The Commercial Real Estate Bomb

The Commercial Real Estate Bomb

A walk through Tenderloin

Table of Contents

Commercial Real Estate Bomb

Balloon Payments and Mortgage Structure

The Case for Defaulting

Convert to Residential?

San Francisco Leads the Way

Should you be Concerned?

Conclusion

Internal References

1. Commercial Real Estate Bomb

Peter Schiff recently visited Yahoo’s offices in the UK and filmed the empty building for a reel on IG, I linked it in my IG story and got a few questions and comments regarding it so I figured today might be a decent day to jump into what’s still coming and some of the common questions people have about it.

In general commercial real estate loans are much shorter than residential real estate. If you own your home, you might have a 15-year or a 30-year mortgage. Considerations around refinancing that loan typically are only centered around affordability or the decision to pull equity out of the house.

However, in the commercial sector, refinancing is more common and is a typical way to run the business model because commercial real estate loans are structured in a completely different manner from your typical residential loan.

2. Balloon Payments and Mortgage Structure

The thing that makes commercial real estate mortgages different from residential is called a balloon payment. Typically commercial real estate has shorter terms than residential real estate, this isn’t achieved by having massively larger monthly payments to cover the principal of the loan sooner, this is instead achieved by having one large payment at the end of the loan. Sometimes the balloon payment can be as large as 85% of the loan.

The most common loan structure for commercial real estate is called a 5/25 mortgage.

In a 5/25 mortgage, the lender applies a 30-year amortization schedule, as if the homebuyer was taking out a conventional loan. However, the loan calls for either a balloon payment at the end of five years or the resetting of the loan. Thus, a 5/25 mortgage has a five-year term but a 30-year amortization schedule.

Essentially, at the end of the 5th year, you make a lump sum payment to cover the remaining balance of what would have been a 30-year mortgage, OR you refinance and start the structure again but with a slightly smaller principal.

This type of structure has worked fine for most commercial real estate because rates have spent the last ~30 years going down with a handful of exceptions. Meaning that every time you refinance, you are getting more favorable loan terms. At the same time this has been happening, most commercial real estate has been getting more profitable and maintaining higher valuations. It’s been a fairly good sector to be in for the last several decades.

3. The Case for Defaulting

However, that has all changed in the last 3 and a half years. You’re all well aware that many employers have switched to remote work, and that quite a bit of layoffs and offshoring of white-collar labor has occurred in the US. And at the same time, overnight lending rates are up from 0.25% to 5.25% in just the last 18 months. This means that when those balloon payments come due, those who are unable to pay their balloon payments and would normally refinance, are now having to look into an uncertain future where they refinance with higher payments while not knowing where their income might come from.

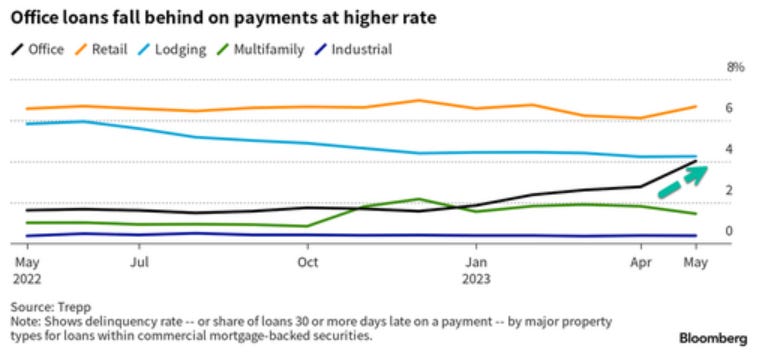

As you can see in the image above, we are starting to see an increasing trend of payments on commercial real estate specifically with office space falling more delinquent. A shift in the delinquency rate from 1.8% to 4% from December of last year to May of this year is a pretty big shift. But this is just the beginning of the pain for the commercial real estate sector as a whole.

Office space is the one type of commercial real estate that is least likely to recover from the CovID slump in terms of having a profitable cash flow in a rising interest rate environment.

While many retail businesses died during CovID, those that didn’t have seen a recovery in revenue from tourism, shopping, and consumer activity as the CovID restrictions continue to ease. If they raise their prices they may be able to survive with rising rents. Typically retail rents on 1-7 year leases depending on the size of the store (small storefronts have shorter lease terms). Commercial Real Estate set up for retail is unlikely to struggle too much.

The same trend is there for industrial, multifamily (apartments), and lodging. There may be some cities and areas that people have moved away from or where tourism has fallen permanently (we’ll explore one example in Section 5), but for the most part, these sectors can also raise rents/costs to deal with having higher lending costs in the future.

Office space is the one that simply can’t adjust to the new environment due to how many companies have gone remote, laid off employees, or offshored some of their white-collar labor force as we discussed would happen last year.

Large companies are still paying their leases for their office space, but when they reach the end of their leases, do you think they are going to renew to keep paying for empty office space? Some of the largest companies might be renting their office space on 7-8 year leases at the most. This is one reason the collapse is slow. If you have a client who is 4 years into a 7-year lease and they have left the space 2 years ago, you know that you’ll need a new tenant 3 years from now and you’ll hope to find a new tenant in the time between. But let’s say that your balloon payment is due in 2 years. When 2 years comes around, depending on the market for tenants and the interest rates being offered, you may have to make a tough decision.

Those tough decisions are exactly what we need to be looking out for the most. It’s why the expectation is for a long drawn-out turnover (multi-year) in these markets as properties get handed back to banks who can’t really afford to take them on.

It’s quite possible that we may see some genuine turnover of office real estate back to the banks in the coming years that is a direct result of interest rate phenomenon. Some of you may be saying, “But Flirtcheap, this is already happening, look at San Francisco!” We will take a look at San Francisco in Section 5, but to save you some of the suspense, San Francisco is just awful, they’re turning over hotels and malls (retail) back to the bank and they’re one of the few cities where that has spread to retail and lodging.

So far, the defaults we have seen this year of office space have been spread out mainly in Los Angeles, New York City, and Chicago. This makes sense as all 3 of these cities have rather dense office space, and many companies left these cities entirely on top of the other factors at play. We also saw $1.7 billion of office loan defaults in Boston, New Jersey, and San Francisco from PIMCO. These defaults are in line with what we can expect in the years to come, and later this year.

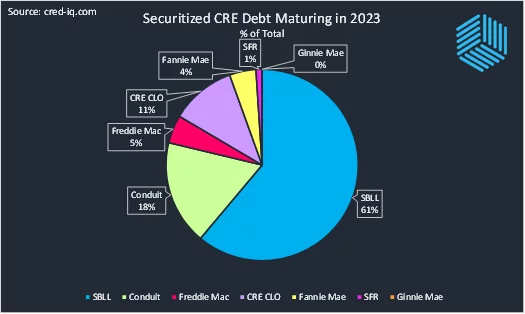

Taking a look at how much CRE matures(d) this year we can see about $160 billion, of which $100 billion is relevant to this discussion.

All of that has to be either refinanced, or they have to pay a massive balloon payment on it. But we aren’t the only ones aware of the risks. Lenders themselves are also aware of the risks and if they lend more money to the commercial real estate sector they are also increasing their exposure to it and they may be in a position where they can only take it on if the interest payments are sizable. This compounds the problem because there might be some properties that are on the edge of defaulting but would and could refinance at today’s rates, but they might not be able to find any lenders willing to do so because they are scared of the default risk. And those properties may end up defaulting simply because they have no choice.

$160 billion in 2023 is a minor problem and sure we see a few defaults, but it’s not that bad, but what does the outlook for the next 4 years look like? A Morgan Stanley Analyst has this to say.

More than half of the $2.9 trillion in commercial mortgages will be up for refinancing in the next couple of years. Even if current rates stay where they are, new lending rates are likely to be 3.5 to 4.5 percentage points higher than they are for many of CRE’s existing mortgages.

There is also another article that popped up around April of this year. It was copied and pasted across Bloomberg, NYPost, CNBC, and others as well as read aloud for several youtube videos. All of them also cite a Morgan Stanley analyst, however, I was unable to find any original source at Morgan Stanley saying this, but I’m going to share the article and the quote from it below with that caveat in mind.

nearly $1.5 trillion in debt is due for repayment by the end of 2025, according to analysts at investment banking giant Morgan Stanley.

Is that how much CRE debt will be coming due between now and 2025? I don’t know and found no confirmation that this was true. But whatever the number is, we can assume it is several hundred billion if not a trillion dollars. This year with only ~$160 billion maturing, we saw several large defaults already. I would expect that trend to increase in the future, but we don’t know just how large of an increase we can expect.

4. Convert to Residential?

In these discussions, you will often hear people saying “Why not convert the property for residential use?” On its face, this sounds smart, since residential multi-family real estate isn’t having the same sort of default rates, and as we discussed last year, rents are rising at a tremendously rapid pace in some areas, and we could benefit all around from such conversions.

The key problem is plumbing. Every office I’ve worked in has maybe 1 or 2 sets of bathrooms per floor. While a residence needs bathrooms, kitchens, and a laundry area all of which require venting and additional plumbing lines. To convert an office into a residential building, you have to totally tear out the inside of the building. In the video below you’ll note that the only things they kept of the original building were the stairwells and the elevator.

While not impossible this is incredibly labor-intensive and expensive. You need capital to do this, and if you’re already struggling to refinance or make a balloon payment it’s unlikely that you’ll have the capital prepared and have spent the time in development to do this.

Realistically, these conversions will happen after the properties default to the banks and then the banks turn around and sell them for pennies on the dollar. For people with a couple hundred million of capital ready to be deployed, this will likely be a significant opportunity to buy, strip the building down to its skeleton or less, convert it, and then sell a partial ownership share at a lower cap rate than what you came in at. The partial sale allows you to pull out a portion or all of your investment while retaining cash flow and equity.

I’d expect that the move to gobble up these properties will coincide with the Federal Reserve eventually bringing interest rates back down as at that point much of the liquidity that has moved into treasuries may start looking for the door and a new place to go.

5. San Francisco Leads the Way

As usual, San Francisco is having a far worse time than other cities in dealing with this problem.

Over the last two weeks, there have been a few major story pieces in the news about Commercial Real Estate in San Francisco being turned over to their lenders. There are two Hilton Hotels, and one 9-story mall that were all easier to turn over to the bank than they were to refinance or make the balloon payments on. What most stories don’t tell you is how close these pieces of property are to each other. Below is a screenshot from google maps. The blue boxes are the hotels, and the red is the mall.

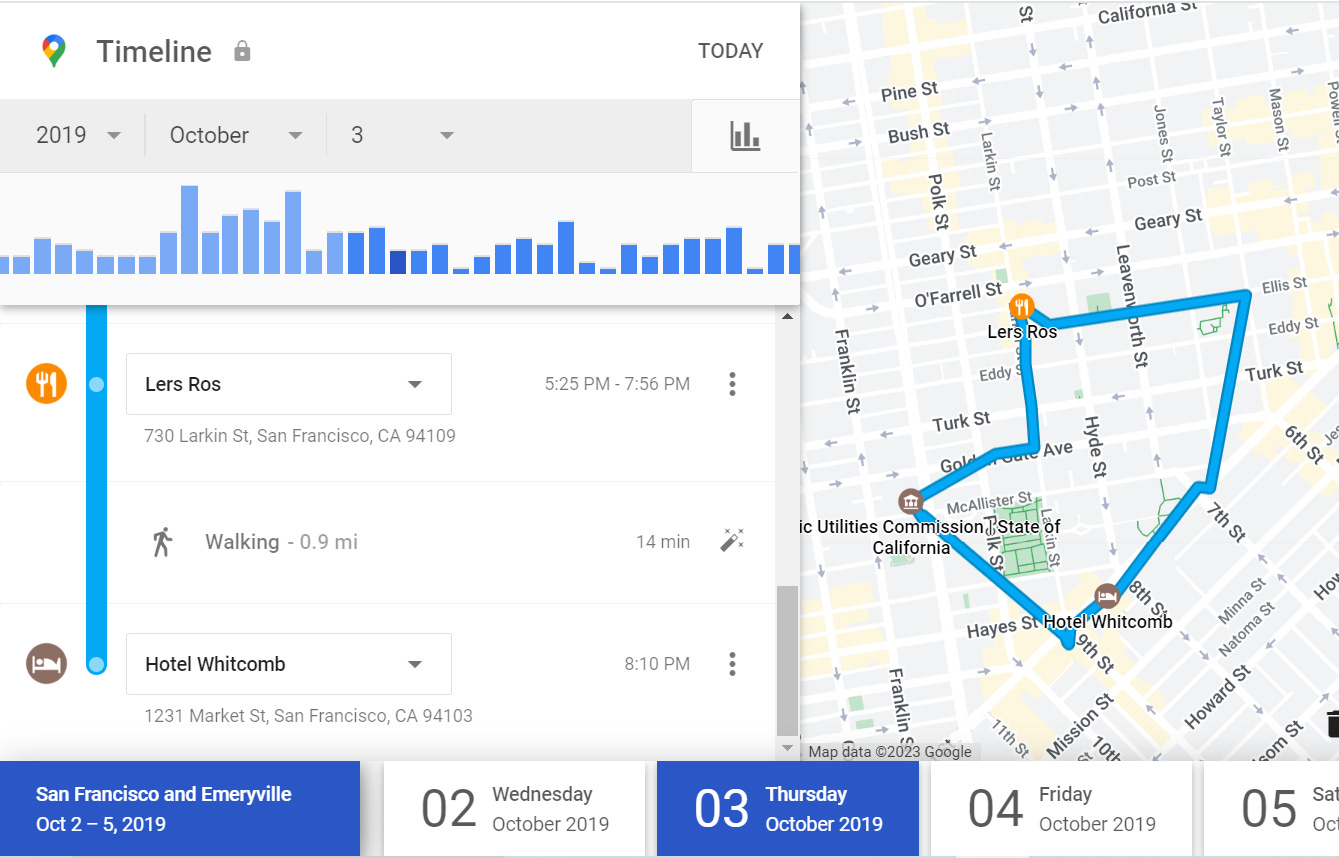

I was in San Francisco back in 2019, it was awful then and out of curiosity, I went to see how far I had been from this part of town. I was about 5 blocks SW of the area above. Below you can see a map of my day on October 3rd, 2019. I started at the California Public Utilities Commission at 10 am, and was there until 5:13 pm, then I walked to dinner with some of our project engineers. We had dinner until 7:56 pm, at which point I decided to walk the long way back to my hotel through the Tenderloin district.

I wanted to see it for myself and decided to take a walk through Tenderloin. It was awful. My walk back to the Hotel around 8 pm that night in October was full of sights that shouldn’t be in a first-world city. Feces on the street, both human and animal were common, as were discarded needles; strung-out junkies lined the sidewalks, a few cars on the street had broken windows and I even watched one man break into the back of an SUV to take a backpack out of the trunk right in front of me. I felt out of place in my suit and tie, but in truth, no one bothered me while I walked. They were in a world of their own.

If you look closely at the map of my walk, you’ll see that I turned right at the corner of one of the hotels that defaulted. At that point, I had had enough and it was still filthy. This blighted area of San Francisco has been spreading north-east into the fancier downtown and business districts and is likely chasing retailers and tourists out. It’s no wonder the 3 properties above defaulted.

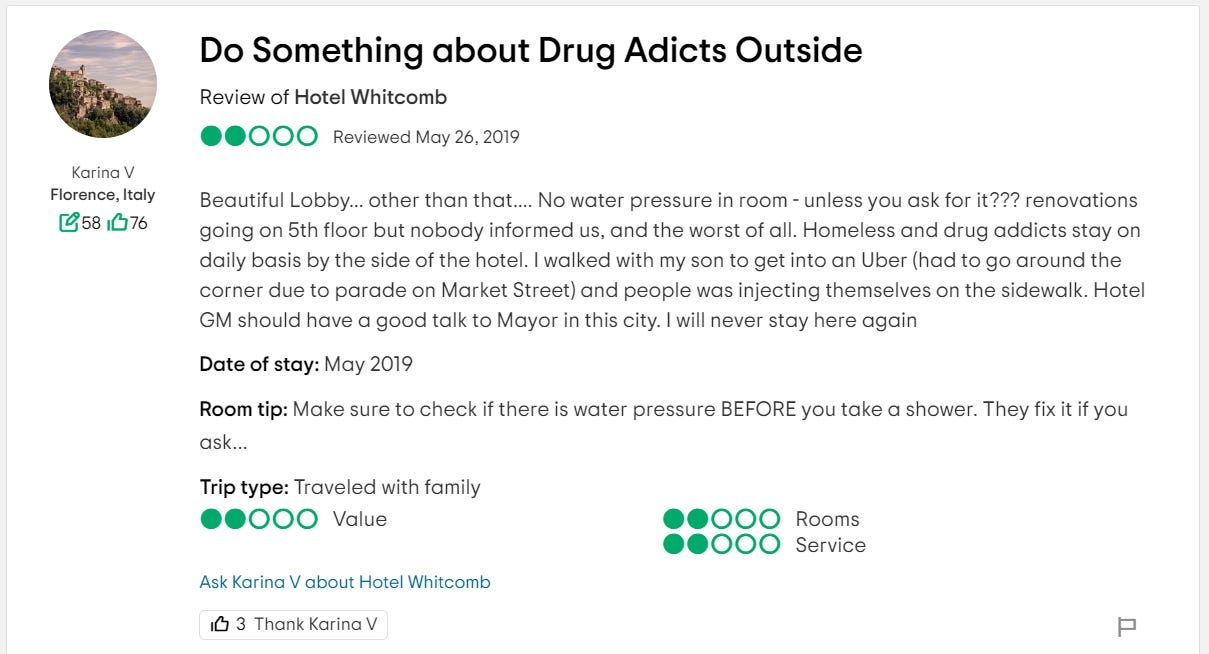

Out of curiosity, I wanted to see what was happening with the Hotel I had chosen for that trip back in 2019. The Hotel Whitcomb (I picked it because it was supposedly haunted, this is how I pick all hotels when traveling for work) was turned into a homeless shelter in March 2020 and was given federal funding to house the homeless during the pandemic. The hotel had to close down in 2022 when the federal funding lapsed, and the hotel has been shut down ever since.

It seems that the Hotel is suing the city of San Francisco for $19.5 million because while the program was ongoing, significant property damage was incurred from the homeless population that was well in excess of what the city paid to the hotel. On top of that, at least 18 people died of overdoses inside the hotel while they were being forced to shelter the homeless. You may note that one of the hotels turned over to the bank was also forced to shelter the homeless for the last two years.

It’s very easy to look at San Francisco and think we are seeing the start of a commercial real estate collapse. We are, and we are not. This part of San Francisco is a shithole. We’re seeing a reflection of city policy combined with a weak refinancing market resulting in the properties most damaged by city policy being defaulted on. Will this be happening in other cities? Not in the same fashion, but we likely have a while to wait before we see another distressed area emerge. San Francisco is just awful and we shouldn’t be looking at these instances as a sign of what’s to come in the rest of the US imminently. It’s quite possible that these properties would be getting defaulted on even if the Federal Funds rate was only at 2% instead of the 5.25% it’s at now.

It’s just an awful city that is not conducive to this kind of business. The problems it’s having probably go beyond the interest rate risk of the current environment. We will start to see some major stress in the commercial real estate sector, but what we’re seeing right now in San Francisco is not it. The city is just a garbage heap and that is reflected in the decisions made by businesses there.

6. Should you be Concerned

There are a couple of bad outcomes that will come of this. First, if your investment portfolio includes any REITs with significant US commercial office space exposure you are probably already feeling the pinch, but regardless, you should take a harder look at them and see what their primary holdings look like.

(REIT = Real Estate Investment Trust)

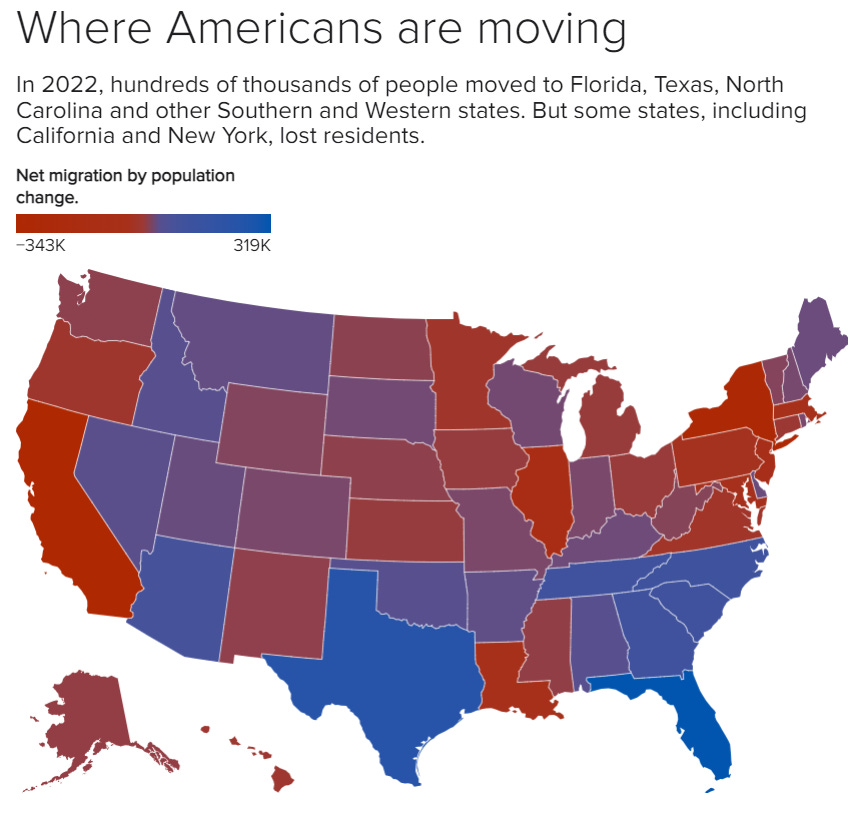

Like most things, this will be K-shaped as well.

The states Americans are moving away from will be the most impacted, while those they are moving to will be the least impacted. REITs focused on states with net migration outflows will be the most impacted, while REITs focused on states with net migration inflows will probably feel less pain.

I can’t tell you to blanket sell your REITs or to just open leveraged shorts on REITs randomly. That would be bad advice as each REIT holds specific exposure. You wouldn’t want to open a short on a REIT with a focus on commercial properties only to find out they mainly hold apartments in Tennessee. You need to look hard at your REIT exposure, see where and what type of property allocation they have, and decide from there.

The other major concern is one I outlined on Tuesday of this week regarding Powell’s testimony. How much stress does this put the US banking sector under if they have to take on properties that they are not prepared to handle?

What happens to the banking sector when a bank is forced to take on assets like these where they lent $725m with these 2 hotels as collateral? The hotels themselves have been renovated many times with nearly $100m spent on renovation in the last decade. How much is the property worth? The bank might have presumed they were worth over $700m when the loan was made, but how much is it actually worth? What happens if the bank has to take a $300m hit and sell these on a firesale just to get rid of the maintenance expense? What happens if this bank has several other loans for commercial real estate? SVB collapsed over a $2b mistake with treasury allocations. Who’s to say a bank focused on commercial real estate couldn’t find itself with a similar hole on its balance sheet over the next 2 years?

Do we see another potential banking collapse in the future? Maybe. Does the Federal Reserve have to open up a swap desk offering liquidity in exchange for CMBSs (Commercial Mortgage Backed Securities)? Maybe. Does Powell have more pressure put on him to cut rates or intervene in the banking sector in the future? Maybe.

If we had a competent Senate banking committee, we would see questions like this being asked of Powell tomorrow when he testifies. But instead, we’ll likely be seeing questions about diverse representation among the C-suite at US banks and how we can improve that. We live in a broken country in a number of ways. I don’t care who sits on the board of the bank, so long as it doesn’t fail and I can withdraw money whenever I want. If we lived in a Harry Potter universe where all of the bankers were long-nosed Goblins but your vault was full of gold coins whenever you showed up, I’d be happy.

But for whatever reason the Senate Banking Committee’s main concerns will be about which made-up gender will be in control of the made-up accounts that we all pretend still have money in them. Give me a competent goblin any day of the week.

Priorities.

7. Conclusion

Over the next 5 years, we will be watching commercial real estate defaults continue past those we’ve already seen this year. An estimated $1.5 trillion of commercial real estate mortgages will mature by the end of 2025. This is a problem because the CRE mortgage structure is typically in a 5/25 mortgage where the first 5 years have payments structured like a 30-year loan, and in year 6 a single balloon payment is due for the other 25 years. CRE usually refinances at this point but since interest rates have risen, this is no longer an option for them.

Instead, they will either have to default or make the payment, with many choosing to instead default. These properties will fall to the banks who will either sell them for pennies on the dollar or potentially board them up and let them rot.

If you have REIT exposure, you should be reviewing it for how much of it is US based and how much of it is office based as those are the primary areas of most risk, while other forms of commercial real estate will fare better. States with net migration inflows will also be safer than those where people are leaving.

8. Internal References

If you’re new and have a question, please read the FAQ post first.

If you wish to search through my entire substack, please refer to this guide post.

Please refer to the Definitions page for any terms or abbreviations that I use that you don’t understand. If a term is missing, please let me know.

The Substack app is out, consider using that instead of email or your browser.

Great post. I was waiting for you to drop the axe on lodging, but I am seeing no slow down in renovations or new construction from where is I sit.

Except in San Fran/Chicago/LA,NYC.

I have a feeling the quote "gradually, then suddenly" will be very apt for a lot of commercial real estate.

Regarding conversion to residential - another consideration is will people really even want to live there? If the office space is empty it's safe to say the jobs aren't located there anymore. If the jobs aren't physically located there, will people want to be? Plus the longer term knock-on effects, which are already in motion, of decline in businesses that relied on people filling up those offices most days.

My little hometown area has gone through several boom and busts from railroads & cattle drives to army depots and a corporate headquarters...the down turns are never quite what you expect.