June US Treasury Auctions

The Dollar's Crown of Thorns

I have now segregated US treasury bond auction updates into their own separate post. This is the 5th of a monthly series of posts updating the bond auction rates and bid to cover ratios. I have previously covered these within the weekly updates. I consider this to be the most important part of what I am covering on the substack and it is where we will see the first signs of distress within the market that the federal reserve cares about the most.

You can view the previous Months’ posts below

(Prior to February Treasury auctions were tracked in the weekly forecasts)

Please refer to the Backdrop Post and trade with mindfulness.

Please refer to Definitions page for any terms or abbreviations that I use that you don’t understand. If a term is missing, please let me know.

Since this is a repetitive series, the text that is repeated each month is in quote format.

Table of Contents

State of the Narrative

Primary Auction Results June

Bid to Cover Ratios

Interest Rates

Secondary market Treasury rates

Market Impacts

Conclusion

1. State of the Narrative

As usual we will start out with a State of the Narrative, this one will be shorter than the initial segment in February as we simply have to cover the changes over the last month.

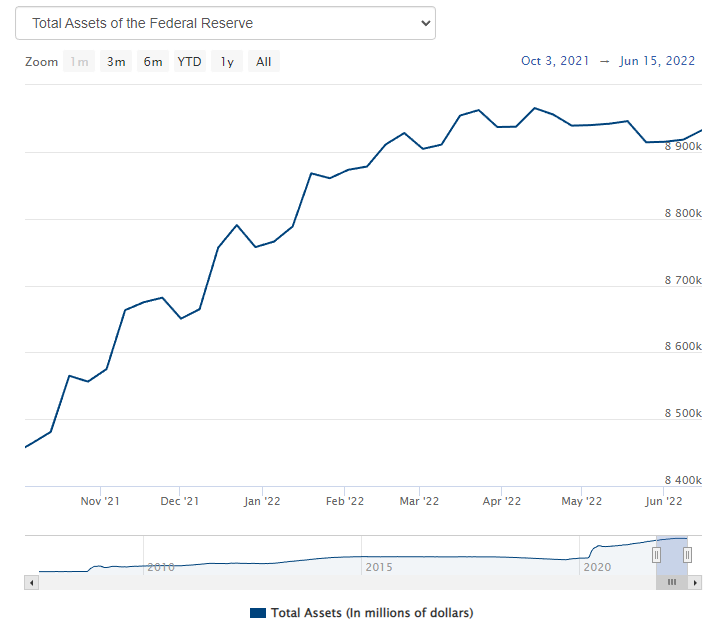

It looks as if the beginning of Quantitative Tightening may have begun, but from the Fed’s own report of their balance sheet it is still unclear and won’t be confirmed for another 1-2 weeks.

From what we saw in the secondary treasury markets in the week of 6/6/2022-6/10/2022 I suspect that QT has started, and it’s the main reason I stated that the following week would be one of the bloodiest weeks for the markets in recent memory.

The treasuries markets closed on Friday with treasury sale values in freefall and rates skyrocketing. That trend will continue into Monday, and I expect Monday 6/13 to be one of the worst days for the markets as a whole in recent memory.

Last month we got a break in the grinding down of asset prices, but from here on out, expect no break until the Fed chickens out when the interest rates offered by the treasury in the primary auctions have been too high for too long. We’ll see intervention in the treasury markets and that will mark the secular bottom for just about every single asset. My original prediction was for the Fed to fold in April/May. I revised that prediction in May and no longer have an expected time-frame.

Last year I had stated that the Fed would likely be forced to reverse course in April or May. I was presuming that combined pressure from the Treasury and the markets would weigh too heavily on their conviction. I am going to have to revise that prediction based on today’s rate hike. I no longer believe that the Fed is watching the markets at all and is going to try and bull rush their way as high as they can with the overnight rates.

Lower in that same section linked above we discussed what level of net interest would cause undue pressure on the US Treasury. This is something to consider as roughly 1/3rd of all of the outstanding US bonded debt matures each year, so when interest rates rise as fast as they did this year, the US Treasury very quickly comes under pressure as the interest payments they have to make increase rapidly.

For continuity sake, below is the same chart of the yield from the 2 year US treasury note that I have provided in every single one of these treasury bond posts. Each post has been accompanied by an orange dashed line to better help you to visualize how much yields have grown over the course of a month.

You’ll note that last month, treasury rates were mostly stable with the month ending around the same yield as April… that was not the case this month, and at 1 point the yields across the board were up over 1% on the month across nearly every treasury with a maturity above 1 year. The 2 year pictured above saw treasury rates go up roughly 0.7%, and that correlated with a bloodbath in the markets. In general, that is always how the market is going to react to treasury yields going up.

If indeed it is true that the Fed has begun QT then we will see acceleration in interest rates across the board for all treasuries, and that might be reflective of what we have seen in the markets so far this month. But as previously stated, we won’t bee able to confirm that for another 1-2 weeks because the Fed is slow to update their balance sheet postings online.

Anyways, lets jump into the meat of the treasury performance this month.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.