I was Wrong on the BoJ

If you are a new reader, there are helpful links at the bottom of this post.

This is another slow news week, the only event is a Bank of Japan interest rate decision and that section alone ballooned up into 4,000 words, so this post is now explicitly about the Bank of Japan again, I’m sorry but this is the last one, I promise.

Also, I’m going to apologize right now. This is probably the least approachable post I have made in terms of accessibility for the everyman.

If you find your eyes glazing over as you’re reading this, skip to sections 5 and 6. Rough Outlooks for the future are presented there in more accessible terms.

Table of Contents

BoJ Interest Rates - Why I Was Wrong

An Academic Economist

Ueda’s Short Time in the BoJ

Reading Ueda

Ueda’s Outlook

Conclusion

Internal References

1. BoJ Interest Rates - Why I Was Wrong

It’s another relatively slow news week in terms of scheduled central bank events. This week’s BoJ decision may seem like it should be a big deal because it’s Ueda’s first meeting, but in general, the first interest rate decision by a new central banker is not to change anything as it takes 4-8 weeks to get into the rhythm of things, and these decisions aren’t made spur of the moment but typically several weeks in advance and in concert with other central banks.

Ueda has been at the helm for 2 weeks, it’s likely the decision for this meeting was made before he was sworn in.

And yet, I’m still going to talk about this meeting regardless.

It often takes me several times to iterate on an idea before I truly arrive at my actual conclusion. I’m going to take this space now to attempt to synthesize what I have been thinking about the new BoJ Head over the last 2 months as I think I’ve arrived at my final conclusion now.

First things first, they aren’t going to make any major policy changes this week.

You’ll recall that 2 weeks ago, we discussed Ueda as Japan’s first academic economist to head the BoJ. Typically, the Japanese administrative class has been wholly apart and separate from Western cultural institutions as they often promote ministers and administrators from within. That is one of the reasons why the Japanese Central Bank Policy has been so wildly different from the rest of the Western world.

In the West, you would never see someone in government admitting to the following, but in Japan, it’s not out of the ordinary.

People in the West would laugh about something like this being uttered, and please don’t construe this to mean that every member of the Japanese government has more experience with administration than with whatever department they are overseeing. That’s not what I’m saying, what I am saying is that Japan values its own culture and cultural institutions above all else. Most in the Japanese government were totally and wholly educated in Japanese Universities, and they rarely pull individuals from the private sector into positions high within the government.

To rise high in the Japanese Government you essentially have to make a career out of government service. Straight from university to prefecture-level administration. That’s how it goes. To rise to any major position within the Japanese Government you have to work your way up. You don’t get to start at the federal level. This is very different from the US, where if you are successful enough in the private sector you can transfer directly into an administrative role at the Federal level. Gensler, who we discussed last week, is a great example. He jumped directly to the US Treasury from the C-Suite of Goldman Sachs.

Due to this, the Japanese bureaucratic and administrative class is very insular and wholly separate from the world around them in a number of ways.

Ueda is a major change in this way.

I have previously framed my expectations for Ueda as such.

He’s spoken briefly out of both sides of his mouth. From a quick look at his stated goals and thoughts, he seems as if he wants to end the Bank of Japan’s ultra-loose monetary policy, but he doesn’t seem to be in any rush to do it.

This isn’t an incorrect assessment, and that’s not what I’m here to correct. I’m here to correct how I’ve framed Ueda and what he means. He probably does want to end the BoJ’s current monetary policy, but I expect he actually may move faster to do so than I may have made it seem before.

Let’s discuss exactly what’s so different and why.

2. An Academic Economist

In my last post about Ueda, I discussed his background but I still didn’t really get why it was so different.

Kazuo Ueda is an academic economist. He will be the first BoJ head to come from academia and not from within the BoJ or the finance ministry itself. Kazuo received his Ph.D. in economics from MIT and studied under one of the primary proponents of New Keynesianism.

You’ll note that I acknowledged his background and the radical shift it implied but I didn’t yet grasp just why it was so different. This may be due to my own blind spot and the severe disdain I hold towards academics. I’m working on being more mindful of this. Yes, what Ueda studied is likely to make him more inclined toward Western thought on fiscal policy. But the fact that he was not promoted up through the government itself is a much bigger deal than I thought.

You may remember that at the beginning of the year, the two contenders for the head of the BoJ were Amamiya and Nakaso. Both contenders were from within the BoJ and the Ministry of Finance. Both were status quo in this manner.

Ueda is not status quo at all. As covered previously, Ueda is an academic first. After receiving his Ph.D. from MIT, the majority of his career has been as a University Professor at a few institutions across Japan (Osaka University, University of Tokyo, Kyoritsu Women’s University, and others). His only experience in government was as a BoJ board member from 1998 to 2005.

This is a far-cry from the lifetime admins and bureaucrats that make it to top positions in the Japanese Government.

3. Ueda’s short time in the BoJ

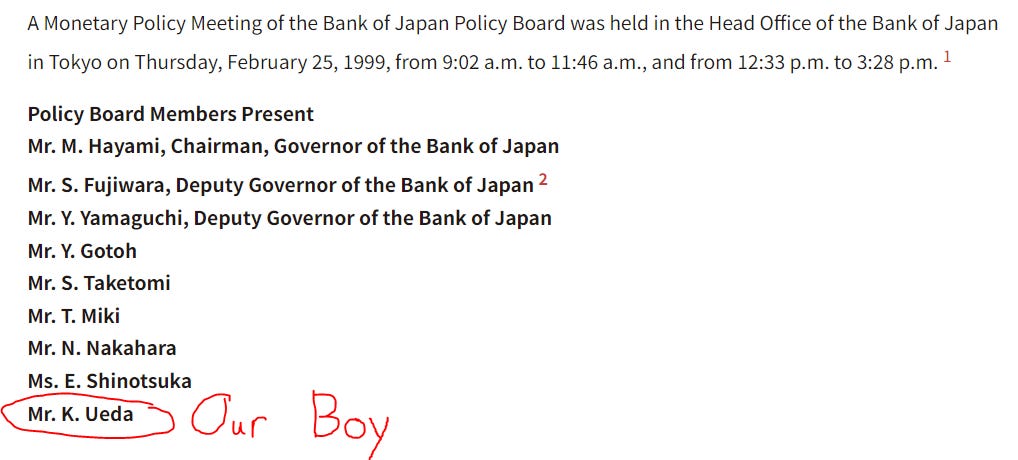

We’re going to take a look at the BoJ minutes from a meeting in 1999 where a debate about QE occurred. Take note of how different these meeting minutes read from the FOMC minutes. You can actually read the debate on policy and see how many members agree/disagree with any specific proposal. The FOMC minutes are mostly just a joke of a pre-written script.

For context, this meeting occurred on February 25th, 1999. Previously on February 12th, the BoJ had just begun a ZIRP (Zero Interest Rate Policy - in this case holding the overnight lending rate to a range of 0.00% - 0.25%) in an attempt to fight deflation and encourage spending to try to bring Japan out of its Lost Decade (at the time they thought they had only lost 1 decade, the phrase has since been renamed to “Lost 20 years” and then “Lost 30 years”).

You’ll note a Mr. K. Ueda as a Board member, that’s him. During the minutes, the opinions expressed by board members are anonymized, but it’s possible we might be able to guess who is who.

At that point in time in the US, Alan Greenspan was undergoing the policy of what was essentially called “The Greenspan Put,” basically if the stock market looked weak, the Fed would cut the overnight rate to backstop the stock market and he reliably did that from ~8% all the way down to 1% from 1990-2003, with a large portion of the rate cuts occurring from October 2000 - October 2002.

We could spend an entire article discussing how Greenspan essentially threw all of the hard work and sacrifices made by Volcker off to the side to prop up the stock market for Bush Sr., Clinton, and Bush Jr. but for now, that’s irrelevant. Just know that in the background of the turmoil in Japan, this was ongoing in the US. You can credibly blame Greenspan for most of the fiscal problems in the US right now.

At this point in time, Japanese economic ministers were desperately trying to achieve inflation above 1%. This same school of thought is also what informed Kuroda, and we’ve spoken at length on Kuroda’s (failed) attempts to do so and why they were misguided.

The general tone of the meeting had established the following priors.

Money was not circulating fast enough through the economy

They needed to keep production and employment high so people would have money to spend internally on Japanese products

Production and employment come from spending, which either comes from savings or borrowing

They needed to keep employment and income steady to boost spending to improve corporate earnings to fund future employment and income

It’s a cyclical argument, chicken or the egg

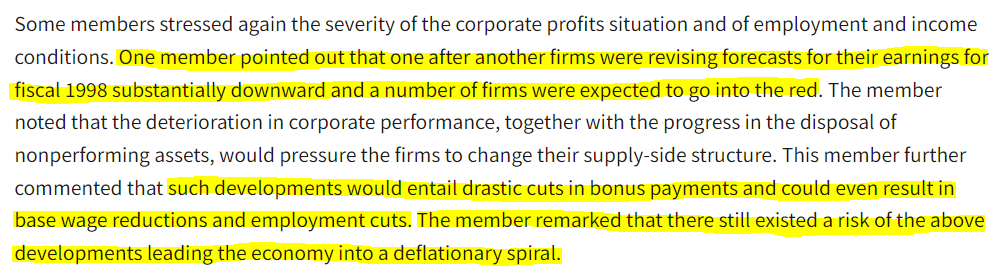

Members were even concerned that about 4 million employees were relatively idle and at risk of being laid off if the economy continued turning downwards. They expected unemployment to reach 10% if that continued.

Whether the concerns above were true in relation to whether or not the BoJ leaned further into its Yen printing scheme (remember, this is 1999, it’s been going more or less like this since then) is immaterial, all that matters is that this is what the group agreed was true.

One of the reasons Kuroda was chosen back in 2010 to head the BoJ is because he invented the concept of the Currency War that the BoJ was discussing here in this very meeting. The post-2008 world was one where Japan’s QE was not strong enough to inflate its own currency faster than its export partners were inflating their currencies, which is why Kuroda made the major blunder of introducing negative interest rates to the world.

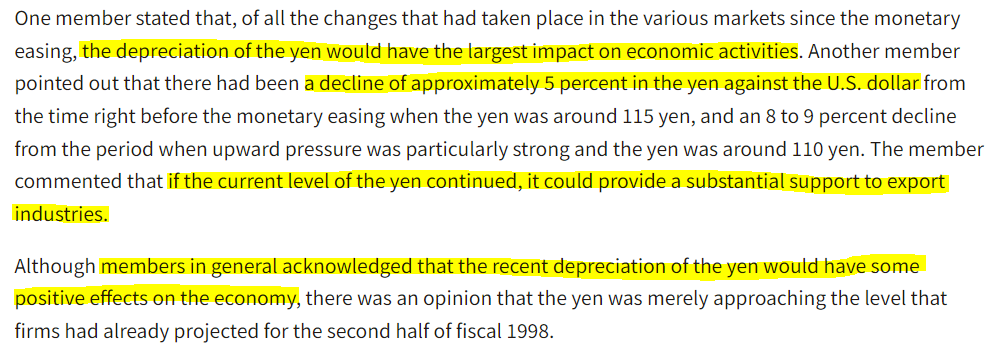

What follows after this is a mostly sensible debate where the members all discuss why they shouldn’t try to push the overnight interest rate down even further. At this point, it was sitting at around 0.15% which was within their range of 0.00 - 0.25%, but some discussion had ensued about trying to keep it at the lower end of this range (closer to 0.00%). Reasons that were cited for not doing so were things like the devaluing of the savings rate making deposits unattractive to regular citizens who just want a reasonable return on the money they put in their bank. Members also discuss how a rising budget deficit was pushing interest rates up and shifting the natural supply-demand forces that created price discovery in the bond markets. They, rather sensibly, discussed how their current attempts at QE would be less effective if the budget deficit continued to rise.

Some members even stated that the BoJ was at the limit of what impact they could safely have on the economy and that (heaven forbid) the economy would have to grow on its own with some government assistance like tax credits and unemployment benefits.

You can see the limited thinking that was present among the Japanese bureaucratic class for what a central bank could and could not do here. Perhaps that was for good reason. Just because something is theoretically possible does not mean that we should do it. We’re all reminded of our favorite Jurassic Park quote:

“Your scientists were so preoccupied with whether they could, they didn’t stop to think if they should.”

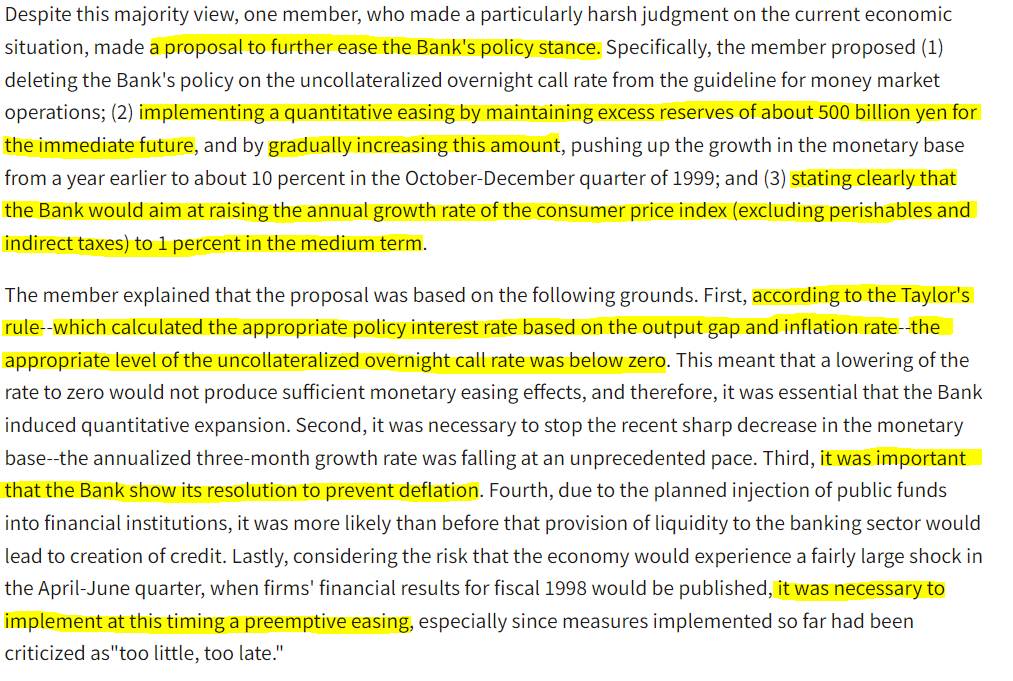

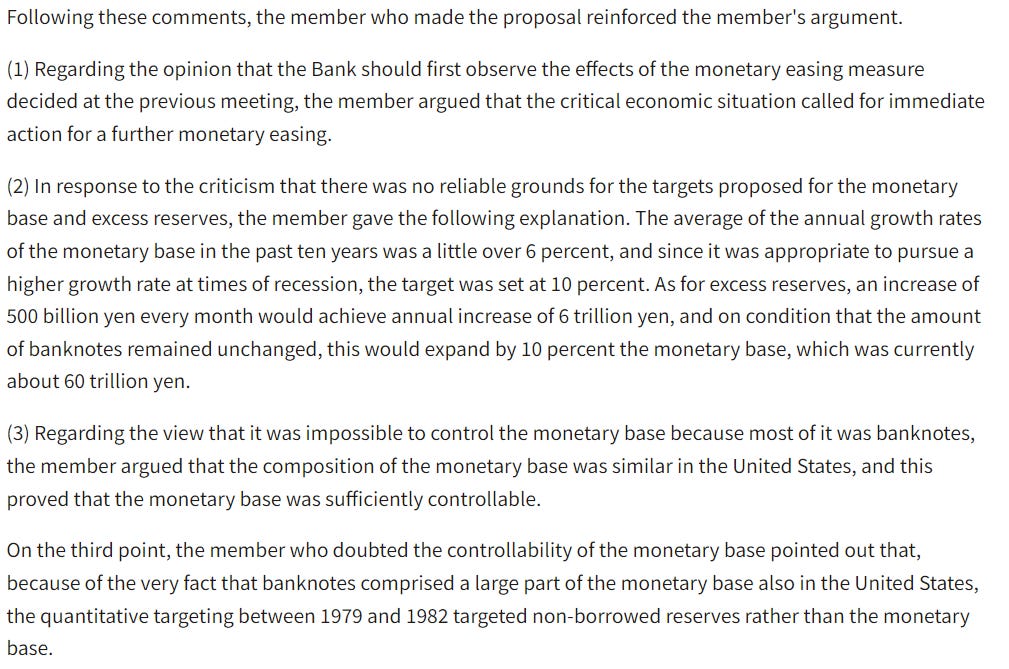

After a relatively tame debate among the members about the money supply and potential policy expansion, someone boldly steps in to join the discussion and I would bet my Bitcoin address that this member is Ueda.

This is essentially New Keynesian theory (CPI targets, gradually increasing excess reserves through QE, determining policy rate based on CPI, major concerns about preventing deflation), and quoting the Taylor Rule in 1999 is a dead giveaway that he’s not from the Japanese Bureaucratic class. This was essentially the ECB’s playbook from 2008 onwards, and we’ve covered that failure here extensively. From this point onwards the entire meeting circled around this one member and his proposals to the BoJ.

While the bank did maintain QE, they didn’t push as radically far as he proposed and raised interest rates a little bit above zero in 2001; and Ueda probably believes that Japan would have been better off if they had (he states as much in an article I quote in the next section). Japan’s problems are larger than money, of course, they have unbalanced demographics that will perpetually shift production and spending in ways that are detrimental to the kind of economy they want to have. That can’t be overturned by printing the wealth that otherwise would have been created by an entire generation of children that were never born and families that were never started. How do you maintain asset prices when there are not enough people in the next generation to buy those assets from people trying to retire? Trick question: You don’t. But that’s an entirely different discussion.

4. Reading Ueda

You may remember that in my post about Ueda 2 weeks ago, I stated that I hadn’t yet read any of his papers, but like the Black Cameraman in Scream 2, I’m reading it now.

I’ll admit. Ueda has written over a dozen papers and books on economics (in Japanese). I haven’t read a single one of them. My interpretation of the man is shallow and based solely on his field of study, his mentors, the people he says inspired him, and the speeches he has given on his plans for policy. It all aligns in one direction.

We’re going to take a short detour to this paper written in 2005 by Ueda and others before returning to why I think Ueda was chosen and what Japan might expect from the BoJ in the short and near term. Please note the state of zombie economy that Japan was already in by this point.

Although taxpayers’ money, bank earnings, and bank capital, in total amounting to about 20 percent of GDP, have been used to address the non-performing-loan (NPL) problem, the banking system has not yet fully recovered.

Take note that the paper also acknowledges the failing and negative outcomes of ZIRP and NIRP.

Moreover, the BOJ’s measures to this end have caused some unusual developments in the money Japan’s Deflation, Problems in the Financial System, and Monetary Policy and capital markets. These include a lowered intermediary function of the money market, the emergence of negative interest rates in some areas of the money market, declines in credit spreads, which were already narrow prior to the ZIRP, and a lowerthan-expected increase in the issue amount of corporate bonds.

ZIRP causes a number of issues among which; supply and demand can push some inelastic supply loans into negative rates. If you can borrow for negative rates, why would you ever issue a loan? Note that the issuance of corporate bonds was falling. When a corporation borrows money, they do so by offering a corporate bond, which has a yield on it that the corporation needs to pay back at a future date. But if you can borrow money for negative interest, then there is no need to pursue a loan at the corporate level, and no need to issue corporate bonds.

Ueda outlines the problem for Japan as one of GDP and inflation. He and the other authors of this paper claim that due to economic shocks to the equity value of assets in Japan, business investment had decreased significantly. Business investment is a key component of GDP and the claim is the following:

The EVR shocks seem to have raised GDP and the CPI through their effects on business fixed investment in the late 1980s, while they have worked in the opposite direction since the early 1990s. Without the shocks, fixed investment would have been higher by some 30 percent in early 2003, GDP by 5 percent, and CPI inflation by about 2 percentage points, implying that deflation would have ended by now by a considerable margin.

In the 80’s, assets and stock prices went up ~500%, in the 90’s they went down by ~75%. Businesses were less willing to spend money and invest in the 90s because they were experiencing a reverse wealth effect. When most academics speak of deflation in Japan, the phenomenon they are describing that Japan is so scared of is not groceries getting cheaper for the average shopper, but assets on balance sheets losing value and discouraging businesses from continuing to invest.

This is the problem Japan has been trying to fix. On its face, it’s obvious this is a demographic problem. What do retirees normally do? They cash out their stocks and bonds, budget for retirement, decrease consumption, and downsize their real estate holdings. Japan has been running a wartime economy since the ’50s, and wartime economies typically run people ragged and destroy their work-life balance. Families decreased, people had fewer children (and continue to do so), and there was no next generation to keep buying stocks and real estate at the volume needed to maintain asset prices.

You may be able to gain an image of just what it is central banks are doing when they print money to expand their asset sheets. I’ve already discussed it above, but they are essentially printing money to simulate the economic impact that families who never were would have otherwise had on the existing productive base. The theory is that you can do this for a short while and then unwind the position slowly at a later. Obviously, we’re living through decades of proof that this can’t be easily unwound, but back in 2005, there was very little proof, only theory.

As a reminder, from a post I made over a year ago. The Bank of Japan bought up it’s own stock market from it’s retiring demographic base in order to keep prices high.

Even their central bank holds more assets than the entire GDP of their country at 128%. In order for Japan to taper, they will have to spend decades selling assets back into the markets and driving prices down of basically all national investments since the BoJ is also the largest holder of stocks on the NIKKEI (Japans version of the S&P 500).

There is a lot we can learn about 1990s Japan that applies to Western economies today, even still.

Firms also invested huge sums of money in land for speculation and securing of collateral for future borrowing. They also added substantially to their employment pool, as they believed that a period of labor shortage was at hand.

In the face of a demographic bomb, irrational exuberance was still the name of the game in the early 90s. Right up until the collapse began in earnest firms were heavily speculating on land, labor, and capital investments. They didn’t reverse course until the collapse was at hand, and this is the heart of the problem that Japan defines as deflation and has spent the last 3 decades trying (and failing) to fix. It’s a battle of Boomers vs. Zoomers in Japan, and ironically the Boomers are learning that not having an enemy to fight against is worse than losing to a demographic enemy.

In response to firms running into a demographic-induced economic slowdown, the BoJ started printing yen and using it to buy stocks, corporate bonds, government bonds, and assets in order to simulate the never-born economic activity that was lost in a wartime economy that disregarded the family in favor of economic production.

In the paper, Ueda congratulated the BoJ for their success during his time on the board, but notes that the recession in 2001 was due to them abandoning ZIRP too soon (which he voted against).

In response to the onset of deflation and the deterioration of the financial system, the overnight call rate was first lowered from around 0.43 percent to 0.25 percent in September 1998. Then it was lowered to near zero percent in March 1999. In April 1999, the BOJ promised to maintain a zero interest rate “until deflationary concerns are dispelled”—the so-called zero interest rate policy (ZIRP). The economy then recovered and grew at 3.3 percent between 1999/III–2000/III. Consequently, the ZIRP was abandoned in August 2000. The economy, however, went into a serious recession again led by worldwide declines in the demand for high-tech goods.

No mention is made that this recession occurred across most developed countries in this paper, but you’ll note Wikipedia covers the other countries that experienced this recession. Japan’s recession was likely caused by the introduction of the Euro and its impact on capital markets and FX flows. It’s not a surprise that every overly financialized economy and Europe experienced this recession. They were all cutting rates or in precarious positions. And an entire continent replaces a myriad of FX liquidity and currency baskets with a new singular currency. That will send a macro-shock as businesses adjust their purchasing and treasury strategy to the new currency and those chasing interest also adjust to this new reality as it took a while for price discovery to settle down within Europe.

Ueda believes that the BoJ caused this recession, and likely takes it personally that his New Keynesian theories were not being followed. But no matter, because when they returned to ZIRP shortly afterward they set out to increase the money supply by 67% from 2001 to 2004 in their fight against deflation.

5. Ueda’s Outlook

Ueda’s outlook can be found in the same paper and this is where we can glean information about how he will run the BoJ.

Needless to say, a commitment to maintain low interest rates until the natural interest rate rises generates a similar effect. In a similar vein, using a New Keynesian type model, Eggertsson and Woodford (2003) presented a version of price level targeting that could be considered an optimal policy in the face of a liquidity trap. In their case, the optimal policy is the commitment to maintain a zero rate until the price level is restored to a pre-committed path.

They are going to be setting inflation targets, and managing that in the same exact way that Powell was claiming to do. QE and low-interest rates until the target is reached.

You’ll note that even Japan is starting to show positive inflation in its own stats.

If Ueda sticks to his academic formulas and interpretation, he is going to have no choice but to start slowing down the rate of QE and allowing interest rates to rise if the inflation rate continues to remain elevated compared to CPI over the last 3 decades.

Sure, he’ll probably wait for a couple of months, half a year, maybe even a full year of data to confirm this, as you’ll note in his own papers and writings he often says that the consequences of waiting too long to end ZIRP and NIRP are relatively low compared to the consequences of ending early. This is a fallacy, of course, but it is what New Keynesians believe and is why the West in general was so slow to raise interest rates while Russia did the entire thing in a day.

Ueda was the surprise selection for the BoJ, and the government of Japan selected him because they want him to pivot away from the current NIRP (Negative Interest Rate Policy).

Let’s return back to our BoJ meeting in February of 1999.

The man I presume to be Ueda has been faced with a number of retorts and questions from the other members of the BoJ board during the meeting. and he responds to each in kind.

You’ll note point 1 is nearly identical to Powell’s playbook in 2020. New Keynesian thought at work. It’s more urgent to ease quickly than it is to reverse the policy. In point 2, he again makes the New Keynesian argument to target the money supply by having the central bank acquire excess reserves. This is New Keynesian inflation targeting policy. You’ll note that the bank more or less followed his targets of 10% a year later on in 2001. And finally, his example of controlling the monetary base uses the US as an example.

There is no one else on the board who would have brought this up except an MIT-educated economist.

Ueda was selected to bring this kind of thought to the Bank of Japan. Japan’s FX intervention last year was massive. It doesn’t take much economic understanding to understand that they can’t afford to burn $500 billion of FX reserves again. Ueda was selected in order for them to avoid that.

New Keynesianism is not an effective way to steward a currency, but in the face of the dollar milkshake, economies can only do a few things. Either shape up and produce enough that you can dictate terms to dependent export partners, or try to suck up an equivalent amount of liquidity alongside other Western central bankers. Japan is now realizing its choice and is likely going to attempt to pull the Katana out of their abdomen and hobble to a hospital.

Japan is in no shape to do the first option, so they are choosing the second.

6. Conclusion

I’m not a central banker. If I was ever given the role I’d probably be the worst one. My response to basically every problem is “it’s time to pay the consequences for our actions.”

But what do you actually want from a central banker if you are the prime minister of a country? You don’t want me. You want essentially what the Tate brothers describe in an ideal lawyer.

You want an academic who will invent theories and imaginative solutions out of Keynesian monetarism where Money is twisted and contorted into whatever shape you need.

Ueda is one of these such economists. His Western background is a seed change compared to the traditional backgrounds of those high up in the Japanese Central Bank and Finance Ministry. It’s so big of a change that this is the first time in post-WW2 Japan that anyone has been selected who wasn’t internally promoted.

The government is looking to him to make major changes and to bring Japan in line with Western economies.

How Ueda decides to do that due to some of the more challenging aspects of Japanese demographics and immigration still remains to be seen. But you can expect that the selection of Ueda will lead to the Bank of Japan joining other Western Central Banks in terms of policy within a short while.

The question is how that will occur. Obviously, most Western central banks have signaled that rate cuts are coming in the future. Will they perhaps meet in the middle? Will Japan’s current QE program slow down or halt, will they adjust long-term projections for the 10-year Japanese Government Bond to signal to the market that they will be easing up on yield curve control in the future?

I think the answer to all of these questions is yes.

And this likely means that the stress Japan will be putting on the US treasury bond market will likely be easing up sooner than I had previously assumed (still about 1 year out).

This is the subtle but meaningful way in which I must change my outlook from what I had previously stated.

7. Internal References

If you’re new and have a question, please read the FAQ post first.

If you wish to search through my entire substack, please refer to this guide post.

Please refer to the Definitions page for any terms or abbreviations that I use that you don’t understand. If a term is missing, please let me know.

The Substack app is out, consider using that instead of email or your browser.

That feel when minor formatting mistakes in the email.

you're not allowed to be wrong bro