This is a slow news week for conventional topics. All that happened was the RBA releasing their meeting minutes on Monday, snoozefest.

So instead we’re going to talk about other things this week.

Today we’ll discuss Gary Gensler’s testimony before Congress, and the House Subcommittee on Digital Assets, which was recently formed in January.

Please note that a large portion of the discussion during the SEC hearing is about climate change. This is because the SEC thought to propose rules about ESG disclosures to investors from companies. This is wholly beyond the SEC’s mandate and Gensler/the SEC are not experts on the climate at all. I mostly ignore these questions because it’s just not relevant and none of the answers provided by the SEC are scientifically meaningful.

Table of Contents

House Subcommittee on Digital Assets.

Gensler Testifies Before Congress

The Actual Testimony

Treasuries on Blockchain

What the SEC Knew about FTX

Custody of Digital Assets by Banks

Emmer Ripping into Gensler

SEC Limiting Public Comment Periods

Coinbase and Kim Kardashian Settlement

SEC Encouraging Front-Running of Trades

The Cost of Compliance

Gensler Doesn’t Trust Industry Participants

Gensler May be Obstructing Congress

The SEC’s Authority was Granted by Congress and the Pee Dossier

Conclusion

Internal References

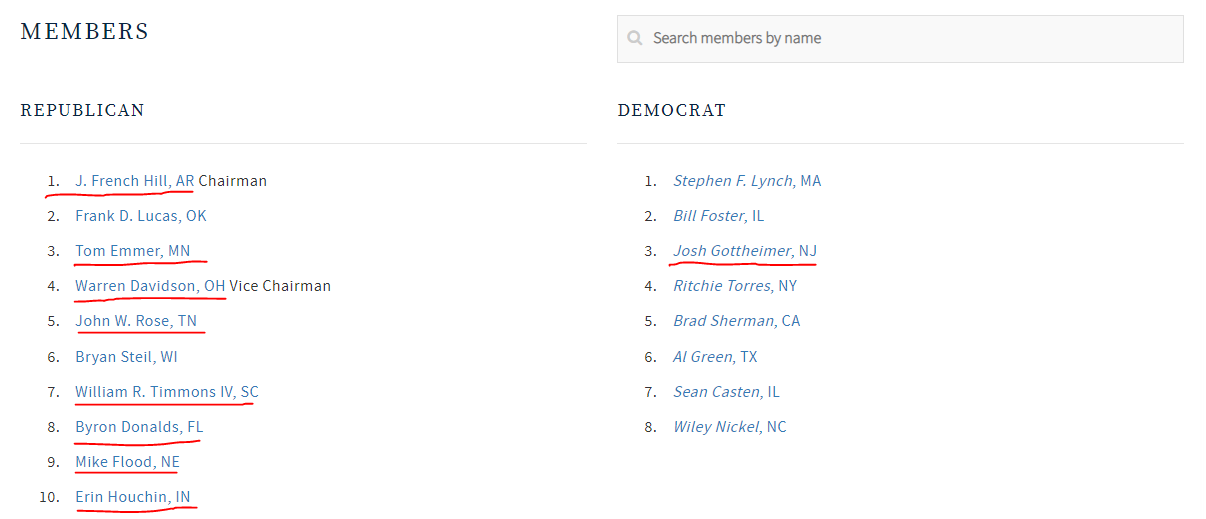

1. House Subcommittee on Digital Assets

This is a new congressional sub-committee, we briefly mentioned them on here at the start of the year, and they have been promising since then. The majority of the good questions directed at Gensler in his testimony come from this subcommittee. And despite being formed in January they have worked relatively fast to get processes in place and bring Gensler to testify before Congress.

We often look for quick solutions and find ourselves disappointed by a government that moves as slowly as wind-borne erosion. It’s refreshing to have a committee move this fast and actually seems to represent our interests before a government that has been wholly adversarial toward us.

Members of the sub-committee - names underlined in Red seem to be on our side

Looking forward, I would love to see the sub-committee achieve the following things despite the current state of the Senate and presidency.

Submit clear legislation outlining how a stable-coin can be compliant with the US government. Legislation should include reserve requirements, reporting requirements, and custody of reserves.

Submit clear legislation outlining how financial entities are to treat digital assets in custody in a manner that allows banks and US financial entities to be cost-competitive with the rest of the world.

Submit clear legislation outlining the ways in which a digital asset can avoid being a security.

Submit clear legislation outlining where the SEC does and does not have jurisdiction to enforce rules against digital assets.

Enact stronger rules for response windows within which the SEC has to provide requested documents to the Congressional finance committee and digital asset subcommittee.

I’m sure there is more but currently, the US crypto industry suffers from a lack of clear legislation, and Gensler and the SEC have been playing in the shadows by enforcing things essentially at a whim.

If you decide to listen to the entire hearing you’ll note that Gensler has not actually finalized any new rules during his term, but has been enforcing crypto entities based on Gensler’s statements alone. This is no way to run a successful industry. Imagine if the automotive sector was regulated by a DoT that made enforcements based on their tweets last week.

The relationship the SEC has with the American Public

There’s no rhyme or reason to it. Those who grew up in an abusive household (I’m sorry, truly) can probably relate to this. You never knew why or what would set off an abusive parent and so you just tried to do as little as possible and hope they wouldn’t notice you long enough to think about hitting you. Why are you getting hit today and not yesterday? You can try to find a rational answer but the truth is that there is none. Why is the SEC pursuing Bittrex today for allowing users to trade the same assets that all other CExes allowed? You can try to find a sensible reason but there is none. It likely may simply be that the SEC noticed Bittrex when they announced they were shutting down their US operations and that’s the only reason.

Gensler’s term can’t end fast enough, and if we were a serious country that was intent on competing in the next generation of finance on the global stage, we’d insure we never had a repeat of Gensler’s term at the SEC.

I think that the promise we can look for from the Subcommittee on Digital Assets is in how they develop and lead this discussion in Congress. I hope that in time we see them shaping legislation and taking back Congress’s mandate to create the law. The SEC has never had the authority to make new laws, yet Gensler acts as if they do. This needs to change.

Most people’s informal introduction to this subcommittee was in today’s testimony. If you watched it all, you’re a saint, but if not, consider the next section to be an introduction to this subcommittee. Almost every good question came from them. Please remember their names and remember their subcommittee.

2. Gary Gensler Testifies Before Congress

So today, Gary is testifying before the US Congressional House Financial Services Committee. It’s probably going to be 4 or 5 hours long, and I will be providing my thoughts and insights from this testimony here.

Unfortunately, most members of the US Congress are not tech-savvy, nor financially savvy so a good bit of this time is wasted. In general, I don’t recommend actually watching any of these senate or congressional hearings unless you are a glutton for punishment, but in case you’re into that sort of thing, you’re always welcome to do so and the video is embedded below. (holy shit it was 5 and a half hours, minus a ~45-minute recess)

As much as democracy is heralded as a meaningful political invention, it just slows things down. I don’t think everyone deserves a seat at the table. But democracy requires that every Senate and House committee has equal representation. Why? Why are there members of the financial services committee with no financial background or experience? Why is someone like Maxine Waters wasting the first 5 minutes of this hearing to applaud the SEC for doubling its manpower specifically to regulate crypto criminals?

Expediency has always been the name of the game in our democratic system. The voters don’t care or really know how the government is structured and often are rather blase about egregious violations of the separation of powers. The SEC is regulating crypto like the ATF is regulating guns. Illegally. The SEC has no power to make rules itself. The SEC was created by Congress as an enforcement agency to enforce the rules created by Congress. The SEC has no mandate to create law, yet they attempt to do this through the court system. This is how America has been broken and become a non-functional government.

If something is brought before the courts that have never been ruled on before, the judges are entrusted to faithfully interpret the law as it was intended by the legislation when it was written. But some judges within the US legal system are cowards, or incompetent, and a prejudiced prosecutor can tilt the tables so far that it is difficult for a judge to rule fairly or interpret the facts of the case dispassionately. If you remember the case against Ian Balina that I discussed last year, the SEC

It only takes one case to establish new precedence in the US. That’s the really shitty thing about how the US judicial system is used. The SEC can lose 99 times, and win once, and from then on out they get to use their terrible argument in cases over and over and over again until someone manages to overturn it. For anyone looking to attack the justice system and use it to their advantage, this is how it gets done. Laws are normally passed through congress and the senate, but activists can side-step the separation of powers entirely by inserting all sorts of nonsense that has no legal precedent into a court case and then quoting the ruling in the future if they win. It’s a roundabout way of making a law, and is so far outside of the intention of the US constitution that I suspect GWash and the gang would be sailing across a river with muskets and cannon-fire in the background if any one had tried it in their day.

In the case above, the SEC attempts to establish that because ETH mining/validating was primarily done by nodes in the US at that time, thus the SEC then had legal jurisdiction over all blockchain transactions that occurred at that time. How is a judge supposed to interpret that? If the judge fails, gives it a pass, or decides to accept the premise presuming that the SEC is operating in good faith, then the SEC can quote this single ruling in the future forever as a justification for expanding their jurisdiction.

This isn’t how the country was designed to operate. But it’s how this country does operate. The legal system in itself is punitive. Simply participating in a lawsuit ruins your life even if you win (speaking from experience).

Addendum

You’ll note that the sections near the top all have short video’s made of them, while those near the end don’t have accompanying videos. This is for two reasons.

The people making these videos only had attention spans to watch the initial hearing and began falling off as we got into the 4th and 5th hour.

The hearing is done in order of seniority. Those members of the committee that are more senior went first, and they tend to have more dedicated staff making clips of their testimony, likely to be used as re-election bait. While those near the end may not have had as many campaign staff ready to make clips of their portion of the testimony.

If I could have a video clip for each bit of testimony I would but near the end the availability of clips just tails off.

The Actual Testimony

Gensler refuses to answer the question of whether ETH is security when directly asked.

Maxine Waters mostly wastes time, none of her questions are seeking information, they instead seek opinions. Her questions also aren’t really questions. An Example she states “I don’t see how de-regulating capital markets is good for small businesses. Could you please explain whether or not you believe de-regulation is needed?” Of course, he doesn’t disagree and simply states that well-regulated markets have less risk within them. Questions like these are a waste of time. But in a Democracy it’s what you can expect. This is a hearing after all. Your own lawyer is going to pitch softballs for you to knock out of the park. Having someone on the Committee like this is a disservice to the American people. We already know what his opinions are.

I’ll avoid covering any questions like this moving forward. But if you didn’t listen to the entire thing and only listened to the highlights you might think it was 5+ hours of relevant and intelligent questions. In actuality, it was more like one good question followed by three nonsense questions.

Gensler is asked about Congress establishing legislation for stablecoins. Which is how laws are actually supposed to be made. Gensler answers in an unconstitutional manner by stating that while he supports a regulatory framework he doesn’t want Congress to undermine the SEC and CFTC’s ability to pursue enforcement. Congress gives the SEC and CFTC their authority, it’s not his place to tell them how to address him. An employee doesn’t tell the CEO what they will be doing at work. Your employer gives you a job description and you follow it or get fired, but in the government, things are so backward that the employee tells the CEO and we all watch and nod.

Treasuries on Blockchain

Representative French Hill from Arkansas asks a very important question that I suspect will become more prevalent in the future. “You have this proposal that people who are buyers of treasuries could somehow be swept up and become a dealer. Why would that happen?” Gensler responds by stating that parties who are facilitating buying and selling treasuries or making markets in these treasuries need to get registered due to a law passed by Congress in the 80s. Specifically, this is the Government Securities Act of 1986. I expect that in the future we will see treasuries represented by digital assets on blockchain (we already are tbh), and the protocols that register in compliance with this act are likely to be the ones that are the safest from regulation. But of course, so long as Gensler is in charge, no one is really safe.

Back to the Testimony

Unfortunately we then had our time wasted by a Democrat hung up on the 2008 housing crash, and then a Republican from Texas who had nothing important to ask but simply had a bone to pick with Gensler on how he introduced himself to the hearing and then spent a majority of his time talking about his father. Democracy at work again, neither of these people provide any value to the hearing but wasted 20 minutes of the public’s time.

What the SEC knew about FTX

After 40 minutes of more time wasting, Rep. Posey asks Gensler if he had any concerns with FTX prior to its collapse. He asked if Gensler ever directed his staff to look into FTX, but Gensler refuses to directly answer and instead states that he directed them to look broadly into the sector as a whole he then references actions the SEC filed against SBF. You may recall that FTX collapsed in November, and the SEC filed against SBF in December and January. It took them a month and a half after it collapsed before they could even submit filings about FTX. It’s quite obvious that despite meeting with SBF and FTX numerous times throughout the year that Gensler never looked at FTX and was likely made aware of their collapse when they saw it on TV. Posey later states that the SEC is facing its higher attrition rate in 10 years and asks them how they’re handling so many employees leaving. Gensler provides a non-answer about how their attrition rate is in line with the financial services industry (it’s not, and it’s hilarious comparing the private sector to the public sector).

This is followed up by another time waster asking Gensler about raising the debt ceiling. That’s not Gensler’s job nor is it his responsibility. This is another softball from what is essentially a congressional member acting like Gensler’s lawyer. Remember that this hearing is likely going to be 4 hours long, we’ll get maybe 1 hour of actual relevant discussion. Everybody does not deserve a seat at the table. Worse, this representative (Cleaver) doesn’t even get his history right, he claims we’ve only defaulted on the debt once in 1812. Cleaver was alive the last time we defaulted on the debt, but he doesn’t seem to know about the default in 1979. This man does not deserve a seat at this table.

Representative Huizenga makes it clear that when the committee requested info about what the SEC actually pushed for in regards to charging SBF that the SEC was not-cooperative and has not sent any of those documents to Congress. Again, keep in mind that Congress created the SEC, and the SEC is supposed to be accountable to Congress. But we live in backwards-ville.

Another Representative is asking the chair of the SEC about sea levels in the Gulf Coast being up 8 inches since 2010. This question is eventually twisted into one about insurance rates and repackaging that risk into financial products, but again, it’s a question with no substance that doesn’t challenge Gensler for facts but simply asks for his personal opinion. Another waste of time.

Custody of Digital Assets by Banks

Representative Barr asks Gensler about the recent Staff Accounting Bulletin requiring banks to list digital assets they have custodied on behalf of their clients on their balance sheets (custodied assets have always been off-balance sheet items for banks). This is a great question because it significantly impacts how banks have to function and their reserve requirements for lending, while non-bank entities would not be burdened by this. The obvious conclusion is that US banks would simply choose to not have custody of digital assets and we’d find only foreign banks doing so.

Such rules often impact the financial sector, and chase financial services overseas. I have been an FX trader on and off since 2014. My primary broker is located in Canada, and my secondary broker is in the Dominican Republic. I would never in a million years choose to do business with a US-based brokerage because of the rules the government has set against what they call “high-frequency traders.”

Neither of these brokerages accepts US clients. I am grandfathered into my broker in the Dominican Republic, and the Canadian brokerage opened an account for me that strictly deals in crypto deposits and withdrawals so I can side-step typical KYC/AML requirements. Technically a crime, I don’t care.

There is no doubt that interference in the crypto markets will (and is) similarly chasing industries and businesses overseas.

Barr asks Gensler if he is aware of the irony that the Staff Accounting Bulletin allowed for the growth of FTX offshore in the Bahamas to grow without any competition from US entities, and apparently no real insight or oversight from the SEC. Barr doesn’t answer the question at all and even states he was proud of this Bulletin.

Barr then asks him if the SEC was aware that FTX, a $32 billion company was being run on QuickBooks. We know that the answer to this is no, the SEC was not aware. This is essentially one of the major consequences of making things difficult for existing regulated entities in the US to compete. You get wholly unregulated entities growing outside of the US and doing whatever they want. Gensler states that if crypto-companies registered with the SEC that they would have access to their books, but again, registering with the SEC has proven to essentially be impossible for crypto-companies. Coinbase tried to do so last year, and despite being the largest US-based centralized crypto exchange the SEC has not responded to coinbase in 10 months (so far). If the SEC were genuinely trying to get US-based crypto-companies to register, you’d think they would make any sort of attempt to work with the largest US-based company as they’ve tried to register. Instead, the only crypto company they made any attempt to meet with last year was a Bahamas-based company with no oversight. Says a lot about the SEC’s priorities.

Emmer Rips into Gensler

The star of the show, Representative Emmer rips into Gensler asking him to provide yes/no answers to questions.

While these questions feel good to have someone pressuring Gensler, the truth is they are just an emotional outlet for us. Will this result in any changes? No, not yet at least. Will Gensler have to answer for any of this? No, he won’t. Will the SEC change its stance and acknowledge that its mandate comes from Congress? No. But at least there is someone within Congress who is on our side.

SEC limiting public comment periods

Gottheimer (finally, an intelligent Democrat question) asks Gensler if he is concerned that limiting the public comment period to 30 days for documents and rule changes that are hundreds or thousands of pages long may be too short for stakeholders to actually participate meaningfully.

Gensler provides a non-answer about how these documents are on the website for longer than the comment period, but of course, there is no way to leave comments on the website.

Rep. Davidson quotes Gensler’s claim that Coinbase is selling unregistered securities and then asks Gensler if the SEC reviewed Coinbase’s IPO documents. It’s another time when Gensler contradicted himself in public comments made. The SEC should not have approved Coinbase for IPO if they believed Coinbase was selling unregistered securities. It’s either one or the other, it can’t be both. Gensler had charged Kim Kardashian for promoting an unregistered security for promoting EthereumMax.

Ironically, Gensler has promoted the Algorand project in the past. One has to wonder if Gensler would sue himself for promoting an unregistered security.

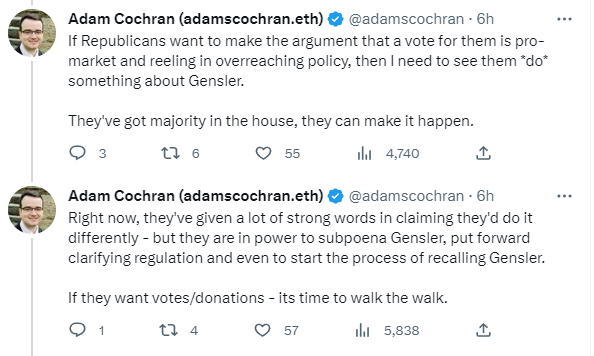

Rep. Davidson is introducing legislation to replace the head of the SEC.

While this is great, it won’t pass with the current Democratic Senate and Biden as President. It would require Democrats to vote for it and for Biden to sign off. Somehow we have ended up in a world where the Democrat party is almost universally against crypto while the Republican party seems to be significantly against Gensler and the SEC. One has to wonder if this dynamic would still be in place if the Republicans had a majority. Full disclosure, I’m a libertarian-anarchist who leans Republican. But one repetitive experience I’ve had from watching the Republican party is that they only really ever seem to fight for your interests when they’re in the minority. I’m cautiously optimistic but have no real belief that if Republicans won the presidency and Senate that they would genuinely fight for a healthy crypto-economy. But what other hope do I have?

This is exactly where Republicans usually fall short of their promises

The obvious answer is that I believe what happens on blockchain, stays on blockchain. I have little interest in political solutions and my true aims are for a world that leaves the US government and the dollar behind entirely. Whether the Republicans are actually our allies or not is irrelevant. I truly believe that one day we will not be off-ramping into fiat. Gensler’s attitude and that of the current Democrats is just the irrational exuberance of the captain of a sinking ship.

There are no political solutions

SEC Encouraging Front-Running of Trades

Representative Timmons brings up how frontrunning trades can be damaging to investors but brings up the SEC’s proposal for an auctions mechanism that would publicly announce the details of a retail order prior to executing the trade. Essentially creating a system through which front-runners would be able to readily front-run retail investors.

Gensler’s answer is silly and references how auctions occur in the options market. But options function in a significantly different manner. You can’t front-run an option just because you know it is being auctioned. A trader can certainly front-run existing options, but they can’t actually damage the positions held by those with the options.

Gensler is essentially being asked if the plants should be given water instead of Brawndo, and his answer is that Brawndo is good for humans.

The Cost of Compliance

Rep. Garbarino mentions how those in the cyber-security industry spend 30-40% of their time on compliance-related tasks instead of doing their actual jobs. He mentions new regulation introduced last year and a 1,400-page rule change proposal submitted recently. He asks if compliance has gotten too onerous and is leaving the financial services industry vulnerable by taking manpower away from their actual jobs.

We don’t get much of an answer from Gensler instead, he just mentions that the comment period has been re-opened on the 1,400-page proposal.

Compliance with regulation is absolutely a soul-sucking part of any job and chases employees out of sectors. I will turn back to my own experience to discuss it as I had to track my hours worked and submit a timesheet and roughly 40-60% of any given week was spent doing compliance tasks for CFIUS and our procurement. Of course, my employer could have hired someone to do this separately from my job (lol, they did after I quit), but the other consideration the government never really makes is how much more expensive everything gets when they turn one job into two jobs. Something has to break. You either force an employee to do a second job for free or the employer hires two people to address the workload.

Regulation, by definition always makes things more expensive. The question that should be asked before introducing new regulation is the following: “How much will this increase the cost of products the American people are buying? Is that price increase worth it?”

Often, those in government have never worked in the real world and typically have no mental concept of this fact and the burden imposed by them. Gensler displays no conception of this concept either. Which makes sense, he’s been out of the private sector since the 90s. It’s plausible that he may be unaware of how much additional regulatory burden has entered the industry since then. Most government employees either have no concept of this or have a concept that is horribly dated.

Experience in the private sector deteriorates with time. Even for me; I’ve been out of the Utility-Finance Sector since January 2022. I no longer am aware of the bleeding edge of that industry. In another year I’ll probably no longer be aware of general industry standards. In 5 years, my experience will be primarily historical with little real-world advice that I could give to someone in that industry. Everything deteriorates, and I have to be aware of how my own experience deteriorates as well. People are far better off when they are aware of how relevant/irrelevant their experiences are to people in the midst of it. Your parents probably can’t give you any decent dating advice because they’ve been out of the mix for too long. Similarly, Gensler is likely not in touch with what the regulatory burden is like for current financial agencies. The problem is that he likely believes he is because of his experience in the 80s and 90s. It’s a dangerous combination.

Gensler Doesn’t Trust Industry Participants

Rep. Lawler asks if the SEC deserves any culpability for the collapse of FTX.

Gensler doesn’t answer.

Lawler asks why the SEC didn’t take action on FTX’s secret lending of $4.8 billion to Alameda Research.

Gensler provides a non-answer.

Lawler brings up the SEC’s OIG (Office of Inspector General) concerns about the SEC shortening comment periods and asks him why they have been ignoring the OIG.

Gensler doesn’t answer and Lawler brings up a remark made by Gensler where he stated “I don’t trust industry participants to provide honest feedback.”

Gensler doesn’t answer again.

A few key takeaways. Gensler doesn’t accept any accountability for things that happened under his watch. You’ll note that Powell and the FOMC take responsibility for the crash of SVB and other banks despite this not really being their responsibility at all. No similar accountability comes from the SEC. Says a lot about the SEC’s goals.

For those unaware, the OIG is an office attached to almost every executive department to provide oversight of their actions and their use of funds.

We get some sort of answer for why Gensler has shortened the comment periods, it’s because he simply doesn’t care for any input from the public at all.

Again, another Tangent - When we had open public comment periods for the offshore wind farm I was developing, we took every comment in good faith, even the ones that seemed to be self-serving or illegitimate. We heard all sorts of nonsense during the comment period, and yet we still addressed them and worked with locals and stakeholders. Having such a hostile attitude towards the industry says a lot about Gensler’s goals at the SEC, and may even give a picture of how he behaved when he was in the private sector. Maybe when he worked for Goldman Sachs he didn’t operate in good faith, and he sees himself in the world. I don’t believe that of us. But it could be Gensler has trouble looking at himself in the mirror and this is how he deals with that.

Gensler May be Obstructing Congress

Rep. Ogles asks Gensler why he hasn’t shared the documents regarding the FTX charges with the committee.

Gensler states that there is confidential information in those charging documents.

Ogles then reminds Gensler that Congress has a committee on Homeland Security and the DHS is required to share confidential information with the committee on a regular basis in compliance with their congressional mandate. Gensler is (obviously) failing to meet his congressional mandate and Ogles implies that Gensler may be actively obstructing Congress. He threatens to take extraordinary measures to get these documents from Gensler, but I’m unsure of what that means and how that might happen.

Ogles quotes the Securities Act of 1934 which created the SEC but then runs out of time, so we don’t get to hear what his point would have been.

Rep. Norman then reiterates that Gensler has thousands of staff members and it’s unacceptable that the SEC has failed to even respond to the committee regarding the documents that were requested in January.

The SEC’s Authority was Granted by Congress and the Pee Dossier

Lastly, Rep. Donalds asks Gensler if he thinks that Congress intended for the SEC to be making rules about climate disclosures.

Rep. Byron Donalds (is he our guy?)

Gensler states that companies are already making these disclosures and that the SEC has congressional authority to do so.

Donalds firmly states that Congress only explicitly gave the SEC regulatory authority for financial statements, not for environmental statements and that the Securities Act of 1934 is explicit and does not grant authority for the regulation of environmental statements nor the regulation of digital assets.

Gensler states that Congress painted with a broad brush in the 30s, Donalds shoots back that they could not have granted authority for things that did not exist no matter how broad the brush was.

The last question made it all worth it.

Donalds states that Gensler was the CFO for the Hillary Clinton 2016 presidential campaign. He asks Gensler if he facilitated the payment of the Steele Dossier.

The actual dossier is long, but 4chan will forever live in infamy as having submitted a paragraph that actually got included in the CIA dossier

Gensler states he was not aware he would be asked this and rep. Donald reminds him he is under oath. We never get an answer but I enjoyed getting a laugh at the end of all of this.

3. Conclusion

Wow.

What a waste of time.

One thing that bugs me is how little respect this congressional committee had for this hearing. This disrespect emerged in many ways, some clearly didn’t prepare at all. Some didn’t avail themselves of the issues. Some failed to represent their constituency. Some chose to talk about topics that had nothing to do with the SEC. But what bugged me the most was that after the recess, almost all of the congressional representatives were gone. They just didn’t come back.

This is the Committee on Financial Services. And most weren’t even interested in hearing the entire testimony from the head of the SEC. What could they possibly have to do that’s more important today than this? If they aren’t interested in financial services, then why not give up their seat to someone who is? The disrespect for the process they have been appointed for is the biggest problem I have with our legislature as a whole. They are wholly disengaged from the actual job. The public trust is dragged through the mud by these people. Both Democrat and Republican. What a shame that this is our legislature.

4. Internal References

If you’re new and have a question, please read the FAQ post first.

Great write up and RIP to your lost *almost 6 hours of time.

It never fails to amaze me how absolutely UNSERIOUS 99% of our "representatives" are. To your call out about seniority and having staffers on hand to make gotcha clips for the next campaign; government is about personal enrichment and power to most. They are not public servants; they look down on us and care not for the havoc they create. All that matters is keeping their gravy train running.

Disrespect and disregard to what actually matters logically is the trend. Non emotional topics and eyes glaze over, w blatant dismissal to the impact.

For me day to day "oh the owner can't make xyz, poor him" but no connection to the lost jobs and ability for ppl to work in the process.the lost trust if certain metrics are not made to prove ability to operate efficiently. Not saying there's not greed, but as you often say emotion takes over. If the politicians don't see the emotional ploy of being there, why be there. And those who don't understand can't see the life raft being given or taken away, it's too long of a timeline. We get what we deserve.

Great write up and RIP to your lost *almost 6 hours of time.

It never fails to amaze me how absolutely UNSERIOUS 99% of our "representatives" are. To your call out about seniority and having staffers on hand to make gotcha clips for the next campaign; government is about personal enrichment and power to most. They are not public servants; they look down on us and care not for the havoc they create. All that matters is keeping their gravy train running.

Disrespect and disregard to what actually matters logically is the trend. Non emotional topics and eyes glaze over, w blatant dismissal to the impact.

For me day to day "oh the owner can't make xyz, poor him" but no connection to the lost jobs and ability for ppl to work in the process.the lost trust if certain metrics are not made to prove ability to operate efficiently. Not saying there's not greed, but as you often say emotion takes over. If the politicians don't see the emotional ploy of being there, why be there. And those who don't understand can't see the life raft being given or taken away, it's too long of a timeline. We get what we deserve.

Only God can provide.

*3 glasses of wine and several opinions later*