Review - 5/1/23 - Powell's Last Hike?

Review - 5/1/23 - Powell's Last Hike?

Regional Banks Continue to Fail

If you are a new reader, there are helpful links at the bottom of this post.

Table of Contents

Continued Bank Failures

Consensus Giveaway

Australian Interest Rates

US Interest Rates

EU Interest Rates

Crypto Macro

Price Action

Coinbase & SEC Update

crvUSD

Conclusion

Internal References

1. Continued Bank Failures

Obviously, these failures are expected and I’ve already explained why previously, so I will spare you any explanation beyond the following.

Rising interest rates mean that many assets banks have can no longer be sold for a profit, but instead at a loss. If they hold these assets to maturity they are fine, but if they have to sell them and the losses realized are in excess of their reserves on hand they become insolvent. This is made worse by depositors withdrawing funds.

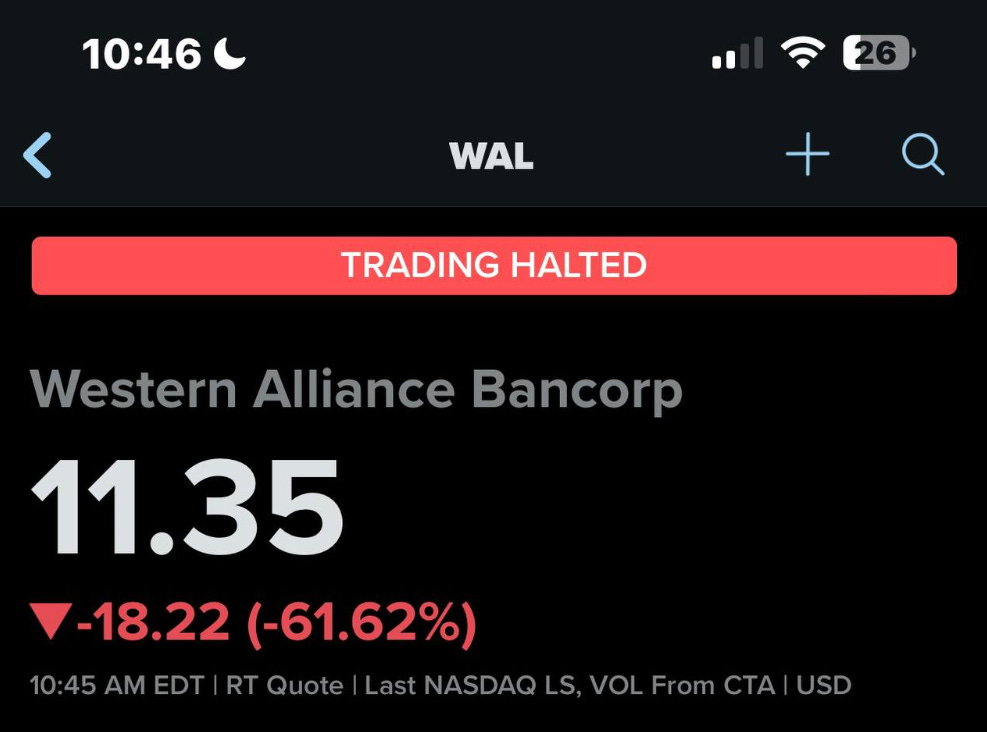

Those following on Instagram may have noticed I posted about two banks likely to fail this week and a third in my IG story that isn’t far behind. At top of my mind, there are three going this week and we’ve seen trading halted numerous times for these bank stocks due to how lopsided traders’ positions had gotten.

This isn’t secret knowledge, everyone is openly discussing these impending failures as this concept has entered the public zeitgeist since March with the failures of SVB, and Silvergate (Silvergate didn’t fail, it was destroyed by targeted regulation, but it looks the same from the perspective of the public).

We’ll discuss the Federal Reserve’s reaction to this in section 3, but let’s muse for a moment on what’s going on. Remember, Every bank has the exact same problem in relation to interest rates. On top of that, we live in a society where pulling money out of your bank electronically is very easy. And even beyond that, short-term T-bills can be easily purchased and outperform high-interest savings accounts. It’s essentially the Dollar Milkshake Theory applied within a localized geography. Banks can’t compete with the US treasury rates, and those who couldn’t adjust their balance sheets to anticipate this in time are unable to keep up.

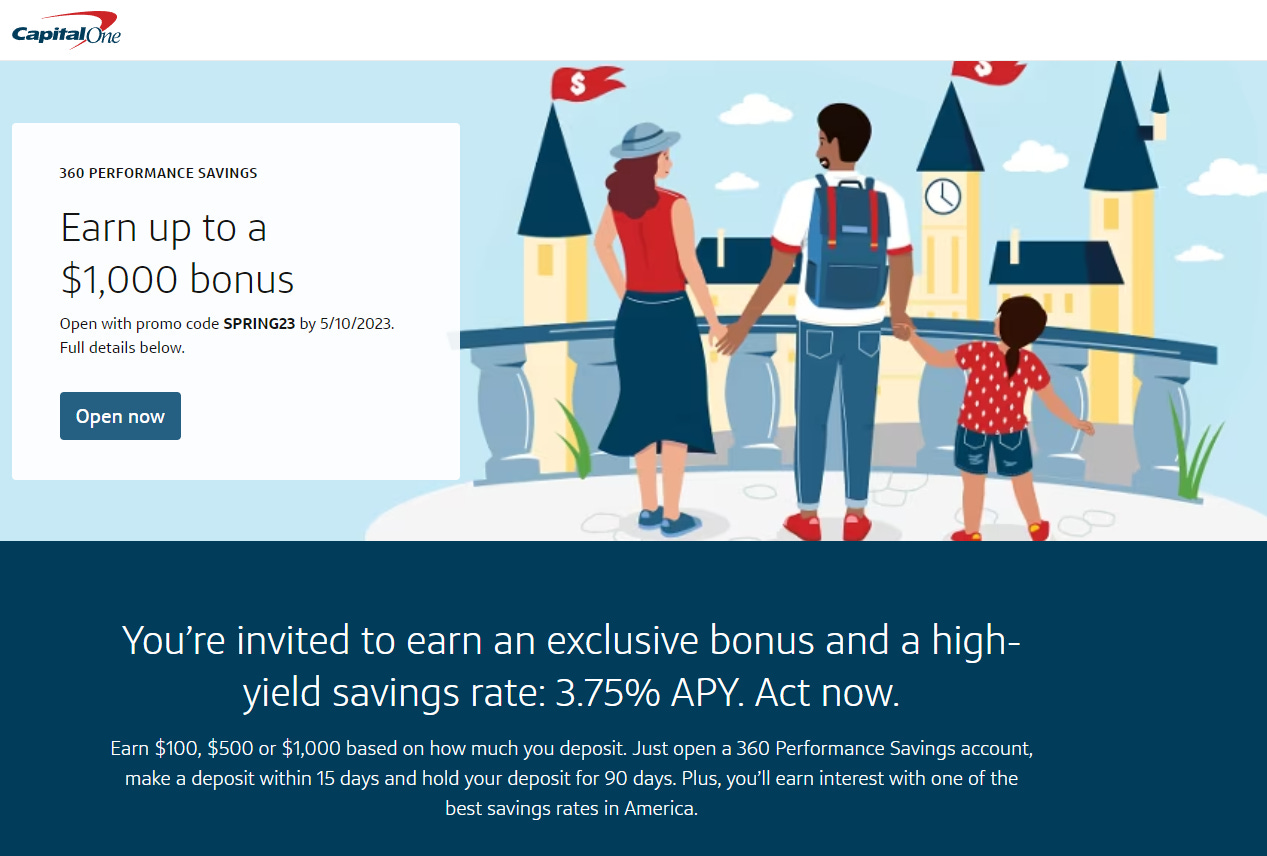

No doubt you’ve probably seen offers like the one below from institutions you bank with.

$50k in a savings account earning 3.75% earns an additional $1,000 after 90 days. That’s a 6% return which is competitive with short-term treasuries. The 3.75% is not competitive, however, but their hope is that you leave the money in after 90 days because closing bank accounts and withdrawing is inconvenient. Every bank is doing this right now, and they’re all doing it for the same reason. They are fighting for liquidity at a time when they don’t want to be forced to sell their assets at a loss and mark their remaining assets to market.

The banks can’t compete for deposits, and this is at the exact time that their own investments are losing value because the same treasuries are outcompeting bank assets in the secondary markets.

These bank failures are the natural consequences of our response to the 2008 financial collapse. Be Sure, your sin will find you out. They are inevitable, the only thing we can control is when they will happen. For the past 13 years since QE started, we have been kicking the can down the road because we do not wish to pay the price for that which we received in 2010. We can’t run from who we are. Our government wanted to protect us from the immutable laws of nature. The populace went along with it, but 1+1 still equals 2. The piper must be paid.

For now, we’ll watch more banks succumb to toxic assets. I expect the Fed to make a few moves in the short term, but I’ll get into that in Section 3.

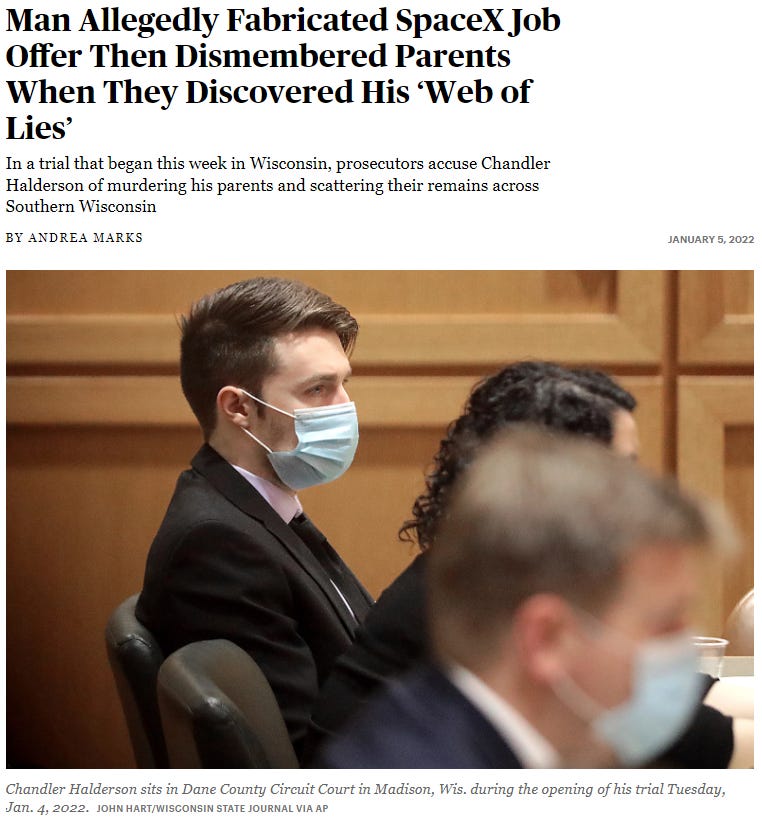

One of the darkest impulses of the human psyche is that of attempting to avoid the consequences of our actions. Most of the worst suffering we experience as humans occurs when we attempt to avoid the natural suffering of life. Bad things happen to us all at some point. This is unavoidable. You’ll lose your job, hit a financial snag, lose a loved one, suffer a major injury, etc. Many negative things come along with these events. Maybe you’ve lost income, owe money, are lonely/suffering, have to make major lifestyle changes, or have to give up things you enjoy. It could be you don’t want to accept these consequences. Maybe you try to maintain your lifestyle because you’re avoiding telling your girlfriend that you got fired and you run up your credit card. Maybe you enter an abusive relationship just to fill a space that a past partner had filled. Or, maybe you don’t know how to tell your parents you dropped out of College and so you murder them and scatter their limbs across half the state.

Bad things get worse when we avoid them. It’s a rare scenario when you can avoid dealing with a problem and it gets better in time. The rule is almost always that consequences get worse and harder to avoid the more you avoid them.

It’s not a coincidence that each crash is larger than the last, and each has a larger impact on the lower and middle classes. No doubt, we will do the sinful thing and avoid the consequences again to lay them on the backs of our children. A large burden to carry. But the consequences are inevitable. Who will pay them is the only question remaining.

Consensus Giveaway

Last week we had a subscription giveaway and 5 of you entered. I let the wheel of names pick a winner and it determined that the user microwave was the winner.

So as of today, Microwave has been comped with 1 years subscription for free. if you click the “Manage Subscription,” you should now find your subscription renews in May of 2024.

Congratulations.

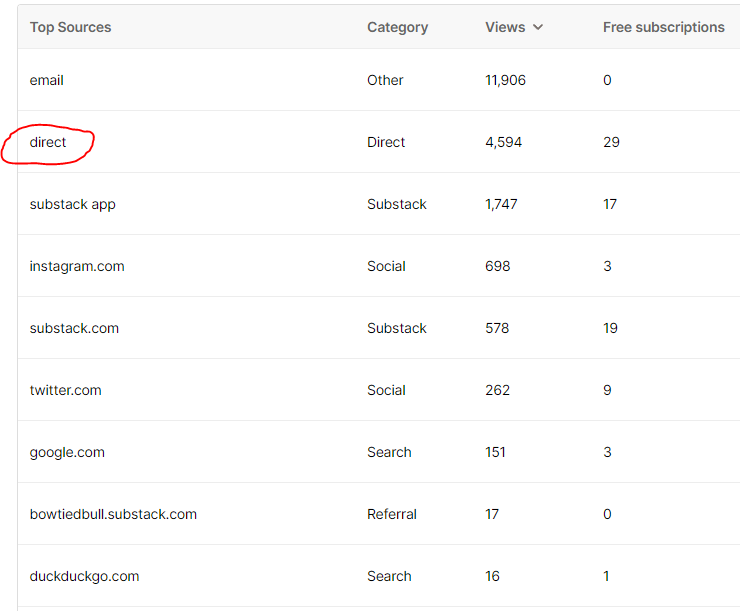

We’ll have another giveaway the next time we hit a subscriber milestone. For reference, we do one every time free subscribers hits a multiple of 100, and every time paid subscribers hit a multiple of 50. I’m horrible at marketing content but a lot of you share my content and it means a lot to me. It’s either a testament to how bad I am, or to how good you all are at sharing, but by far my largest source of new traffic comes from people like you directly linking my content to others.

This primarily succeeds because of ya’ll sharing content with others. I would never ask you to share anything I write just because. You should only share it if the writing stands out or speaks to you, or is meaningful and of use. You should never share something just as “a favor” for me. I am gratified in my belief that when you share something you do so because you genuinely want to regardless of who wrote it. And if one day I ever start writing dogshit, you owe it to me to unsubscribe. The only thing that should be rewarded in the creator economy is genuine production. As soon as I stop doing that to a level worth rewarding, I need to be informed of that as quickly as possible. This should never be charity.

Keep reading with a 7-day free trial

Subscribe to Flirtcheap’s Asymmetric Economics to keep reading this post and get 7 days of free access to the full post archives.