Stagflation In the US

CPI still high, but assets down

If you’re new and have a question, please read the FAQ post first.

Please refer to Definitions page for any terms or abbreviations that I use that you don’t understand. If a term is missing, please let me know.

This post will be too long for the email, please come to the substack website.

Substack has launched an iOS app for those of you using apple devices. I am an android peasant and can’t tell you if its good or not yet, but I will know soon. Substack has announced a waitlist for their android app, which they claim is nearly ready. I’ve signed up for the waitlist and the link is here in case you wish to do so.

Table of Contents

August CPI

Market Reaction

Midwit Fear of Deflation

Stagflation

Conclusion

1. August CPI

Yesterday, the US received inflation data from the Bureau of Labor and Statistics. This inflation data was in the form of the CPI. The official release from the BLS is here.

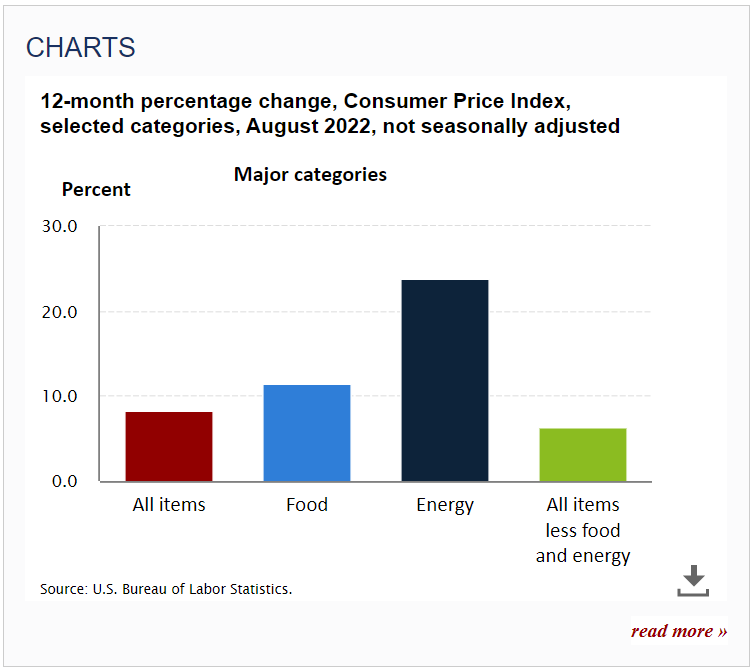

The CPI in August rose by 0.1% month over month, and 8.3% annually.

Despite the administrations best efforts to keep energy prices down by raiding the US Governments Strategic Petroleum reserve, prices are still on the uptrend in all other sectors. You can see the impacts that the sales of our last fuel reserves have highlighted below.

Food costs, as can be seen above, have been increasing by roughly 1% each month since February, and over the last 12 months are up. This is a familiar story of course, you’ve already heard all of this the last time we analyzed a CPI report. Not much is really changing since then except energy prices are briefly going down for as long as Democrats care to sell the US’s strategic petroleum reserve. Right now, they only plan to sell our oil until the week before the midterm elections.

Of course, the numbers in these reports are fake. We’ve covered that numerous times before, and last week we heard Powell explain to us how these statistics are useful in controlling the behavior of citizens. It’s quite likely that the real numbers are much higher than as they are presented to us. But you probably know that already. So rather than spending too much time discussing the report and whats in it, we’re going to talk about how and why the markets reacted the way they did, and how this relates to the overall macro thesis of this substack.

2. Market Reaction

As you all probably know by now, there was a rather large market sell-off after the CPI print on Tuesday.

The question people usually ask is, if all of these assets are counter-inflationary, then why are they going down when we get a higher than expected inflation report? Well, you need to remember some of the things discussed last year in the backdrop post.

Being right, when everyone else is wrong, looks the exact same as being wrong.

If you try to trade the truth on the short term, you will get burned, you want to be trading what it is the market is going to do. You want to know what they will hear, how they will interpret it, and how they will trade. That is far more important than knowing what is true and making fundamentally perfect trades.

The markets are trading with an expectation that the Federal Reserve will succeed in their tightening cycle. The market is not trading with an expectation of long term sustained inflation that the Fed is incapable of beating. The market expects Federal Reserve Rate hikes and QT to occur in a vacuum. Essentially the markets are only trading first order effects while ignoring second order effects.

When taken at their word we can presume that the Federal Reserve’s goal is to primarily fight inflation, and that they intend to keep raising rates until inflation has been beaten down to below 2%. A large contingent of the market (both dumb and smart) stop their considerations here. Yes, a very large contingent of the market is simply making bets on what the Fed will do, and not on both what the Fed will do, and what is possible. Dumb market participants are doing this, and smart market participants are simply trading their expectations of what dumb money will do.

So we see the following behavior (and this is what determines the macro). Any news that increases the chance the Fed will raise rates at future meetings (even though treasuries are mostly divorced from the overnight Fed funds rate) will push asset prices down. Any news that increases the chance that the Fed will slow down the rate at which they raise rates will push asset prices up. I covered this at the end of last week, although when I had covered it, my expectation was for a lower CPI print due to the amount of our petroleum reserves that we are currently selling. It seems that pillaging our energy stores was not enough to offset the continued rise in prices.

You will continue to see this behavior from the markets until the Federal Reserve is forced to change course, which is why the macro has been, and still is flat/down. All market participants are watching nothing else except for the Federal Reserve. Nobody cares about any of the data beyond the question “what will the federal reserve do as a result of this?” That question applies to the treasury markets as well. If the expectation is for the federal reserve to raise rates and continue to hold liquidity out of the treasury markets, then the treasuries will continue to sell off. Any speculator would be silly to be buying treasuries right now, and as such interest rates are continuing to rise as the sell-off continues.

We’re getting close to the point where the new issuance of debt will be upwards of 4% as the 1 year bond and above are all sitting around 3.9%. Even at the shortest end of the curve on the 4 week bill, yields are currently sitting at 2.6%. According to the government, their average interest paid on debt is still sitting at 1.971%.

What will interest rates look like by the end of the year? In march, I was predicting 4.5% on the 3 year note by December, but at the current rate we may very well eclipse that prediction, which probably seemed like a ludicrous prediction at that time. This also implies that asset prices will be pushed even lower to close the year out. You should be keeping that in mind as the year continues, do not go all in on these markets yet, we still are not at the secular bottom, and you still have time to be accumulating more cash or continuing a calm DCA strategy.

Currently, the Fed only has one tool available to them to inject some liquidity back into the markets. This is, as I’ve stated before, the Overnight Reverse Repo facility. If they stop paying interest for entities using that facility, most entities using it will stop, and will likely use their liquidity to buy treasuries and other assets. It will essentially release ~$2 trillion in funds back into the broader markets. So there will be a brief period where that money will be chasing assets until those entities are repositioned as they wish to be. I expect that when the Federal Reserve does this, it will be a sign that the Treasury has pressured them, and that they’re close to the end. Releasing the liquidity in the Reverse Repo facility will likely put a short term bottom into the markets, but the bleeding will continue after that. Be aware of the coming playbook and plan accordingly.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.