Advanced Guide to DeFi #2 - StableCoins

Advanced Guide to DeFi #2 - StableCoins

Tether, USDC, UST, and other Algo Coins

I didn’t realize this needed to be written, but it was brought to my attention that there was a bit of a hole in the information I’ve been sharing.

This is a guide for people that are familiar with everything discussed in the Beginners guide to Crypto, and for people familiar with the basic function of a DEx I outlined in section 2 of the Beginners Guide to DeFi.

You also should be familiar with Signing Transactions as well.

A Definition list for the abbreviations, words, and terms that I use.

As usual, this post is too long for email, be sure to check out the substack site or download the substack app if you have an apple product or iPhone.

Table of Contents

What are stablecoins

Why do they exist

History of Stablecoins

Tether

Bitshares

Types of Stablecoins

Fiat-backed

Commodity-backed

Crypto-backed

Algorithmic

Stablecoin risk

Oracle Risk

Regulatory Risk

Conclusion

1. What Are Stablecoins

The basic definition of a stablecoin is as follows. A stablecoin is a cryptocurrency that is designed to track the price of a non-crypto asset. The stablecoins people are most familiar with are dollar stablecoins which track the price of the USD so that 1 stablecoin is more or less equal to $1. However, there are stablecoins for other currencies as well, such as the British Pound, the Euro, and the Chinese Yuan. There are also stablecoins that exist and peg their value to the value of Gold, Silver, and probably other commodities. If they do not exist yet, I have no doubt that they will come to exist at some point.

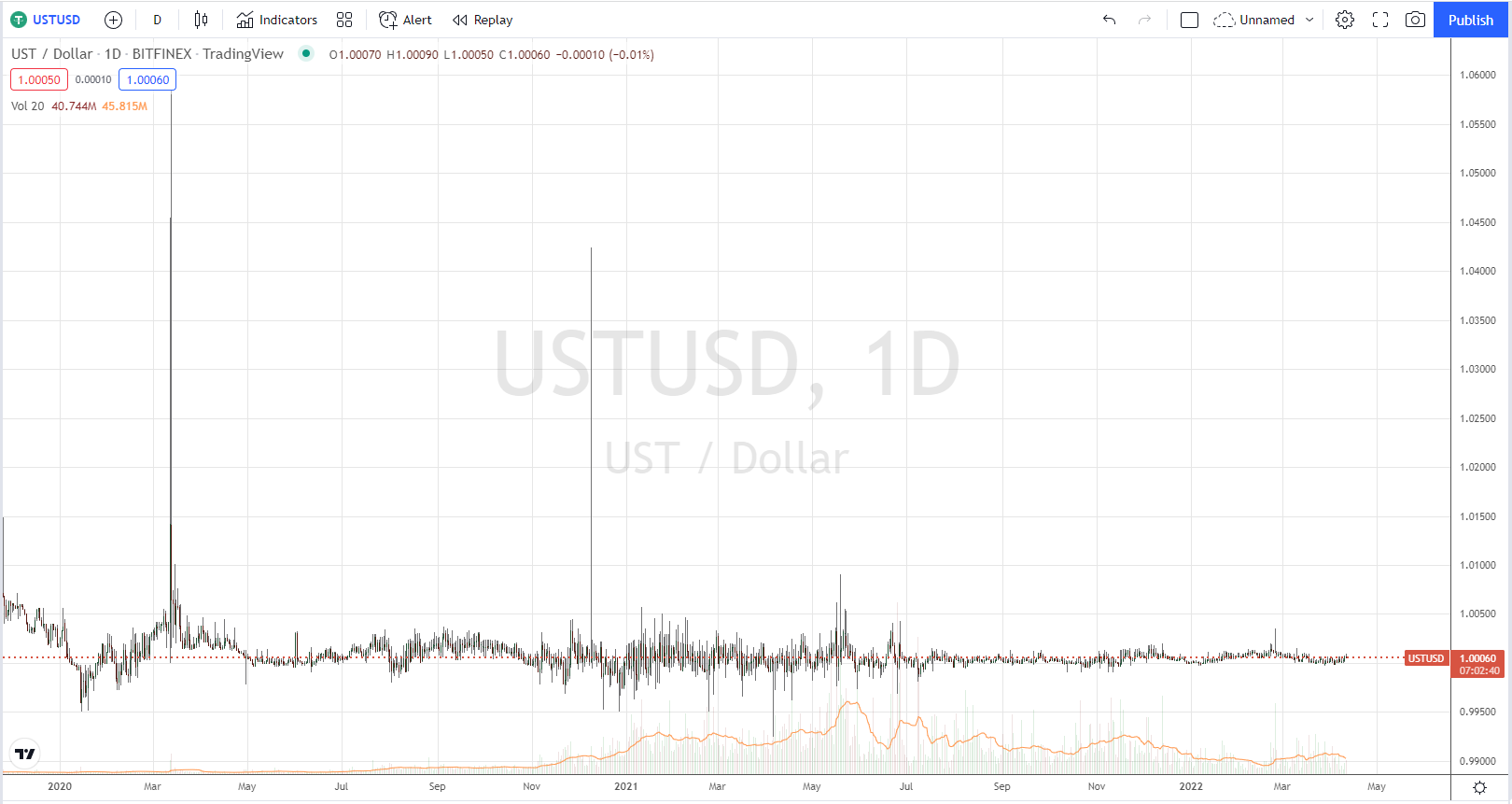

But what you need to know is that the point of the coin is to have a price that is within an acceptable tolerance of an outside reference price. What would be considered an acceptable tolerance is dependent on the user. The more popular dollar stablecoins rarely track outside of +/-0.2% of $1. Some of the newer dollar stablecoins with less volume behind them might only be aiming for +/-1% or 2% of the US dollar. In times of significant unexpected trading volume stablecoins can briefly lose their peg by 10% or sometimes even 20% in a few places. Below is a chart of Tether price from February 2020 to now. This price is specific to the Bitfinex Centralized Exchange only.

You can see that there were a few disruptions in price on this exchange. During the March 2020 crash when individuals were trying to sell out of assets and into dollars, Tether rose 6% on this exchange to a value of $1.06. Similarly there was another point in December 2020 when it rose up to a value of $1.04. But otherwise, on this centralized exchange Bitfinex, price has been relatively stable. The Price of any asset can be different in multiple places. This is mainly a function of liquidity. Bitfinex was probably running out of available Tether, as people were bidding it up when they tried to buy back into Tether, which meant that they were selling their assets below market value. One thing that could also have been occurring, is that its possible Tether prices were even higher elsewhere, and people were simply buying it on Bitfinex to transfer it somewhere else to sell it. A 4% difference in price creates an arbitrage opportunity, and many traders are running bots that automatically arbitrage stablecoins across a number of centralized and decentralized exchanges for profit. This kind of activity actually serves to make stablecoins even more valuable as they can more easily keep their peg. We will discuss this in greater detail in Section 4 when we talk about the types of stablecoins, how they function, how they hold value and how they maintain their peg on exchanges.

2. Why do They Exist

Stablecoins exist for a fairly simple reason. People want to trade assets back into US dollars or other fiat temporarily without exposing themselves to tax liability, or without taking their assets off chain and back to a centralized exchange.

For instance, one of the main thesis’ of this substack is that asset prices are going to be flat or down until the Fed is forced to intervene to rescue the US treasury from either a failed treasury bond auction, or untenable interest payments. I currently have around $7,000 in stablecoins sitting in a Liquidity pool earning around 7-18% APY (potentially more depending on future value of reward tokens). I would have liked to have had more stablecoin sitting ready, but due to the issues with my bank I have not been able to really move more assets into crypto since January (and have sadly had to liquidate some instead). If I had not sold assets into those stablecoins, those assets would be worth 4x less today than they were when I sold them. Stablecoins allow speculators to lock in profits for periods of time without having to bring assets to centralized exchanges.

Of course, there are stablecoins on centralized exchanges as well. In the past centralized exchanges didn’t fully report transactions to the IRS, and so trading into stablecoins on those exchanges was perfectly fine behavior, which is why stablecoins are available on exchanges. Currently they are still tradeable on exchanges, but their purpose on centralized exchanges is waning and will continue to wane as regulation on centralized exchanges continues. This of course is a detriment to certain types of stablecoins (the ones backed by real world assets like Tether, USDC, etc.), and is a benefit to other kinds of stablecoins (the ones that are algorithmically backed or backed by on-chain assets). I’ve explained the conclusion before in the first crypto macro post from December, but will go into more depth into how I came to that conclusion in Section 5 of this post.

The other regulatory push I’m seeing is centered around regulatory entities finally discovering stablecoins. These entities are mostly retarded and not up to date with the sector, so they are only targeting the most visible and centralized stablecoins. For now they are only able to target Tether in an attempt to restrict stablecoin issuance to only large banks and financial institutions to the detriment of Centralized Exchanges that don’t play ball. Governments have no ability to target algorithmic stablecoins, nor stablecoin minting in DeFi from users connecting pseudonymously with their wallets. This is for the same reason that governments cannot target DExes. When something is truly decentralized there is no neck to separate the head from the beast. We are the proverbial Hydra and poor Hercules has nothing but a sword.

So, stablecoins exist to provide the service of allowing speculators to temporarily lock profits or take an unleveraged short against their crypto holdings. As DeFi expanded, money markets and crypto lending have created additional use cases for stablecoins beyond just the preliminary service being provided to speculators.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.