As some of you may have deduced from Instagram, I have been snowboarding for the past two weeks while Silicon Valley Bank, Silvergate, and several others crashed/collapsed.

Nero played his lute.

Basically me the last 2 weeks

More contagion continues to occur this week and the US Federal Government after fully backstopping deposits at SVB has decided to commit an additional undisclosed amount to backstop the markets (estimates are for ~$2 trillion).

We’re going to cover the existing problem from the frame of things I’ve already said here over the last year+, and then get into what you can expect moving forward.

Table of Contents

The Treasury Problem

Mark to Market

Work shouldn’t be fun

A Joke of a Stress Test

A new Lending Desk

$2 trillion of Added Liquidity

Conclusion

Internal References

1. The Treasury Problem

Often, people look for guidance in times of crisis. I have none. I provide guidance for what you should be doing when times are good. Do you want advice for right now? Too bad, there is no good advice, and people trying to tell you what you need to do right now are more than likely just selling you something to capitalize on your fear. Your nutritionist can’t solve your kidney failure. Let me rephrase… your nutritionist can solve your kidney failure… but he doesn’t want to. He wants you to eat right, and avoid boozing too hard so that your regular check-in is simple and stress-free. He wants to go home at 4:15 pm. He doesn’t want emergency calls at 11:30 pm when you’ve checked in to the ER because your bowels have become immotile, and the blockage is causing tearing and sepsis.

If you’ve been more or less following the advice on here:

You have a larger nut of cash saved to deploy into risk assets for the point of liftoff when the Fed is forced to inject liquidity into the treasury bond markets.

You might not have these notes exactly lined up in your head, but you should be close to this mentally even if you couldn’t fully execute. It’s the safest strategy. The DCA means that you already have exposure and don’t have to scramble because you’re worried you’ve missed the bottom. Being aware of the double bottom means you knew you would get at least two swipes into the teens (bitcoin price). And having a larger nut of cash means you can feel like you’re doing something when the market begins to take off.

As discussed numerous times, trading is an emotional game first, and a logical game second. If you don’t have your emotions handled, they will control the logic, and you will be in the passenger seat for even obvious moves.

At same time, 10-year U.S. Treasury bonds – the benchmark of global borrowing markets and traditional go-to asset in troubled times – have had their worst first half since 1788.

This stat already sounds amazing at a passing glance, but if you look deeper into American history and governance at that time you can see just how significantly bad this year is. The US declared independence in 1776, but the constitution wasn’t officially ratified by all states until 1788, and George Washington did not become president until 1789. Prior to that, the US acted as a confederation with each state acting essentially as its own de-facto country. In 1788 the US Treasury was run by 1 guy who was chosen because he was a half-decent merchant who could procure funds on short notice, and he had a staff of only3 people helping him.

In 1788, this guy was the entire US Treasury

For the first 12 years of its independence, the US governments finance’s were basically non-existent as no one really tried to pay off the revolutionary debt and the continental dollar devalued 500 to 1 against hard currencies. Looking back historically when comparing a treasury market there is basically a wall at 1788, we will never have a worse year than that unless we go full Venezuela into hyper-inflation. Essentially, this will be the worst year for US treasuries ever, because I don’t even count 1776-1788 as a functioning treasury market. At that point we basically wrote IOU’s in crayon and handed them out until Alexander Hamilton decided we needed to put away childish things.

If you’re new here, you have a lot of reading to do to catch up in the back catalog, but considering that last year was the worst-performing year of US treasuries ever, we have to consider the knock-on effects this had on financial institutions.

As I’ve stated here many times before, banks and financial institutions hold a portion of their cash savings in US treasuries. From the point of view of regulators, these assets are considered to be cash equivalents as everyone presumes that the US government is good for their obligations. At the shorter end of the curve (3 months or shorter maturity dates), these are considered to be worth their face value because you don’t have to wait very long for them to be redeemable.

The same trend that has been occurring every single month this year (except May) occurred again. Every single entity that bid into the treasury auctions ended up significantly upside down by the time the treasuries were issued. They can’t sell these into the secondary market for profit, and if the Fed did indeed start selling their balance sheet into the secondary markets as well it will make for an incredibly disappointing experience for any entity that did not plan on holding treasuries until maturity.

This leads us to the important concept that is occurring.

2. Mark to Market

As interest rates were rising all of last year, we were tracking the issuances compared to the secondary markets. That trend was that every single market participant in the treasury auctions was upside down on those positions essentially forever. This is what happened to Silicon Valley Bank, Silvergate, and several other entities that probably could have used an autist like me on staff (I’m not for sale, lol).

As I stated numerous times last year, if you buy a treasury bond that is worth $102, for $100, you are buying it at an interest rate of 2%. If market yields rise to 4%, you can’t sell that bond for the $100 you paid for it, nor can you sell it for the $102 face value it has. You have to sell it for ~$98. Why? Well anyone who wants yield on the market can get 4%, so you have to offer a competitive yield, otherwise, no one is buying your bonds on the secondary market.

Anyone with half a brain could predict the rising interest rate environment was coming and that doing something like putting $100 billion into 10-year treasury bonds at 1.95% would put a financial entity at significant risk. Hell, that’s the general thesis for why this substack was started and what we’re tracking. With rates pushing up to 5%, that $100 billion is now worth $97 billion. The genius that thought he was earning his bank $2 billion in interest just put a hole in his bank’s finances that is large enough to cause a few people to seriously consider jumping out of windows once they get the news.

Why is Getty making stock images for this?

This is easily preventable and easily predictable.

Usually, when financial entities make mistakes like this, they just pretend it didn’t happen, hold the asset to maturity and look the other way while hoping rates come down at some point in the future. This occurs more often than you’d expect.

But sometimes there is not enough cushion in the financial models of large entities for them to just ignore assets on their balance sheets. Sometimes financial entities need to shore up cash because they’ve mismanaged several things at once, and have to acquire enough liquid cash to cover their cash needs.

When this occurs they have to sell off assets. This is where problems arise. You never lose any money until you sell, so the solution, when upside down on treasuries is just to not sell and pretend they don’t exist. But if you’re forced to sell, suddenly you have to realize that loss. Be mindful of the following sentence.

The financial institutions that have “collapsed” are just the ones that were forced to sell, everyone is holding toxic treasury debt so long as rates keep rising.

A financial entity that has not accounted for losing a significant chunk of money being forced to do so in a moment when they are already in distress is likely done for. When an entity has to realize a loss, it has to re-adjust its own books and financial models. If too much of your holdings are exposed to long-term maturities, this can create a significant discrepancy between the face value (how much it’s worth when it matures) and its market value (what you can sell it for today).

A junior-level treasurer or financial controller should be able to mitigate these risks with basic GAAP (Generally Acceptable Accounting Principles) by keeping an appropriate ratio of their assets in short-term and liquid form. But Silicon Valley Bank did not hire anyone with any significant accounting background and had no risk management officer for the majority of 2022, only hiring one in January of this year. You can take a look at how much hiring they did for LGBTQIA+ and DEI though.

Cart before the horse

There are two ways to account for assets with long-term maturities.

Face value - You account for them at their value when they mature (Your $100 billion investment is worth $102 billion)

Mark to Market - You account for than at whatever their current sale value is (Your $100 billion investment is worth $97 billion and falling)

I imagine it must have been quite a shock for SVB to be informed by their newest January hire that they have a $5 billion hole in their books that is growing. Presumably, this is what led to their plan to do a capital raise of $2.25 billion by selling stock last week. I assume that amount would have covered enough of the hole for them to continue operations. Of course, the capital raise failed because that’s not how you raise capital. You raise capital by telling a story and promising a return. Not by telling people you have a hole in your balance sheet. There’s no promise of return there and the only investors were likely people who probably have strengths in a field other than finance.

3. Work Shouldn’t be Fun

I don’t mean this literally, I had a lot of fun at my first serious job.

But looking at the internal presentations and documents from SVB reminds me of my last serious job. I remember receiving emails about Hip Hop History month, it wasn’t quite the last straw, but it was right about here when I put my 6 weeks’ notice in to quit.

The discussion was atrocious. I wasn’t allowed to talk about any music more recent than 20 years ago, and it was a complete cringe. Vulgarity was essentially off the table. Most large corporations fail because they have a fake culture and no work gets done. You’re not allowed to actually be a person, just a caricature of one. If you’re lucky, you’re one of the chosen few who already have an identity that is within the allowable bounds of corporate pop culture. You get to bring your whole self to work. Everybody else has to self-censor, hide, and mitigate their true self, while you pretend to have liberated the drones.

Fake jobs encourage fake people to do fake work.

My first serious job was at an office of 10 people. There were 2 of us in development (myself and my boss), 2 in operations, 5 in finance, and our CEO.

We got a lot done. We were vulgar. We were sexist. We were racist. We were homophobic. None of us agreed with each other on anything related to politics. It was great.

This was my first office

When we built and sold our largest wind farm and made our parent company nearly $200m on a $20m budget by flipping a joint venture to a green VC fund we got drunk in the office at 9 am and then flew to the project site where we cut the ribbon and then drove a party bus around a town of 8,000 people buying all of the locals drinks at each bar until our treasurer and one of our construction contractors got in a competition to see who could punch each other in the stomach the hardest. The CFO for the VC fund we JVed with was drunk enough to think he could join in and ended up throwing up all over the bar after the first punch.

I had more hair back then

We had fun doing work and making money.

We were actually free to bring our whole selves to work. You could say whatever you wanted. There were no stultifying rules about office behavior outside of crimes. The woman in charge of HR cursed more than I did. All of our hires did something directly tangible towards making money.

We didn’t have to have an office committee about hip-hop awareness month. Instead on a random Tuesday our CEO would buy us pizza and then tell us why we all had shit taste in music for 45 minutes, and we were free to argue with him.

I compare that to my next job and we see a lot of parallels with SVB. I worked in an office of over 700 people and we were only about 5x more productive than my first office with 10 employees. I remember my first 3 months there. I originally was trying to do so much, while endless committees, approvals, working groups, and request forms got in the way, I eventually just gave up. If you wanted to do 2 hours of productive work, it required several hours of unproductive work to approve it.

You combine nonsense like Cringe-Hop History month, and our endless DE&I hires with the fact that my department refused to hire another actual developer for the entire west coast (yes, I was responsible for half of the country), nor a procurement manager (yes, I was responsible for this on top of my actual job) and you can see why I got fed up. When we needed work to get done, they didn’t hire productive employees and just piled the extra work on to me and the other few people doing work, while the army of useless breathers I had to fight through to get work done continued to grow. But they had entire teams of people supporting whatever that week’s diversity initiative was.

Work should not be fun. Its primary purpose isn’t to be fun. The primary purpose of work is to make money as easily as possible, fun is a natural side effect of doing that. You can’t force culture, you can’t force fun. It happens all on its own when you let productive people be productive.

The failures of SVB look all too familiar to me. This was a company that ignored productivity and general financial and accounting practices because they thought they could make work fun. I’m not Nostradamus. None of the content on this substack is revelatory to anyone worth their salt in any semi-financial industry. You are watching elementary-level mistakes being made across the globe by corporations trying to force fun for the whiniest group of employees at the detriment of productivity.

4. A Joke of a Stress Test

So, this mistake was one that should have been fairly predictable right? If I (an autist in his pajamas) could identify it as a problem coming before interest rates even lifted off from zero, where were the authorities?

You will also note that the stress test does not include any sort of stagflationary scenario (like one where inflation remained high while asset prices dragged down as bond and lending spreads widen significantly).

The most predictable negative outcome was not tested for by the Federal Reserve when they stress-tested the banks.

This unfortunately means that any analyst working for the Fed who simply depends on the work of others to determine risk would have really had no clue that this sort of collapse was imminent. I have no doubt that a few autists work at the Federal Reserve and probably had their own private opinions/suspicions, but they would have had no official data they could point to due to a failure of imagination when the parameters for the stress test were formed.

Okay, so the federal reserve failed, but what about the Congressional Budget Office?

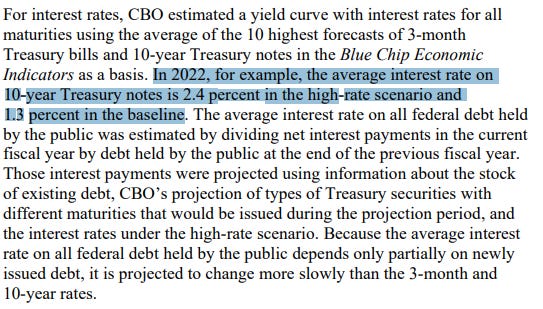

The CBO (Congressional Budget Office) and the treasury have not forecasted for this scenario at all. I am going to share a letter written by the CBO just last month about net interest payments on the national debt. Take note, that they made estimates for how high interest rates for the 10 year treasury would get to make estimates on the interest payments the treasury would pay.

1.3% interest was the baseline they expected to pay. With a “high-rate scenario” being 2.4%. Again, this was written last month. This month already the 10-year treasury auction concluded for 2.72%, and rates are not done rising.

In March of last year, they predicted that the 10-year treasury rate would remain ~1.3% in an average scenario and 2.4% in a “high-rate scenario.” I had trouble understanding how they could even come to predict that in a serious manner back then. Looking back now it’s even more incredulous to me, but congress isn’t exactly a place for people with significant financial chops to go. It’s more of where they go to die. So neither congress nor the Federal Reserve had this scenario on their radar (officially). Unofficially, I suspect the Federal Reserve has been acutely aware this is impending and has been just hoping that inflation would go down and treasury markets would normalize before too much damage was done.

The bleakness of the truth has always been that solving this problem lies outside of the hands of the Federal Reserve. But they can’t tell you that for the same reason that the captain can’t run to the lifeboats once, it’s clear to him that the ship will sink.

They instead pretend each financial epoch is going fine until the turmoil can’t be covered up anymore, and then the next financial epoch starts. We’re nearing the end of this one.

5. A New Lending Desk

You’ve probably seen a lot of people tossing the following phrase around.

$2 trillion of Added Liquidity

They are claiming that the Federal Reserve is injecting $2 trillion into the markets to backstop pending bank failures.

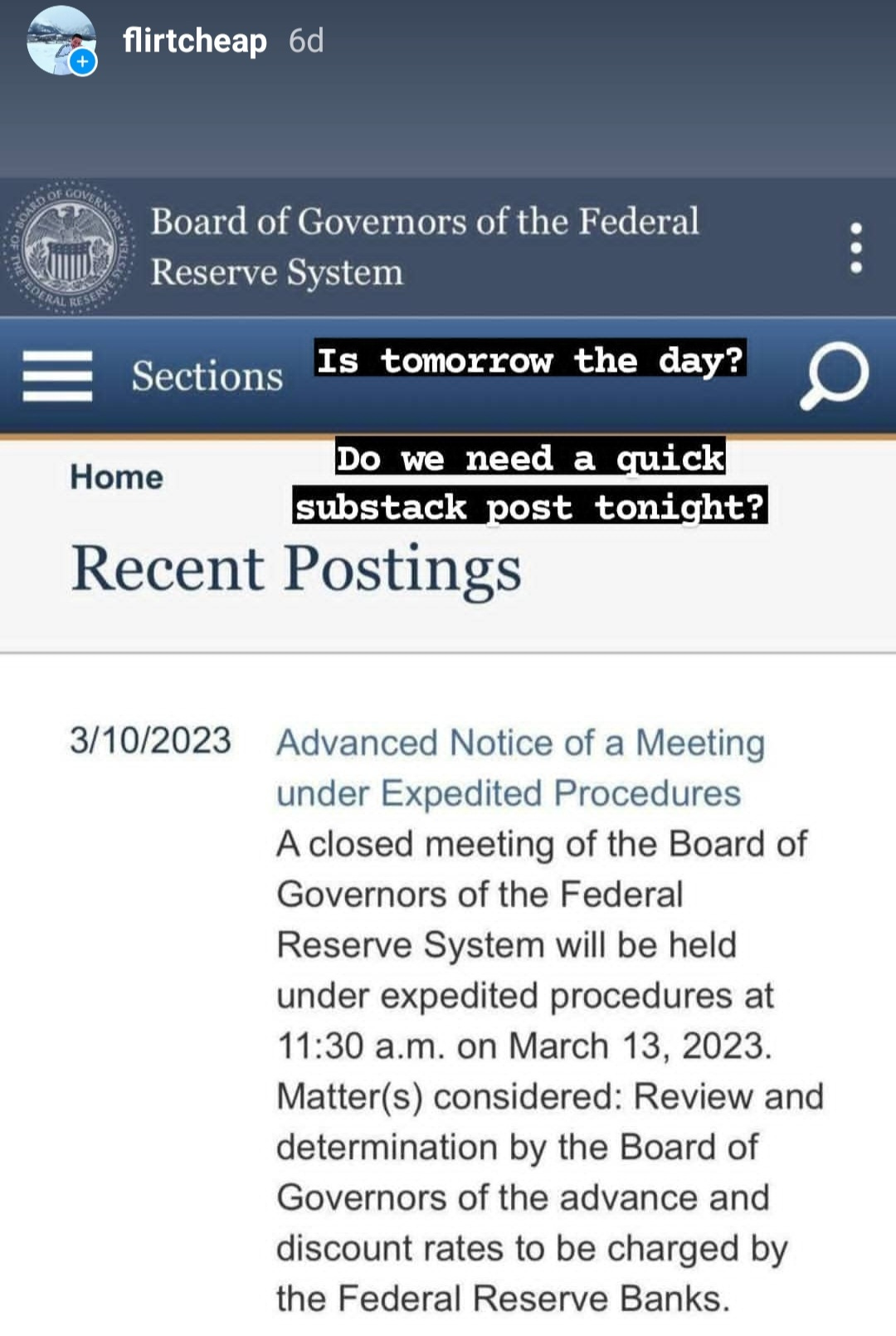

Not quite. As usual, most people lack the context to be able to properly explain what is going on. Late on Friday afternoon, the Federal Reserve added an unscheduled meeting to its calendar. I posted it quickly on IG and hinted that I would be making a substack post about it soon. I had hoped I could do it that night, but I spent ~2.5 hours creeping through Loveland pass in a front-wheel drive rental car while 7 inches of snow fell, and I didn’t return to town until far too late to be productive.

In any given year, there are a few unscheduled federal reserve meetings (rarely more than 2 or 3). They typically point to only a few possible things. Emergency changes to the overnight lending rate, to the reverse repo facilities, or the opening/closing of an emergency trading desk/facility for financial entities to use.

The Federal Reserve has not put a cap on the amount of capital that can flow through this lending desk.

offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution's need to quickly sell those securities in times of stress.

Essentially every bank that failed to adequately prepare for a wholly predictable scenario in any reasonable manner can now swap their dumb treasury purchases at face value rather than market value to the Federal Reserve for the next year if they find themselves needing cash.

US 3-year treasury yield

As you can see in the chart above, now that treasuries can essentially be traded for free money (you get interest now rather than in the future) a number of institutions rushed to buy treasuries and yields fell back down rapidly.

So, where does the $2 trillion figure come from?

JPMorgan.

The Fed did not provide a figure for how much this facility could inject into the markets over the year it will be open, but they did say it was large enough to cover all uninsured deposits in the US.

How many uninsured deposits exist?

Roughly $7 trillion.

But of course, not all of that is represented by treasuries, mortgage-backed securities, and corporate bonds. And not all financial institutions will use the facility just because it’s opened. JPMorgan made an estimate that $2 trillion will be the actual figure that gets injected into the markets.

We have no way of knowing what the actual number is, and of course, the incentive exists for institutions to simply buy treasury bonds to use the facility without actually having any need for the facility. Regardless, it will serve to push interest rates down.

If you’ve learned anything from these past 18 months on here, you should have learned this. When interest rates get pushed down, asset prices get pushed up.

Buy bitcoin, buy Ethereum.

6. Conclusion

This isn’t exactly a pivot, but it marks the change in trend toward a pivot. The Federal Reserve meets next week to discuss interest rates. They will be between a rock and hard place in this coming meeting. Even something like pausing the rate hikes will be seen as a pivot by the markets. While sensing a pivot will cause traders to take some of the burden off of Powell’s back by front-running the trade and buying treasuries, it may anger many Americans who would view it as a surrender in the fight against inflation.

But to us it’s irrelevant. At this point, it’s time to look for opportunities to toss your nut into the ring. You should keep DCAing of course, but if you had a larger stock of liquid cash set aside to invest, this will likely present a relatively safe time to enter. Giving price guidance at this particular point will be a bit difficult as BTC price is currently in the No-mans land area for price action that I outlined last summer. But 9 months from now it will hardly matter so long as you entered.

Just as in March of 2020, we saw numerous trading and swap desks opened to plug the hole in market liquidity stemming from the September 2019 contagion emanating from the Reverse Repo Markets. The last one to open was what set the bottom. But there are a bunch of traders watching right now who also learned the same lesson back in 2020, so we have to be even more prudent about timing because you never get the same market twice.

Buy Bitcoin. Buy Ethereum.

7. Internal References

If you’re new and have a question, please read the FAQ post first.

I couldn't agree more with your points on office culture and productivity.

In my first real job I worked for a major retailer, but was lucky enough to land in a group of rebels to the office norm. Our group of about 30 generated 35% of revenue compared to the 200+ others in similar functions. We were competitive, crass, but damn we worked hard. All the things you said above applied to us. I still have a word doc of all the one liners from one of the old heads..."how's your wife and my kids?" "you're a year away from being a good analyst, next year it'll be 2!" and on. The entire time we grew and killed our goals regardless of the rest of the industry even.

And on the flip side every year brought a new "big idea" forced down on us by consultants or hairbrained schemes from other product categories that never hit a number in their life and after a while the deadweight was too much to carry and we got bought out. The core group scattered to the winds and what was left was sanitized and crippled compared to what we had accomplished.

Sorry to just reminisce here...just wanted to say you're spot on and in my experience very few people are lucky enough to have ever experienced a truly productive setting like you describe. And after they do, the blinders come off and it's plain to see how many unproductive people are in the world.

1) Is this essentially ending Quantitative Tightening efforts? Essentially a sneaky way to print money without the general public realizing?

2) Should we still be watching the treasury markets like before? Or does this change the equation to a possible big jump in, now that the feds are *Sort of maybe* infusing new large amounts of money?

*Essentially*, how does this affect our original action plan and should we adjust the previous "tells" and plans due to the “Bank Term Funding Program", or should we generally stay the course?

It was my understanding that we were waiting out some important factors I won't belabor here as you know them. However, this seems like a monkey wrench.

Would this be a good time to write a "where we're at now" post, with potential action steps and new levers... just so we can be super clear about what our options are when it comes to US financial markets mainly?

I couldn't agree more with your points on office culture and productivity.

In my first real job I worked for a major retailer, but was lucky enough to land in a group of rebels to the office norm. Our group of about 30 generated 35% of revenue compared to the 200+ others in similar functions. We were competitive, crass, but damn we worked hard. All the things you said above applied to us. I still have a word doc of all the one liners from one of the old heads..."how's your wife and my kids?" "you're a year away from being a good analyst, next year it'll be 2!" and on. The entire time we grew and killed our goals regardless of the rest of the industry even.

And on the flip side every year brought a new "big idea" forced down on us by consultants or hairbrained schemes from other product categories that never hit a number in their life and after a while the deadweight was too much to carry and we got bought out. The core group scattered to the winds and what was left was sanitized and crippled compared to what we had accomplished.

Sorry to just reminisce here...just wanted to say you're spot on and in my experience very few people are lucky enough to have ever experienced a truly productive setting like you describe. And after they do, the blinders come off and it's plain to see how many unproductive people are in the world.

A few important questions:

1) Is this essentially ending Quantitative Tightening efforts? Essentially a sneaky way to print money without the general public realizing?

2) Should we still be watching the treasury markets like before? Or does this change the equation to a possible big jump in, now that the feds are *Sort of maybe* infusing new large amounts of money?

*Essentially*, how does this affect our original action plan and should we adjust the previous "tells" and plans due to the “Bank Term Funding Program", or should we generally stay the course?

It was my understanding that we were waiting out some important factors I won't belabor here as you know them. However, this seems like a monkey wrench.

Would this be a good time to write a "where we're at now" post, with potential action steps and new levers... just so we can be super clear about what our options are when it comes to US financial markets mainly?

Thank you!