. Take them with a grain of salt, but also consider that when you hear the same or a similar story from people, it is unlikely they all decided to agree on the same lie. I wouldn’t feel too comfortable quoting any of these numbers to someone else, but I would feel comfortable saying that its likely that many people are feeling a fairly decent increase in their rent this year.

I agree with your assessments above.

Real estate (rentals) used to be an asset class to build wealth. In the current environment it has changed to an asset class to preserve wealth.

If you have income from other sources (W2 or business) real estate is one of the best tax shelters.

There is one other subtly about real estate that most people leave out. In the current (inflationary) environment the real estate (actual building) has become the liability while the debt is the asset. The debt serves as a fixed rate, non callable, dollar short when you are borrowing below the rate of inflation. Many times the actual rental is just breaking even but your debt is melting away as the government prints.

What source did you use for getting the tax info? I'm working on making a similar spreadsheet.