Anarchy on the Blockchain

Rules... but no rulers, unless you want them

For those of you that are paid subscribers, you may have seen some commentary in Section 3 of this post where I discussed my first attempt to create a job for myself in blockchain. Yes, that’s correct. A job, with a recurring monthly salary. This has been in the works since January, but in truth it’s been in planning since October.

I’m going to explain what it was, why, how, and what jobs of the future will look like, while also explaining how blockchains themselves can become digital nations with their own governance. As blockchain advances, you will see decentralized governance entering more sectors of your life.

I have added a Definitions page which will include all of the terms and abbreviations that I use from now on and will be referred to on every post.

If you’re new, it may be good practice to read my FAQ after you finish this article.

Table of Contents

Blockchain Governance

Governance Proposals

A Job on Blockchain

Blockchain Grants

Conclusion

1. Blockchain Governance

Blockchains are semi-sentient entities that are self-interested in their own expansion to the extent that the owners of those tokens are usually interested in the growth of that chain. This isn’t always the case, but is generally true.

How does a blockchain exercise its sentience?

Phrased another way, how does a blockchain make decisions on behalf of it’s users and stakeholders that represents the will of those users and functions in their best interests? A blockchain is not like a corporation where a founder, CEO, or board of directors are authorized to make top-down decisions on behalf of the entities holding equity in the corporation.

So, how can a blockchain, or any digital entity fairly make decisions on it’s own behalf? The simplest way is to allow all stakeholders to vote, and some form of buy in for a user to submit a proposal for a vote. Yes, voting and democracy as concepts are thriving on the blockchain. Decentralization is the key tenet of blockchain, which means that leadership and decision making can’t come from a central figurehead. Sure, there are a few chains that completely ignore this central characteristic of blockchains, like Ripple ($XRP), where Ripple Labs Inc. and it’s corporate substructure is essentially wholly in charge of the blockchain and governance.

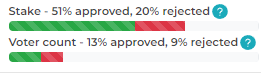

But there are thousands upon thousands of different crypto-currencies, and XRP is just one far end of the spectrum. Most blockchains allow all holders of the token to vote on proposals, these proposals can be for literally anything, and most of the time it’s just mundane stuff. Below is a screenshot from my fwallet for the Fantom network ($FTM). I don’t participate in FTM governance because it requires you to migrate your tokens out of metamask and into the fwallet. The tokens are far more useful in metamask.

You can usually click on governance proposals, and I expanded the most recent one regarding migrating the branding of an on-chain stablecoin to a specific DEx (Decentralized Exchange). It failed because the governance requires a minimum percentage of eligible FTM to participate in the vote and they didn’t cross that threshold.

If you are curious to read a bit more of the basics behind FTM’s governance, I’ve included a brief a link to their official explanation of the on-chain governance.

The voting is entirely on-chain and decentralized, and 1 FTM equals one vote. Governance is available to FTM holders who stake their tokens.

Any FTM token holder who stakes FTM can submit a proposal. Each proposal submission costs 100 FTM that will be burned during the operation. Voting costs just the transaction fee, usually a fraction of 1 FTM, or $0.00001.

The main thing for you to take away from this is that a blockchain is just code that has been released into the Æther. For the code to be changed, human action and intervention is necessary. But for it to be fair, the rules for how humans can change the code has to be established when the code is released. Some chains give 1 vote per 1 wallet, no matter how much of the token you hold, this can be gamed by creating many wallets. Some chains, give 1 vote per 1 token; this advantages early adopters and the wealthy. Some chains have delegated voting, similar to how the electoral college works in the US. You delegate your tokens to a node, and that node votes on governance on your behalf. Hopefully they represent you well, if not, you delegate to a different node. The limit is essentially our imagination. Pointless to hate Ripple for controlling their token when there are thousands of other chains you can participate in instead. Typically, submitting a proposal costs money to make sure that some skin is in the game, sometimes this is relatively cheap, sometimes it costs over $10,000 to submit a governance proposal. Again, you choose a chain based on which one fits your preferences.

You get to choose your rulers, and if you want, you can choose a chain with no rulers.

2. Governance Proposals

This will be a short section, but essentially anything that can be coded can be proposed. Sometimes there are restrictions on what can be proposed, sometimes there aren’t. Last year I made a post on Instagram about DAO’s (Decentralized Autonomous Organizations), within it I provided an example of a governance proposal that was made on UNIswap ($UNI) to establish a DeFi lobbying firm using a portion of UNI’s treasury. This amounted to roughly $25.7 million at the time of the vote (roughly 0.2% of their treasury).

The lobbying firm that was created from this vote appears to be active, but I haven’t dug too deep into them to see what they have actually accomplished yet, if anything. However, the example is here simply to point out that the establishment of real things, in the real world are possible through blockchain governance.

There are of course concerns about the corporate capture of blockchain governance. For instance, Harvard University had a significant ownership share of UNI at the time of the vote to establish the lobbying fund above, and it should be noted that the proposal included some of the allocation to go to Harvard in exchange for certain services. Is there a risk of some corporate capture of governance? Yes. But again, the solution is simple, if you don’t like it, sell and move to a different chain. There are literally thousands of chains, and I have no doubt that in the future some silly corporation will spend hundreds of millions buying a sizable governance position on a chain, only for a bunch of degens to dump their holdings and move somewhere else. The corporations have a financial incentive to behave in line with the established culture when they enter these spaces.

But, proposals can also plausibly lead to evil as well. Here is something a little more gray, and a little less black and white. It’s a recent proposal on Juno ($JUNO), which is a Layer 1 protocol built on top of Cosmos ($ATOM). There was an airdrop and a whale manipulated the mechanics of the airdrop to have a large amount of the token sent to their wallet. Personally, if the mechanics of the airdrop had a fault in them, the responsibility lies on the developers, not on the person who exploited these mechanics. But my personal opinion doesn’t matter, as a governance vote was held to initiate a hard fork, where two chains would be created from the current existing blockchain. One where the whale kept their tokens, and another, where the whale’s wallet address had its total token amount adjusted down to what it should have been based on the intentions of the developers from that airdrop. Presumably, the fork where the Whale’s token amount was adjusted is the one that the developers will be working on. This is a fairly significant development for governance to impact wallet totals, my opinion on this is negative; but good news is I’m not on that chain, so who cares what my opinion is.

You are probably already familiar with the forking mechanic even if you don’t know it. For instance, Ethereum and Ethereum Classic exist as a result of a governance vote that resulted in a hard fork. Some users wanted to stick with the original code, and preferred that chain instead, everyone who owned Ethereum before the hard fork has a wallet for both chains and both Ethereum and Ethereum classic in that wallet. Mostly everyone was happy.

98% of all governance votes are going to be mundane operations making minor changes and adjustments. These votes typically authorize the expense of assets in the treasury to pay for developer hours to make minor tweaks in the code. Sometimes these tweaks are major, but for most Layer 1 tokens it’s extremely minor changes.

Again, this is limited to your imagination. So long as you never post your wallet address in any space where it can be tied to your identification, your operations in this space are fully pseudonymous. For the cost of submitting a proposal, you can alter the fabric of the future if your proposal is popular enough. Most blockchain governance has a forum tied to it for members and users to ask questions and better understand community sentiment and the existing functions to make sure that you aren’t wasting your time with an unpopular or impossible proposal. But beyond that forum, you and every other holder of the token directs the future of the token in essential anonymity. This is the opposite of Apple which hasn’t really been able to function in a sensible manner since Steve jobs died.

Crypto is intended to not be dependent on any one personality or single driving genius behind it. The creativity behind the decision making is truly decentralized here. Any one can submit new proposals to create anything they want in crypto (within the limits of the specific blockchain being used). Read that last sentence again. I can say this, and I know it to be true within my bones because I have participated in it multiple times and seen how different it can be depending on the chain. But I can almost guarantee that at least one person will read that sentence and their first reaction to it is cynicism about some 3 letter organization. People have a certain learned helplessness about them. Sure, the WEF (World Economic Forum) probably has fingers in a half a dozen blockchains, so what? Choose a blockchain where you don’t feel their influence. You can find pure anarchy if that’s what you want, or any form of limited/distributed governance between that and the autocracy of Ripple. If you are intelligent enough, you can find some struggling blockchain on the fringes (outside of the top 100), accumulate a few thousand dollars worth, and start influencing the chain in whatever way you want. You can even influence the chain to fund developers to make dApps for you. Many chains have incentive and grant programs right now that came into existence because it was suggested in governance by some anonymous degenerate.

3. A Job on Blockchain

So now this story turns a bit more personal and we’re going to talk about me. Since fall of last year I have been working part time as an anonymous consultant on chain for blockchain projects. I am essentially working for free with 2 others within a larger DAO of a dozen or so people in exchange for future project equity. We wanted to make our DAO larger and associated with the Layer 1 token it was built on. This Layer 1 token is Icon ($ICX), a sleepy token that sits right around the cusp of top 100 by marketcap. This token’s governance is done through delegation. You as a token holder delegate your tokens to a node, the node votes on governance on your behalf. Similar to the US electoral college. Our DAO straddles several layer 1 tokens including Polkadot ($DOT), but we have a node on ICX and you could consider that our home blockchain.

Governance proposals on ICX come in two separate forms, we’re going to focus on the more relevant form which is called CPS (Contribution Proposal System). Essentially, whenever any users makes a transaction on this blockchain, a small fee is charged. This fee is used for a number of things, but a portion of it is sent to a treasury specifically for CPS. Every few weeks, the treasury reaches a certain dollar amount and can be distributed to projects that have applied for funding through the CPS. Essentially a portion of the network fee is used to fund anything that gets proposed and approved by the voting nodes. Applications are directed to focus on either building something on ICX or increasing awareness of ICX to increase the probability of being approved in the vote.

You can see where this is going. We submitted a proposal to fund us to expand the development pipeline on this chain, incubate a pipeline of viable DeFi projects to add to the chain, and to increase outside exposure to the CPS funding system. If you want to get real meta, you could say that me writing this article is doing exactly that right now… but I digress. We were rejected, I don’t yet know why. With delegated voting there really are only a few parties voting, and quite a few who I thought we had in the bag ended up not following through, but that is life sometimes. For those of you that are paid subscribers, you may remember reading section 3 of this post while I was waiting on the vote to complete.

I much prefer to get paid in crypto, which is what I set out to accomplish when I left. I’ve gotten close to my goal, and in truth, it’s being voted on right now whether my project will receive funding or not, whether I will have a salary in crypto or not, and it’s fairly tight at the moment.

This is the first inning of this world. We truly have our futures in our hands. This is one of the most meritocratic time periods and opportunities of recent history (I say, after having lost my proposal). I wish I could say everything that I know, but, just like the corporate world, some things are subject to confidentiality. I will however say this. No matter who you are right now, you have the potential and the access to move mountains should you so choose to do so with just a few years of dedication to some niche within blockchain. The job you create for yourself on blockchain does not have to be coding. Obviously, if you can code and have an understanding of blockchain, that’s better, there’s more work than there are people when it comes to coding and development. But if you have an intuitive idea for what blockchain can and can’t do and how it can interface with existing systems, you can write a proposal for a grant like the one I just lost and you might receive funding to pay someone else to make the system you have envisioned, and you can have a job for yourself as a custodian, a community manager, an admin, marketing, or whatever ancillary service your idea might need. Take a look at this proposal to create a decentralized social media and crowd-funding platform.

What roles do you see here? Not all of them require coding. No one here is checking for college degrees or for certificates. What does need to be in these proposals is an example of work, previous projects, or a strong community presence. Join those discord servers and telegram chats, make sure people know you. Work for free alongside visible projects, gain a few references in the crypto space on the chain you’d like to work on. Bring value adds and not just suggestions, but actionable suggestions. It’s one thing to tell someone to re-design their landing page, it’s another to send them an example of how it could be re-designed. Everywhere I go in the crypto space, no one knows who or what I am on the outside. All I have is what I have accomplished so far, and I highly recommend that you start thinking along these lines as well and become visible within the crypto space so that people might recognize at the very least your discord username. After a few years, it can get you farther than you might think.

You’ll notice that I didn’t link you to the proposal that I’m included on. That was on purpose. If you poke around the CPS site, you might be able to figure out which one was mine based on the details in this section, but I prefer the plausible deniability.

4. Blockchain Grants

When you ask people to name a few crypto-currencies, you will probably hear the same names from most people. Bitcoin, Ethereum, and maybe a Dog themed coin as well. For every other blockchain, marketing is the key for how they attract users and developers. Marketing, of course is not enough by itself, and so when thought of in the perspective of the concepts we discussed earlier (using governance to vote to deploy the treasury), it then becomes quite obvious that blockchains are using their treasuries to attract users and developers. I covered this in Section 4 of this free post. Brand recall for blockchains is dismal outside of the 2 or 3 that the minority of the population that invests in crypto is aware of. Blockchains essentially have only a few groups to advertise to.

The crypto ignorant

The uninitiated crypto speculator

The initiated crypto user

We’re going to talk about one form of marketing that is specifically targeted towards the 3rd group, crypto users. For this definition, a crypto user is someone that has self-custody wallets and knows how to sign transactions. Still a fairly novice user, but a user nonetheless.

That form of marketing we’ll discuss are Blockchain Incentive programs. I have mentioned these before in Section 4 of this free post. Smart contract platforms that want to incentivize a certain type of dApp development or usage will create an incentive program or a grant program to reward people for creating dApps on their chain. Developers making dApps brings users, and users bring more developers. These programs essentially are used to bootstrap a userbase on a side-chain. We’ll explore the Avalanche ($AVAX) incentive program here so you can get a picture of how this program was designed and what it’s goal was.

AVAX wanted to bring in more developers and more users. Usually when a DeFi dApp launches, it has to reward users in some way in order to get users to lock liquidity onto the platform so that it can function. AVAX is compatible with all dApps coded for Ethereum (this is known as EVM compatibility), and they wanted to incentivize Ethereum dApps to bridge to AVAX and have the dApp exist on multiple blockchains. But those dApps didn’t have extra governance tokens budgeted to reward users for locking liquidity on a new chain. So AVAX created a fund that they gave to developers to use as rewards for users on their platform. With this fund, developers could attract users for free and make money off of the user activity that the Avalanche platform paid for.

It was a no-brainer for developers, and this attracted more developers, which attracted more users, which fed into itself. You can clearly see this incentive program was designed to attract a very specific type of traffic.

Many other chains have very similar grant programs. They built up treasuries over a long period of time in order to deploy them like this. FTM pays developers based on how much liquidity they can get locked up over certain periods of time. So developers on FTM were focused on offering higher rewards for people locking up funds into DeFi for longer periods of time.

NEAR launched an incentive program that was influenced by outside VC money. It’s mainly focused on DeFi, and crypto-native startups. Perhaps we’ll start seeing several DAO’s coming from NEAR in the future that have an outside affect on the real world. Maybe UNI’s lobbying fund from Section 2 might seem quaint in comparison to the future.

And the list goes on and on; at the end of last year, and early 2022, the Layer 1 interest in creating grant programs like this probably peaked. Ultimately, the Proof of Stake blockchains that don’t need to pay miners transaction fees have an essentially self-generating treasury based on the level of user activity and the level of inflation that is programmed into the token. So long as there is demand for these tokens to keep the price up, then they are essentially perpetual energy machines that can fund projects and development.

Ultimately, what these tokens are doing is competing for talent from the traditional fiat system. Governments haven’t realized that they are competing for talent just yet, and they probably won’t figure it out for quite some time. If you can get paid in NEAR, ONE, AVAX, ICX, or FTM, etc for doing work, and we are going through a time of significant inflation, it becomes an even more attractive proposition for someone to make the jump. So long as the funds stay on-chain, there is no tax exposure unless you dox your own wallet address to the IRS. Inflation on these chains is anywhere between 3-7%, and fully transparent. Some of these chains can be deflationary for periods of time as well, depending on user activity. As they grow, they become more attractive as a personal reserve currency. If you can create a crypto-native company on NEAR that is governed by anonymous voting, or you can deal with the myriad red tape, regulatory oversight, and byzantine tax authority of establishing an LLC in the state of your choice, which do you choose? I believe that we are approaching a point in time when the calculus people do when making this choice is going to change. Unless the prospect of owning and holding dollars can be made more attractive, the risk of establishing yourself on a blockchain (even when they are giving you money for doing so) is going to be seen as minimal compared to the dollar.

5. Conclusion

You might not think that you have enough time for an additional job, but you most certainly do and can. My current role demands 10 hours a week, sometimes less, sometimes more. I can do that in my sleep. Not every blockchain job is 17 hour days 7 days a week. If you are writing the proposal, you can set your rate, you can set your expectations. You can stretch the deliverables out over an extra 3 months (maybe they’ll vote no), so your day to day bandwidth isn’t being compressed too much. Whatever you want, propose that. The worst that will happen is they’ll say no after you post about it on your blog.

You are in a world that is constrained only by your imagination. You always have been.

I once read that when people attempt to predict the future, one of the key reasons why they end up being wrong is because they lack the temerity to extend reasonable conclusions to their end point. They aren’t brave enough to take a conviction to it’s strange, but logical conclusion. They find themselves influenced by their normalcy bias. If you ask the average person to imagine what their life will look like when they are 80, most people will imagine themselves 80 years old in the current world. They won’t even think about how technology, medicine, population levels, living styles, governments, and tax regimes might change in that time nor how it might affect them. Most will imagine themselves wearing the same clothes they wear now. People do this with most everything when looking into the future, they only change one variable at a time and imagine the world with just that one thing alone changed. If you want to look into the future, you have to imagine all variables changing at once and then changing each other as they change as well. So too, when you imagine what possibilities may become available to you at any given time, be brave enough to change a few things radically, and meditate on the consequences for a little while.

Spiral upwards with me for a second. “I am now aware of the possibility that there are greater possibilities.” It doesn’t end.

I didn’t win the governance proposal; and that’s okay. I know what my future holds. I will have a job in blockchain, I will be paid in crypto for work that I do. I will save in crypto. I will spend in crypto. My financial existence will be in crypto. I don’t know exactly when that will happen, but I know that it will, and I know that it’s just the beginning for me. I do not know what the future holds for you, but as the existing government fiat systems go through their own K-shaped recoveries, I know that our opportunities to create careers for ourselves in the crypto space will grow and at some point we will reach that critical mass when the rest of the world tumbles over that barrier behind us and joins us on this side of the wall.

If you want anarchy, its yours, you can find it on the blockchain. These are digital nations in every sense of the word. Whatever level of ruler you are looking for, you can find that on blockchain. People will ultimately fixate on what they deserve. If you find yourself staring into the abyss of Central Bank Digital Currencies, that’s because you are genuinely afraid that you deserve those. You don’t. You deserve to be free, and as such, freedom will find you.

Dope

FREEEEDDDOOOOOMMMMM